I keep hitting the buy button on Broadcom (NASDAQ:AVGO | AVGO Price Prediction) because I have never watched a company sit this squarely on the single biggest capital cycle of my lifetime while acting like a cash-return machine for shareholders. Custom AI silicon for the handful of companies building frontier models, paired with a software business that prints money, paired with management that hands the cash back. I am long.

AI is a major draw

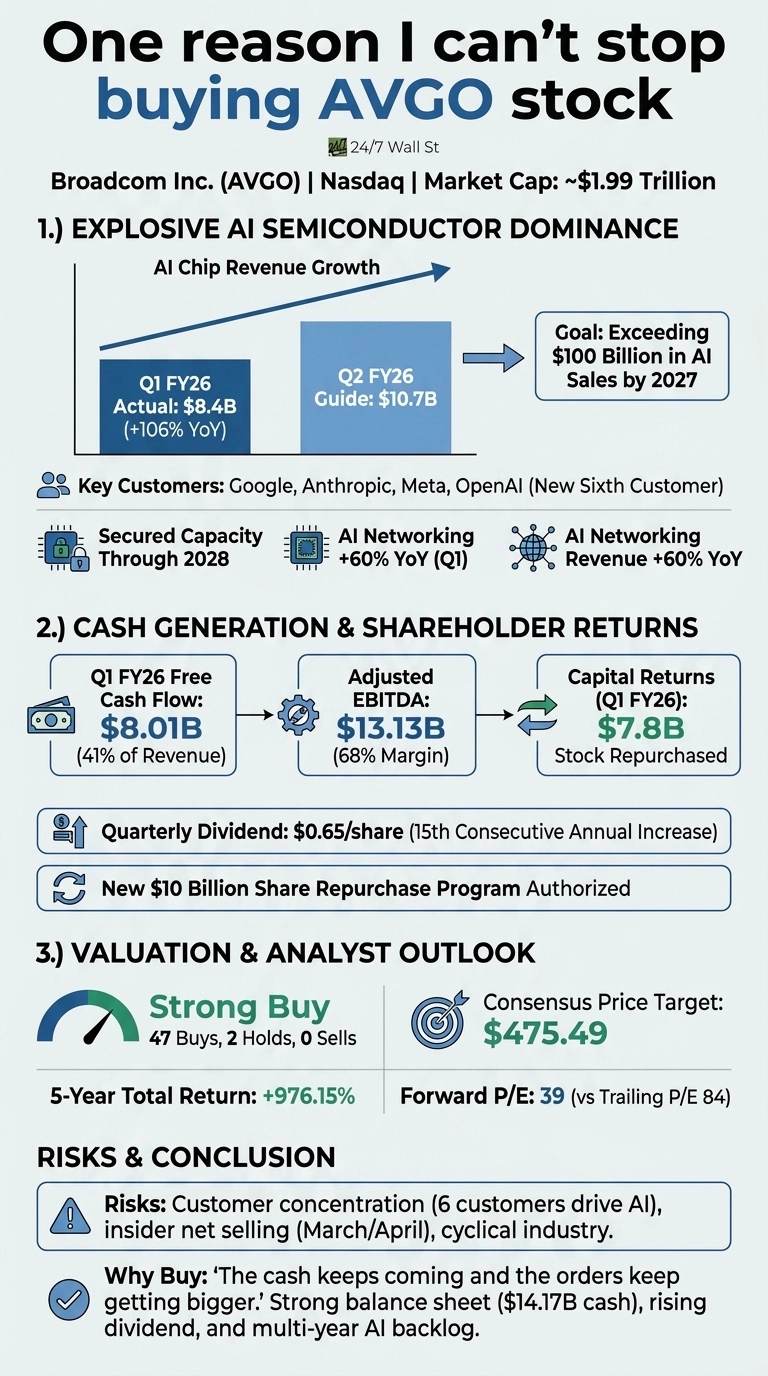

The number that pulled me in is the AI line. AI semiconductor revenue grew 106% year-on-year to $8.4 billion in fiscal Q1 2026, and management guided Q2 AI revenue to $10.7 billion. Hock Tan said it plainly on the call: “we have line of sight to achieve AI revenue from chips, just chips, in excess of $100 billion in 2027. We have also secured the supply chain required to achieve this.”

The customer list is no longer a guess. Google’s seventh-generation Ironwood TPU, Anthropic at 1 gigawatt in 2026 surging past 3 gigawatts in 2027, Meta’s MTIA scaling to multiple gigawatts, and OpenAI as a newly disclosed sixth customer expected to deploy in volume in 2027 at over 1 gigawatt. That is a multi-year backlog.

Free cash flow is mounting

Reason two is the cash. Free cash flow hit $8.01 billion in Q1, which is 41% of revenue, on adjusted EBITDA of $13.13 billion at a 68% margin. Fiscal 2025 produced $26.91 billion in free cash flow. Management is returning it aggressively.

Broadcom repurchased $7.8 billion of stock in Q1, authorized a new $10 billion buyback through year-end 2026, and raised the dividend 10% in December 2025 to $0.65 per share, the fifteenth consecutive annual increase since fiscal 2011. I am a long-term income and compounding investor. That cadence is the language I speak.

Reason three is the moat under the hood. “We have been in the silicon business for over 20 years,” Tan said, and Broadcom has fully secured capacity through 2028 on the leading-edge wafers, HBM, and substrates that every rival needs. AI networking revenue grew 60% year-on-year and is guided to 40% of total AI revenue in Q2, anchored by the Tomahawk 6 switch at 100 terabits per second.

The VMware piece throws off 93% gross margins and 78% operating margins. Sitting behind it all: a market cap near $1.99 trillion and a 976.15% five-year total return.

The risk I am not pretending away

Customer concentration is real. Six customers drive the AI franchise. If one rethinks its custom silicon plan, a quarter gets ugly. The shares do not trade cheap at a trailing P/E of 84, and insiders have been net sellers in March and April. Holding me in the position: the forward P/E of 39 against a business compounding revenue at 29% with Q2 guided to 47% growth, and contracts that already span multiple years per customer.

Why the buy button stays active

The Street agrees with the direction. 47 buy ratings against 2 holds, zero sells, and a $475.49 consensus target tell me I am not alone. I am buying a balance sheet with $14.17 billion in cash, a dividend that rises every year, and a chip business locked into the buildout of every serious AI cluster on the planet through 2028. The buy button stays active because the cash keeps coming and the orders keep getting bigger.

Contact [email protected] for any questions or corrections.