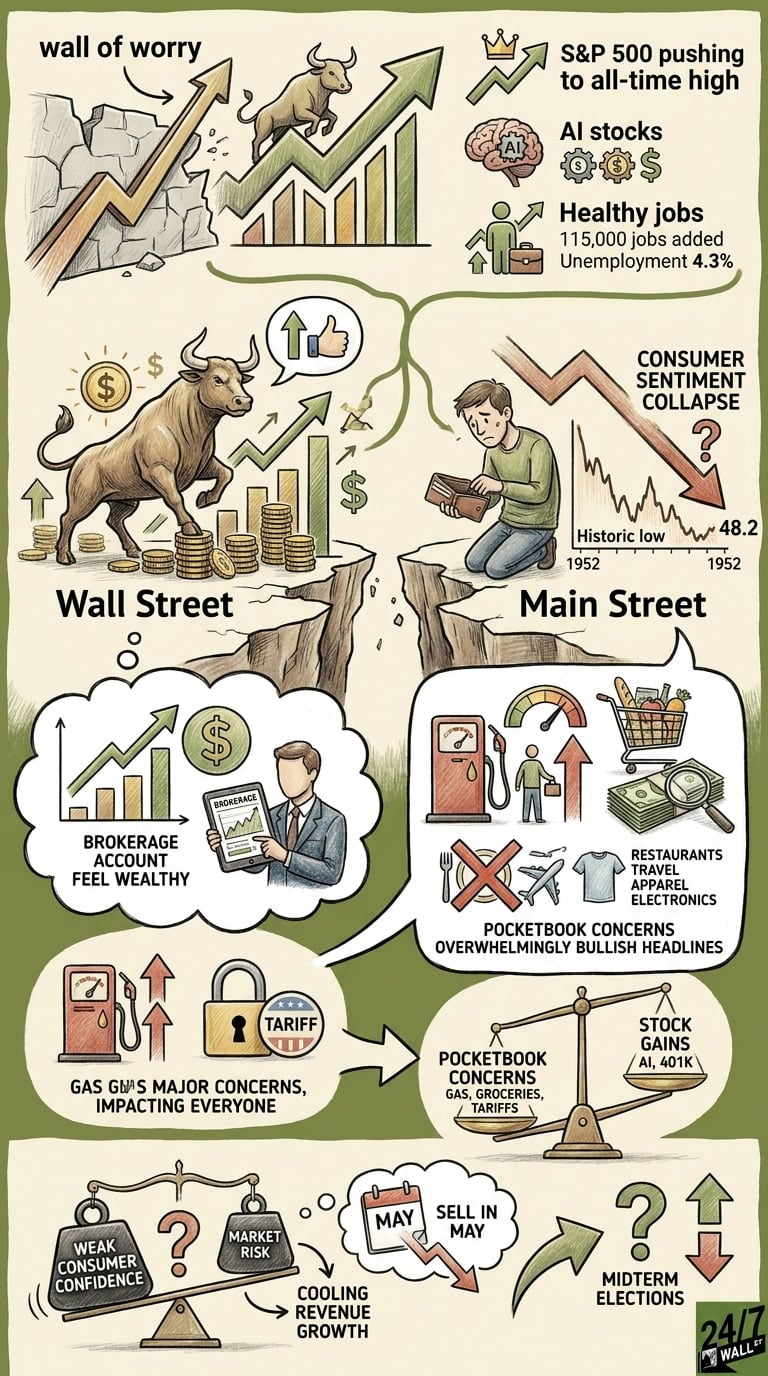

The stock market is doing what bull markets do best — climbing a wall of worry. The S&P 500 recently pushed to another all-time high, AI stocks continue pulling massive amounts of capital into the market, and the latest jobs report showed employers added 115,000 jobs in April versus expectations for 65,000. Unemployment held steady at 4.3%. By most traditional measures, that’s the kind of backdrop that usually keeps consumers upbeat and incumbents politically comfortable.

President Donald Trump recently pointed to both the labor market and record stock prices as proof that “our country is doing well.” And historically, strong markets and healthy employment numbers have been tailwinds heading into midterm elections.

