Palantir Technologies (NASDAQ:PLTR | PLTR Price Prediction) has been one of the most polarizing names in the AI trade, and that tension is showing up clearly in the price action. After a euphoric run, the stock has cooled hard in 2026, and our proprietary model now sees a measured recovery rather than a moonshot.

Our 24/7 Wall St. Price Target Points to $152

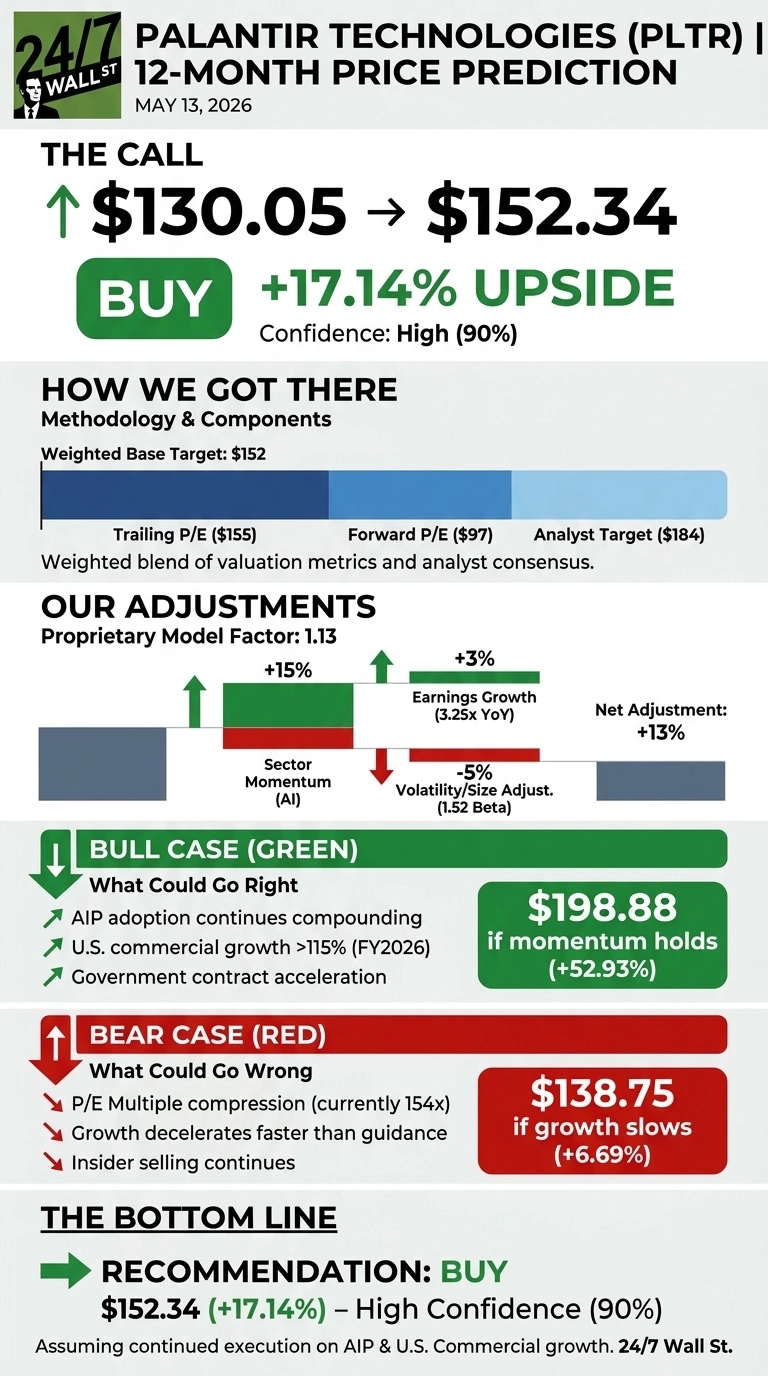

Palantir trades at $130.05 as of May 13, 2026. Our 24/7 Wall St. price target for Palantir is $152.34 over the next 12 months, implying 17.14% upside. We rate Palantir a buy with high confidence (90%), tempered by the fact that the stock carries one of the richest multiples in software.

| Metric | Value |

|---|---|

| Current Price | $130.05 |

| 24/7 Wall St. Price Target | $152.34 |

| Upside | 17.14% |

| Recommendation | BUY |

| Confidence Level | 90% |

A YTD Correction Sets the Stage

Palantir is down 26.84% year to date and off 2.8% over the past week, sitting well below its 52-week high of $207.52 but above the 52-week low of $118.93. The pullback came despite blowout fundamentals.

Q4 2025 revenue grew 70% YoY to $1.41 billion, U.S. commercial revenue jumped 137%, and CEO Alex Karp noted Palantir’s “Rule of 40 score is now an incredible 127%”. Management guided FY 2026 revenue to $7.182 to $7.198 billion, implying 61% growth. Fundamentals accelerated while the multiple compressed.

The Case for $200+

Bulls have real ammunition. U.S. commercial remaining deal value hit $4.38 billion, up 145% YoY, giving Palantir visibility most software peers would envy. Q4 closed a record $4.262 billion in total contract value, with 61 deals above $10 million. AIP adoption is the engine.

Wall Street’s consensus target of $183.73 sits well above ours, and 61% of covering analysts are bullish versus just 6% bearish. Our model’s bull scenario points to $198.88 by May 2027, a 52.93% return, if AIP wins continue compounding and government spend accelerates.

What Could Go Wrong

The risks are real. PLTR trades at a trailing P/E of 154x, price/sales of 62x, and forward P/E near 97x. Multiple compression alone could pressure the stock even as revenue grows. Stock-based compensation hit $684 million in FY 2025, and insider activity shows net selling across 72 recent transactions.

Prediction markets imply a high-probability range of $120 to $150 through May 2026, suggesting the crowd is more cautious than the sell side. Elevated SBC reflects Palantir’s aggressive talent strategy, and insider selling can be programmatic. Our bear case projects $138.75 if growth decelerates faster than guidance.

Palantir Price Prediction 2026-2030

Our 24/7 Wall St. price target of $152.34, a buy rating, and 90% confidence reflect a simple thesis: Palantir’s growth and Rule of 40 are anomalous, and the YTD correction has done meaningful work on the multiple. The thesis holds if AIP momentum and U.S. commercial growth sustain through Q2 2026, and weakens if FY 2026 guidance gets trimmed or government contract timing slips.

Looking ahead, our model projects Palantir could trade assuming growth gradually decelerates from 61% toward the 30% range with steady multiple compression. The 5-year base case lands at $214.58 by May 2031.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $152 |

| 2027 | $170 |

| 2028 | $188 |

| 2029 | $202 |

| 2030 | $215 |

These projections assume Palantir keeps executing on AIP and U.S. commercial expansion. Significant upside or downside could result from a step-change in enterprise AI adoption or a sharp reset in software valuations.

Contact [email protected] for any questions or corrections.