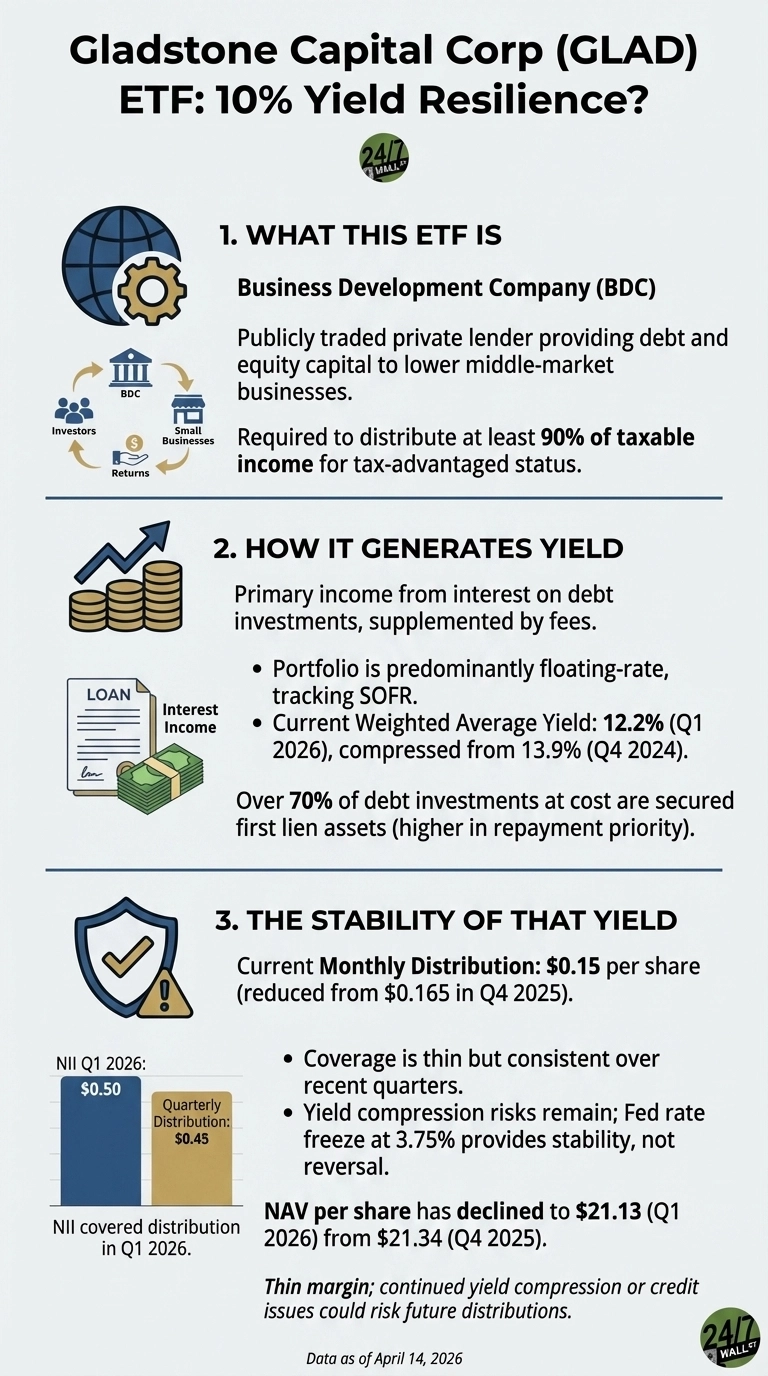

Gladstone Capital Corp (NASDAQ:GLAD) carries a yield near 10.4% and a monthly payment structure that appeals to income-focused investors. Whether that income stream holds up depends on mechanics that are easy to misread from the headline number alone.

How GLAD Produces Its Monthly Income

Coverage Is Thin but Consistent

- Q1 2026: NII of $0.50 per share covered the $0.45 quarterly distribution

- Q4 2025: NII of $0.50 per share covered the $0.45 quarterly distribution

The Rate Freeze: Stability Without Recovery

Gladstone Capital’s portfolio is predominantly floating-rate, so income tracks SOFR. The weighted average yield on the interest-bearing portfolio compressed from 13.9% in Q4 2024 to 12.2% in Q1 2026. The Federal Reserve has held rates at 3.75%, which has stopped further compression but has not reversed it.

Management’s response has been to grow the loan book. The weighted-average principal balance grew from $647.2 million in Q3 2025 to $772.3 million in Q1 2026, the primary lever that kept per-share NII stable as yields declined. It’s also important to note that the portfolio’s ending fair value reached a new high of $902.9 million. President Bob Marcotte noted: “These actions combined with our modest leverage have positioned us well to deliver continued asset growth and sustain our net interest income in support of future shareholder distributions.”

Balance Sheet Refinancing and Credit Trends

Gladstone Capital issued $149.5 million in 5.875% Convertible Notes due 2030 while redeeming higher cost 7.75% and 5.125% notes, lowering interest expense and extending maturity. The credit facility was expanded to $320 million, with the revolving period extended to October 2027 and the final maturity to October 2029.

Portfolio quality shows modest stress. NAV per common share has drifted from $21.30 to $21.10 over recent quarters. That figure is not alarming in isolation, but the direction is consistently downward.

Total Return and Price Context

Distribution Safety Verdict

The $0.15 monthly distribution is covered at current NII levels, but the margin is narrow. Portfolio yield, NAV, and fair value as a percentage of cost are all trending lower. The rate freeze provides stability, not reversal. A second cut is possible if loan book growth stalls or credit quality deteriorates. Total return depends heavily on reinvested dividends, given the price decline over the past year.

Data Sources

- Gladstone Capital’s 10% yield comes with a hidden strength: dividend coverage that actually holds (247 Wall St., April 13, 2026): Used for NII coverage ratios, portfolio composition, balance sheet refinancing details, and distribution cut context.

- Federal Reserve Economic Data (FRED) via Fuse API: Fed funds rate history and current 3.75% rate freeze since December 10, 2025.

- Alpha Vantage OVERVIEW and DIVIDENDS endpoints: Current yield, payout ratio, 52-week range, analyst ratings, and dividend payment history.

- Fuse API earnings data: Quarterly NII per share, total investment income, portfolio yield, weighted average principal balance, and NAV trends across Q2 2025 through Q1 2026.

Contact [email protected] for any questions or corrections.