At current prices, Microsoft (NASDAQ:MSFT | MSFT Price Prediction) at $413.96 screens as attractive, Dell Technologies (NYSE:DELL) at $238.80 looks fully valued, and Intel (NASDAQ:INTC) at $113.01 looks overextended. All three have ridden the AI infrastructure wave, but the setup at each price has diverged sharply.

Microsoft’s pullback has reset valuation against accelerating AI revenue. Dell’s run has front-loaded a year of upside. Intel’s rebound has outrun the fundamentals. It reflects my relative preference within the group, and not an outright sell recommendation.

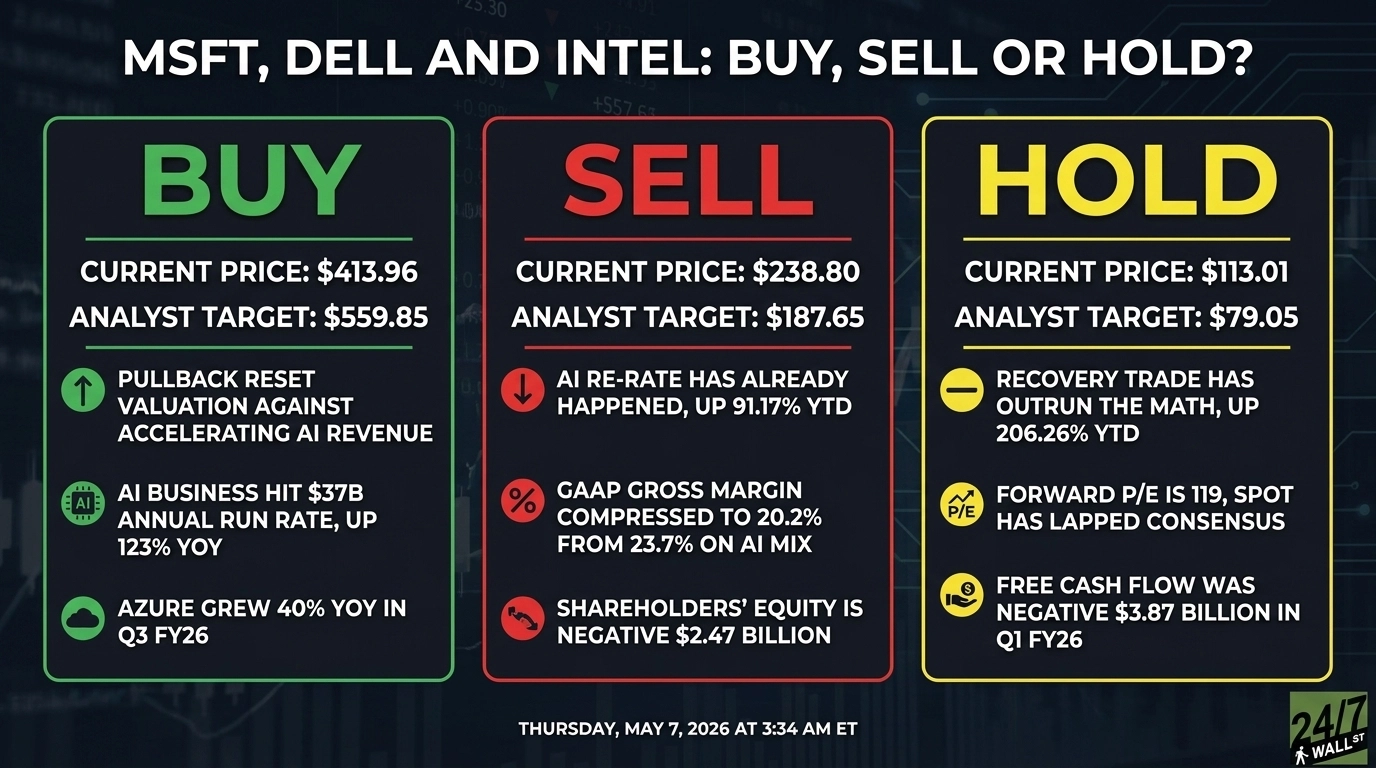

Buy Microsoft: The Pullback Has Reset the Setup

Microsoft is down 14.21% YTD and off 2.47% over the past week, even after Q3 FY26 delivered EPS of $4.27 vs. $4.07 expected and revenue of $82.89 billion, up 18.3% YoY. Azure grew 40%, Microsoft Cloud reached $54.5 billion, and the AI business hit a $37 billion annual run rate, up 123% YoY. Commercial RPO sits at $627 billion. Trailing P/E is 25 and forward P/E is 21.

Capex hit $30.88 billion, up 84% YoY, and More Personal Computing slipped 1%. Even so, analyst consensus stands at $559.85 with 9 Strong Buy, 42 Buy, 3 Hold, and 0 Sell ratings. The spread between consensus and spot is wide. Microsoft has materially outperformed the broader market over five years (+70.89%) while the recent drawdown has cooled the multiple. The pullback has reset the multiple against accelerating AI revenue.

Hold Dell: The AI Re-Rate Has Already Happened

Dell is up 91.17% YTD and 158% over one year, closing fractionally below a 52-week high of $239.45. Q4 FY26 was landmark: revenue $33.38 billion, up 40.2% YoY, AI-optimized server revenue $8.95 billion, up 342%, a $43 billion AI backlog, and FY27 guidance of $138 billion to $142 billion (up 23% at the midpoint) with AI servers near $50 billion.

The catch is the consensus. Forward P/E is 16, but the analyst target is $187.65, well below spot, with 5 Strong Buy, 14 Buy, 7 Hold, and 1 Sell. GAAP gross margin compressed to 20.2% from 23.7% on AI mix, and shareholders’ equity is negative $2.47 billion. Dell has lapped the broader market by a wide margin, but waiting for a margin trough or a guidance reaffirmation is the disciplined call.

Sell Intel: The Recovery Trade Has Outrun the Math

Intel has gone parabolic, up 206.26% YTD and 466.75% over one year, pressing a 52-week high of $113.50. Q1 FY26 was strong on the surface: non-GAAP EPS $0.29 vs. $0.0127 estimate, revenue $13.58 billion, up 7.18% YoY, DCAI up 22%, and non-GAAP gross margin 41.0%. The $5 billion NVIDIA (NASDAQ:NVDA) equity stake, the Google ASIC collaboration, and the Xeon 6 win on NVIDIA’s DGX Rubin NVL8 are real catalysts. I’m not giving an outright sell call, but it does sit at the bottom as compared to the other two companies.

The math is the problem. Trailing EPS is -$0.59, GAAP results carried a $3.73 billion net loss tied to a $4.07 billion Mobileye impairment, free cash flow was negative $3.87 billion, and forward P/E is 119. The analyst target sits at $79.05 across 48 analysts (2 Strong Buy, 11 Buy, 30 Hold, 2 Sell, 3 Strong Sell). Spot has lapped consensus targets by roughly 43%. The fundamentals improved; the price ran further. The setup looks stretched until guidance pressure-tests the rally.

Contact [email protected] for any questions or corrections.