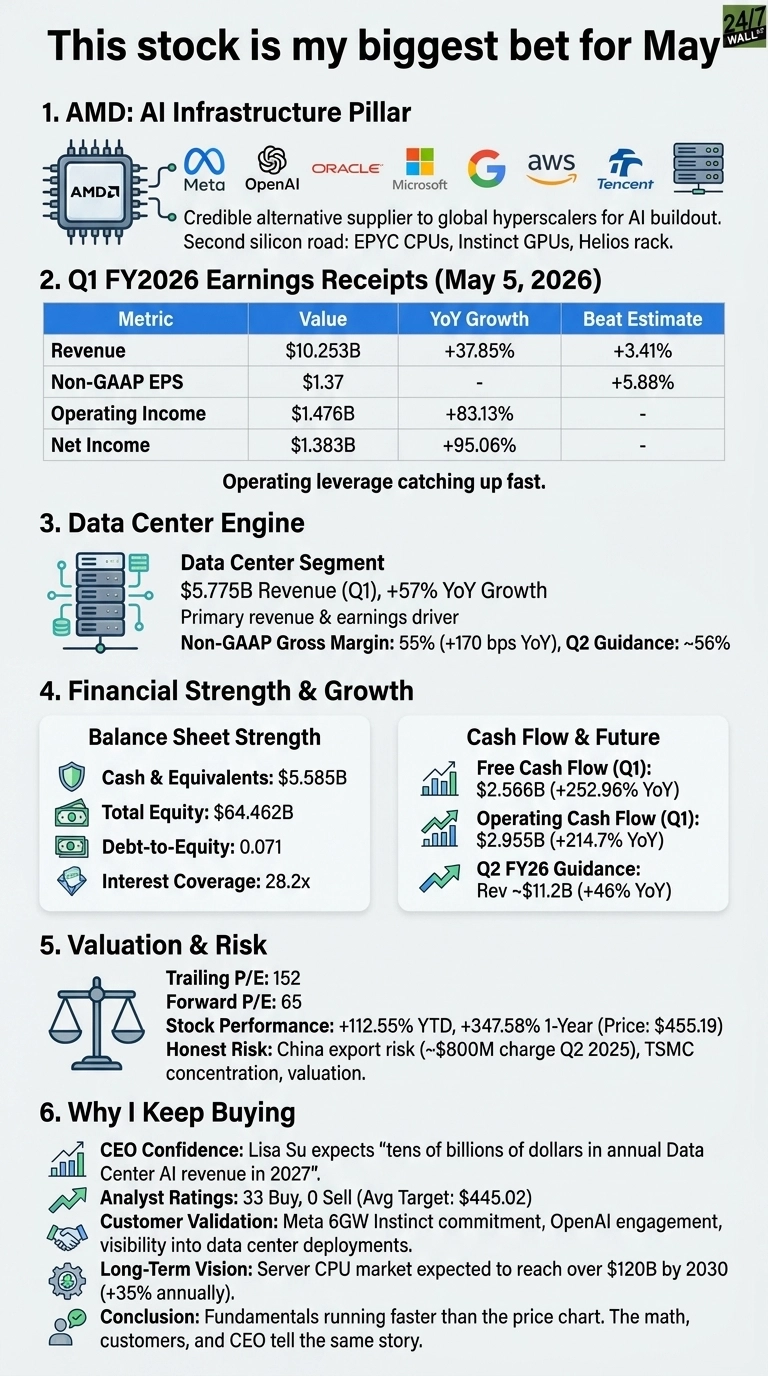

I bought more Advanced Micro Devices (NASDAQ:AMD | AMD Price Prediction) again last week, and I am not embarrassed to say it was my biggest single buy of the year. AMD is the position I keep funding because Lisa Su has quietly turned this company into the second pillar of the AI infrastructure buildout, and the receipts from May 5, 2026 only made the case louder.

What pulls me back to the buy button is simple: AMD is the only credible alternative supplier to the world’s hyperscalers at the exact moment those hyperscalers refuse to be single-sourced. Meta, OpenAI, Oracle, Microsoft, Google, AWS, Tencent. They all need a second silicon road, and AMD is paving it with EPYC CPUs, Instinct GPUs, and the Helios rack. That is the thesis in one breath.

The receipts

Q1 FY2026 revenue came in at $10.253 billion, up 37.85% year over year, beating the estimate by 3.41%. Non-GAAP EPS of $1.37 beat by 5.88%. Operating income rose 83.13% and net income 95.06% on that 38% top line. That is operating leverage I will pay up for.

The Data Center segment did $5.77 billion, up 57% year over year, and it is now the engine. Non-GAAP gross margin landed at 55%, up 170 basis points YoY, with Q2 guided to 56%. Free cash flow more than tripled to $2.56 billion, up 252.96%.

The balance sheet keeps me sleeping at night. Debt-to-equity sits at 0.071, interest coverage at 28.2, with $5.58 billion in cash against $64.46 billion in equity. There is no leverage time bomb here.

Then there is the TAM math from the call. Lisa Su said the server CPU market should now grow at “greater than 35% annually, reaching over $120 billion by 2030”, with CPU-to-GPU ratios moving from 1:8 toward 1:1. She also said the company has a “clear path to exceed our long-term financial targets, including delivering more than $20 in EPS over the strategic time frame.” Pair that with Q2 guidance of roughly $11.2 billion in revenue at 46% YoY growth, and the trajectory speaks for itself.

The honest risk

Valuation is real. The trailing P/E sits at 152 and forward at 65. The stock has run 112.55% year to date and 347.58% over one year to $455.19.

Layer on the China export risk that produced $800M in MI308 inventory charges in Q2 2025, and TSMC concentration, and the picture is not riskless. What keeps me buying through that is the cash flow conversion. Operating cash flow grew 214.7% YoY. Earnings are catching the multiple, fast.

Why the buy button stays active

Su told the Street she has “strong and increasing confidence in our ability to deliver tens of billions of dollars in annual Data Center AI revenue in 2027” and visibility down to which data centers the GPUs will sit in. Meta’s 6 gigawatt Instinct commitment and the OpenAI engagement are scheduled shipments with named delivery windows. Wall Street still lists 33 Buy ratings and zero Sells, and the analyst target sits at $445.02.

Mizuho raised the firm’s price target on AMD to $515 from $415 and keeps an Outperform rating on the shares.

I am building a position I plan to hand my future self, and AMD is the rare stock where the fundamentals are running faster than the price chart. I keep buying because the math, the customers, and the CEO are all telling me the same story.

Contact [email protected] for any questions or corrections.