I keep buying Meta Platforms (NASDAQ:META | META Price Prediction) because I have rarely seen a business this large still compound this fast, and the market handed me a discount on the same week the company posted its biggest earnings beat in years. That is the short version. The longer version is why my finger has been on the buy button five times since the Q1 report landed.

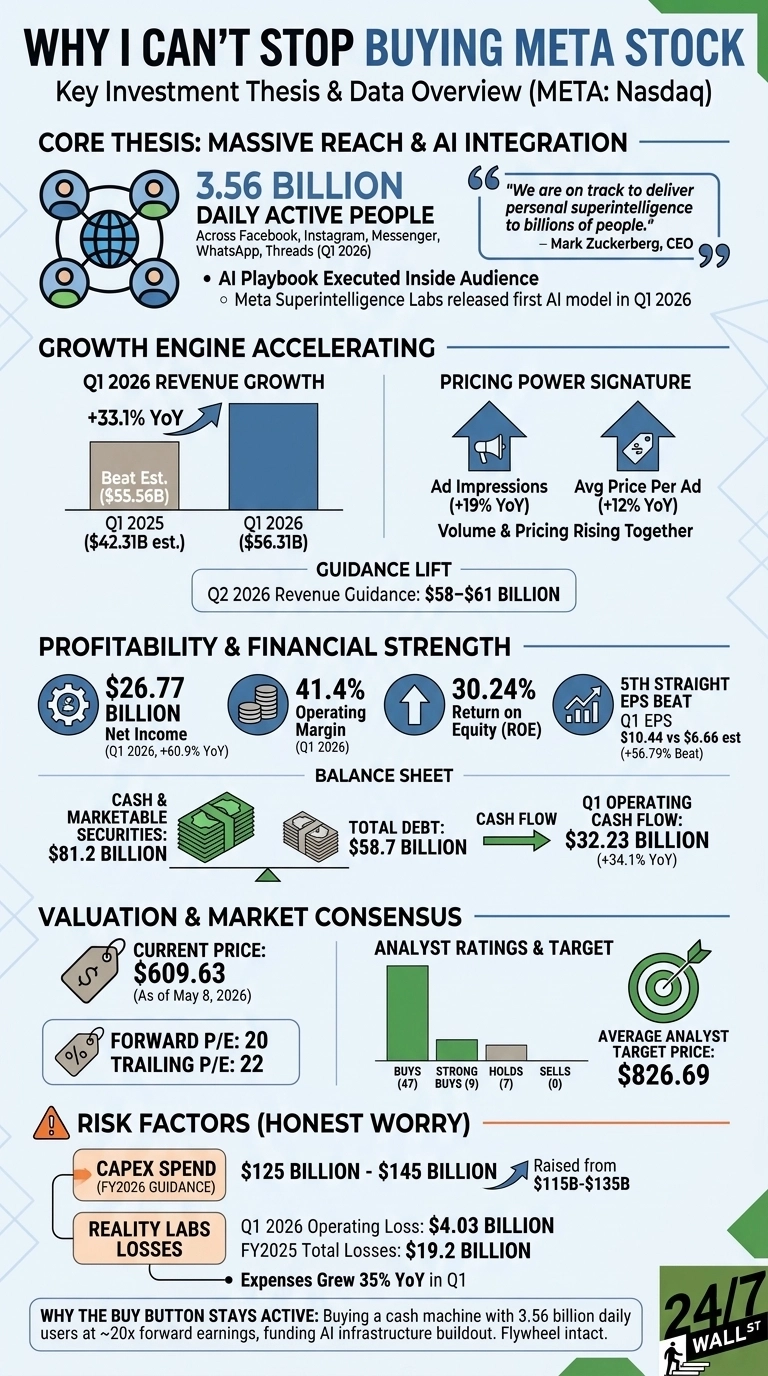

The core thesis I keep returning to is simple. Meta Platforms reaches 3.56 billion daily active people across Facebook, Instagram, Messenger, WhatsApp and Threads, and it is running the AI playbook from inside that audience rather than chasing it from outside. Mark Zuckerberg told investors on the Q1 call, “We are on track to deliver personal superintelligence to billions of people.” When a CEO with that distribution says that, I listen.

The receipts behind the conviction

First, the engine is still accelerating. Q1 2026 revenue came in at $56.311 billion, up 33.08% year over year, with ad impressions up 19% YoY and average price per ad up 12% YoY. Volume and pricing rising together is rare. That is the signature of pricing power, and it is showing up while the company is also raising guidance to $58 to $61 billion for Q2.

Second, the profitability is hard to argue with. Operating margin in Q1 sat at 41%, return on equity is 30.24%, and the balance sheet carries $81.2 billion in cash and marketable securities against $58.7 billion in total debt. Full-year 2025 operating cash flow was $115.8 billion. The company funded $26.25 billion in Class A buybacks last year and still pays a $0.53 quarterly dividend.

Third, the valuation finally met me halfway. Shares trade at $609.63, down 7.57% year to date, on a trailing P/E of 22 and a forward P/E of 20. Wall Street analysts carry an average target of $826.69, with 9 strong buys, 47 buys, 7 holds and zero sells.

The risk I will not pretend away

The honest worry is the spend. Capex guidance for 2026 climbed to $125 to $145 billion from a prior range of $115 to $135 billion, and Reality Labs lost another $4.03 billion in Q1 on top of $19.2 billion in FY2025 losses. Expenses grew 35% YoY. That is real money, and the stock fell 8.55% on earnings day precisely because the market is asking whether the return will justify it.

Zuckerberg’s framing helped me sit with it: “If we end up not needing as much as we anticipate, we can choose to bring it online more slowly or reduce our spending in future years as we grow into the capacity that we are building now.” The spend is optional in the out years. The cash flow funding it is real and already on the books.

Why the buy button stays active

Q1 net income of $26.773 billion, up 60.86% YoY, the fifth straight EPS beat, and 10 million weekly business AI conversations, up from 1 million at the start of the year, tell me the flywheel is intact. I am buying a cash machine with 3.56 billion daily users at 20x forward earnings while it builds the rails for whatever AI becomes. I will keep buying until that math changes.

Contact [email protected] for any questions or corrections.