Palantir (NASDAQ:PLTR | PLTR Price Prediction) trades at $137.80, with the stock going sideways while almost everything else rallied, and that divergence frames the setup from here.

Palantir builds enterprise AI software, with Gotham for the intelligence community, Foundry for commercial customers, and AIP turning U.S. commercial into the fastest-growing piece of the business. A year ago shares traded at $119.15. Today they sit at $137.80, a 15.65% one-year gain while the S&P 500 doubled with a 30.54% return. Q1 2026 revenue grew 85% year-over-year, FY 2026 guidance calls for another 71%, and the share price has gone nowhere since November.

The AI Software Compounder Argument

The bull case is operational. U.S. commercial revenue grew 133% YoY in Q1, and U.S. revenue as a whole grew 104% year-over-year. U.S. government revenue grew 84% year-over-year. Palantir’s “Rule of 40” score has hit 145%, and the company’s CEO said it “shattered” the metric that only a handful of other AI companies matched.

Earnings are catching the multiple. Reported EPS climbed from $0.13 in Q1 2025 to $0.33 in Q1 2026, and free cash flow guidance at $4.2-4.4 billion. Forward P/E sits at 93 against trailing ~150. If 2026 revenue lands inside the $7.182 billion to $7.198 billion band, today’s price stops looking absurd.

What 150 Times Earnings Has to Justify

Even after a 22.48% YTD drawdown, Palantir trades at sensible-esque prices with some precedent during bull markets. The market has already credited the company for hitting the high end of 2026 guidance and repeating in 2027. Anything softer is a derating.

Stock-based compensation ran $684 million in FY 2025 against $1.625 billion in GAAP net income. Termination-for-convenience clauses and long sales cycles make 133% commercial growth the most volatile line on the statement. Polythimarket traders price a 77% probability of a down close today and cluster s week between $132 and $138.

Waiting for Earnings to Catch the Multiple

Palantir is mid-digestion. Fundamentals are doing what bulls want, price is doing what bears want, and the two converge if 2026 plays out as guided. The setup is a bet you don’t need to be early on a stock the entire Street already knows.

Watch Q2 commercial bookings, Rule of 40 sustainability, and whether U.S. government holds its pace once federal budget cycles reset. If those check out, the forward multiple compresses without the stock having to move.

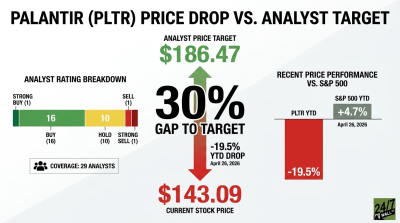

What the Analyst Coverage Says

Palantir has a consensus target of $153, implying roughly 11.9% upside. Coverage from 32 analysts splits across five rating buckets.

- 3 Overweight

- 17 Buy

- 10 Hold

- 0 Underweight

- 2 Sell

Over the past year PLTR has gained 15.65% while the S&P 500 returned 30.54%. Year-to-date, the gap widens, with Palantir down 22.48% against an 8.17% index gain. Beta of 1.52 magnifies whatever the broader market does next.

The Picture Post-Earnings

Palantir presents a mixed picture today. The business is executing better than almost any large-cap software story in the market, and the stock is down 22.48% YTD. That divergence resolves one of two ways. The multiple compresses peacefully as 2026 earnings arrive, or the broader rally re-rates AI software higher and Palantir becomes the reflex trade again.

A bullish re-rating signal would be a breakout above the 200-day moving average of $163.93 on a beat-and-raise Q2 report, confirming the multiple is willing to expand into the growth. A bearish signal would be a Q2 commercial growth reading below 100% YoY, which would crack the acceleration narrative that justifies a 97 forward multiple.

Until one of those prints, the market is paying full price for a story everyone already knows, with the math arriving roughly on schedule. Earnings need to do the work, unless the rally has another gear, in which case Palantir starts to look cheap next to the moonshots it gets compared to.

Contact [email protected] for any questions or corrections.