The memory rally has been one of the most extraordinary moves of the cycle, and SanDisk (NASDAQ:SNDK | SNDK Price Prediction) sits at the center of it. After a 3,197% gain over the past year and a 482% year-to-date run, the question is whether fundamentals can keep up with the multiple.

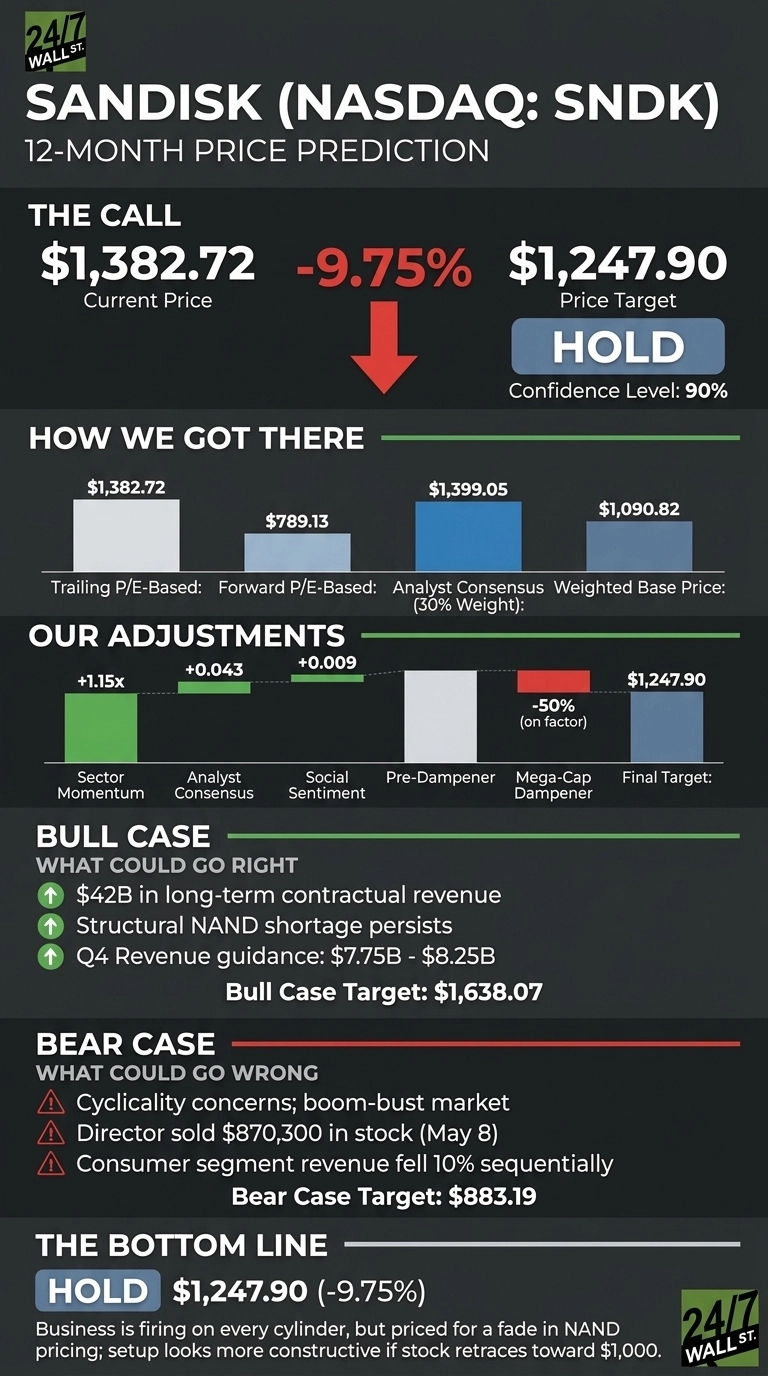

Our 24/7 Wall St. price target for SanDisk is $1,247.90, implying roughly 9.75% downside from $1,382.72. The recommendation is hold, with high model confidence of 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $1,382.72 |

| 24/7 Wall St. Price Target | $1,247.90 |

| Upside/Downside | -9.75% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Our 24/7 Wall St. price target sits below where SanDisk trades today. The stock has real catalysts: $42 billion in long-term contractual revenue from five new hyperscaler agreements and a structural NAND shortage analysts expect to persist through 2028 could push it well past our model. Susquehanna’s $2,000 price target shows how aggressive the bull case can get. Consider our target one datapoint among many.

From $41 to $1,382 in Twelve Months

The rally has been violent and earnings-driven. Q3 FY26 reported April 30, 2026, delivering EPS of $23.41 versus $14.66 consensus on revenue of $5.95 billion, up 251% year over year.

Datacenter revenue alone hit $1.467 billion, up 645%, and gross margin expanded from 22.5% to 78.4%. The stock is up 46.4% in the past month, though it pulled back 4.46% on May 14 as retail sentiment cooled.

The Case for $1,600 and Beyond

Bulls have a clean thesis. CEO David Goeckeler called Q3 “a fundamental inflection point” with a shift toward multi-year, financially committed customer engagements. Q4 guidance of $7.75 billion to $8.25 billion in revenue and $30 to $33 in non-GAAP EPS implies continued acceleration.

Mizuho’s $1,625 target, Melius Research’s $1,350, and Susquehanna’s $2,000 all rest on AI memory demand extending through the decade. Our internal bull case lands at $1,638.07 over twelve months, an 18% gain, and the 52-week high already touched $1,600.

What Could Go Wrong

The bear case starts with cyclicality. NAND has historically been a boom-bust market, and SanDisk’s forward P/E of 24x already prices in sustained pricing power. Our bear scenario sees $883.19, a 36% drawdown. Consumer segment revenue fell 10% sequentially in Q3, hyperscaler concentration is rising, and the Kioxia partnership is a strategic dependency.

Director Necip Sayiner sold $870,300 in stock on May 8. The sale represented restricted stock vesting and a small fraction of his holdings. Barclays remains at hold with a $1,200 target.

SanDisk Price Prediction 2026-2030

The 24/7 Wall St. price target of $1,247.90 with 90% confidence reflects a business firing on every cylinder priced for a fade in NAND pricing. The setup looks more constructive if the stock retraces toward $1,000 or if a sixth NBM agreement lands with another hyperscaler.

Caution is warranted if NAND spot pricing rolls over or if Q4 guidance comes in below the $8 billion midpoint. For now, our model lands at HOLD.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $1,247.90 |

| 2027 | $1,290 |

| 2028 | $1,310 |

| 2029 | $1,330 |

| 2030 | $1,255 |

These projections assume SanDisk converts hyperscaler demand into multi-year revenue and NAND pricing stays disciplined. Significant upside could come from HBF adoption in AI inference, while a return to traditional memory cyclicality remains the biggest swing factor.

Contact [email protected] for any questions or corrections.