Yet there’s one problem investors can’t ignore: consumers don’t seem to believe it.

Wall Street and Main Street Are Sending Opposite Signals

That disconnect may be the most fascinating — and potentially dangerous — market development right now.

The University of Michigan’s Surveys of Consumers has tracked household sentiment for roughly 75 years. Investors often overlook the report because it isn’t as flashy as payrolls data or inflation prints. But consumer spending makes up roughly two-thirds of U.S. GDP, which means how Americans feel about the economy eventually matters to corporate earnings.

And the latest reading wasn’t just weak. It was historic.

The University of Michigan’s preliminary May consumer sentiment index fell to 48.2, down from April’s 49.8. That marked the lowest level ever recorded in the survey’s history dating back to 1952.

Surprisingly, this collapse in sentiment is happening while stocks are at records and job growth continues to exceed expectations.

That’s a sharp divergence from what investors usually see. Strong labor markets tend to support confidence because people who feel secure in their jobs are more willing to spend money on homes, vacations, electronics, and cars. Higher stock prices also typically create a “wealth effect,” where consumers feel financially stronger because retirement and brokerage accounts are rising.

This time, though, pocketbook concerns appear to be overwhelming the bullish headlines.

Record-high stocks and AI booms can’t hide the empty wallets on Main Street. The ‘Wall of Worry’ just got a lot steeper.

Record-high stocks and AI booms can’t hide the empty wallets on Main Street. The ‘Wall of Worry’ just got a lot steeper.

Why Gasoline and Tariffs Matter More Than AI Stocks

According to the University survey, about one-third of consumers spontaneously mentioned gasoline prices as a major concern, while roughly 30% mentioned tariffs. That’s important because energy costs hit consumers differently than stock gains.

A rally in semiconductor stocks may help investors with 401(k)s. But higher gasoline prices hit nearly everyone immediately. Filling up a tank isn’t optional for most households. Neither are groceries, utilities, or transportation costs. When those expenses rise, consumers often pull back elsewhere. Households simply have less money left over for discretionary spending.

And that matters for investors because discretionary spending fuels large portions of the economy:

- Restaurants

- Travel

- Apparel

- Consumer electronics

- Entertainment

- Home improvement

If consumers begin trimming those purchases, corporate revenue growth can cool quickly.

Geopolitical uncertainty has only amplified the volatility. ETF flows showed large capital outflows during March as fears surrounding the Iran conflict intensified. But April brought a sharp reversal as optimism surrounding a potential de-escalation and renewed enthusiasm for AI stocks triggered fresh buying.

Regardless of how you look at it, markets are trying to price two completely different realities at once — resilient corporate earnings on one side and deeply pessimistic consumers on the other.

Could “Sell in May” Finally Matter This Year?

Investors hear the old Wall Street phrase every spring: “Sell in May and go away.”

Most years, it’s little more than seasonal market folklore. But 2026 may offer conditions where it gains traction again.

Granted, the bull case remains strong. AI infrastructure spending continues expanding, labor markets remain healthy, and inflation expectations in the Michigan survey actually eased slightly, with one-year expectations dipping from 4.7% to 4.5%.

That said, sentiment readings this depressed rarely happen without economic consequences eventually showing up.

The biggest risk may not be an immediate recession or market crash. Instead, it could be slower consumer spending, weaker retail sales, and a gradual cooling in earnings growth just as markets are priced for perfection.

And with midterm elections only six months away, investors should expect every economic data point to receive amplified attention.

Key Takeaway

In short, the market’s biggest risk before midterms may not be unemployment, corporate profits, or even interest rates. It may be confidence itself. When consumers feel squeezed by gasoline prices, tariffs, and rising living costs, they tend to spend more cautiously — regardless of what the stock market is doing.

For now, Wall Street is betting AI-driven growth can overpower those concerns. Consumers appear less convinced.

When all is said and done, smart investors should watch whether Main Street eventually pulls Wall Street back down to earth — or whether falling energy prices and easing geopolitical tensions finally close the gap between the two.