At $390, Alphabet (NASDAQ:GOOGL | GOOGL Price Prediction) finally earned its place alongside Nvidia (NASDAQ:NVDA) in the AI conversation is now trading its fortress balance sheet for the right to spend like a utility.

Alphabet has the rare full stack. Search and YouTube remain two of the most-visited destinations online. Cloud is compounding at 63% growth on $20.03 billion in quarterly revenue, sitting on a $462 billion backlog. Gemini lives inside the API, the consumer app, and Search itself.

The complication is on the cash flow statement. Capex more than doubled year over year in Q1 2026, free cash flow fell 46.6%, and 2026 capex guidance now sits at $180 billion to $190 billion. Long-term debt climbed from $22.6 billion in 2024 to $90.5 billion by March 2026.

What the bulls actually own here

Alphabet just posted $109.90 billion in quarterly revenue, beat consensus EPS by 94.1% at $5.11, and expanded operating margin to 36.1%. Cloud operating income tripled to $6.6 billion, and revenue from products built on Gemini grew nearly 800% year over year.

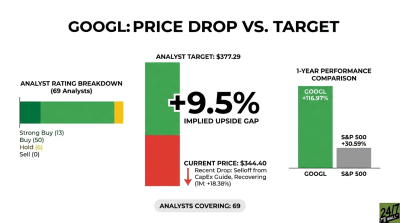

Valuation is what bulls underline. A forward P/E of 28 against 21.8% revenue growth and 82% earnings growth makes Alphabet the cheapest hyperscaler relative to its growth rate. 59 of 64 analysts rate the stock Buy or Strong Buy. Waymo just crossed 500,000 autonomous rides per week. The current multiple gives it almost no credit.

The big mistake hiding inside the big spend

Spending $180 billion to $190 billion in a single year only works if the demand on the other side is real, durable, and priced to clear. Q1’s headline net income was flattered by $36.91 billion in unrealized equity gains from the Anthropic stake. Strip that out and core earnings look ordinary against the spend. Capex hit 78% of operating cash flow in Q1, well above the historical norm near 35-40%, and the CFO openly warned of higher depreciation and data center energy costs ahead.

Long-term debt has quadrupled since 2024 and the cash-to-debt ratio has fallen from 4.82 to 1.40. Google is funding the AI race the way utilities fund power plants.

Why patience earns its keep

Both sides have a case. A $462 billion backlog represents real contracted demand. But management said the majority of TPU hardware revenue lands in 2027, asking investors to underwrite a year of margin pressure for a payoff that has not arrived.

If Cloud holds above 50% growth through the back half of 2026 and free cash flow stops bleeding, the spend was justified and the stock re-rates. If Cloud decelerates while capex climbs, depreciation eats the operating margin and Alphabet starts to look like an infrastructure business priced like a software one.

Why Alphabet is a Hold

Most of the bull thesis is already in the tape. Pressing against a 52-week high of $402 after a 160% one-year run, the market has paid for Cloud’s growth, the Gemini surge, and the Waymo milestones.

The bear case is real but unresolved. Free cash flow is down sharply, debt is rising, and 2027 capex will exceed 2026’s already-record level. Trust management’s ROIC framework and patience is rewarded over two to three years. Doubt it and Alphabet is turning itself into a leveraged AI utility in real time.

The Buy trigger requires Cloud growth holding above 50% for two more quarters while free cash flow inflects positive. The Sell trigger is the inverse. Cloud slows below 40% while capex climbs and operating margin compresses by more than 200 basis points. Between those outcomes sits a stock you already own and probably should not chase.

Owning Alphabet here is reasonable. Chasing it at all-time highs while the company quadruples its debt to fund an unfinished bet asks more of you than the math currently supports.

Contact [email protected] for any questions or corrections.