Few stories in the 2026 market rival the SanDisk (NASDAQ:SNDK | SNDK Price Prediction) run. The stock has gone from a sleepy Western Digital spinoff to a pure-play AI memory supercycle bet, posting a 3,460.95% gain over the past year. With the stock now trading near $1,380.93, the question is whether the move has more runway or the easy money has already been made.

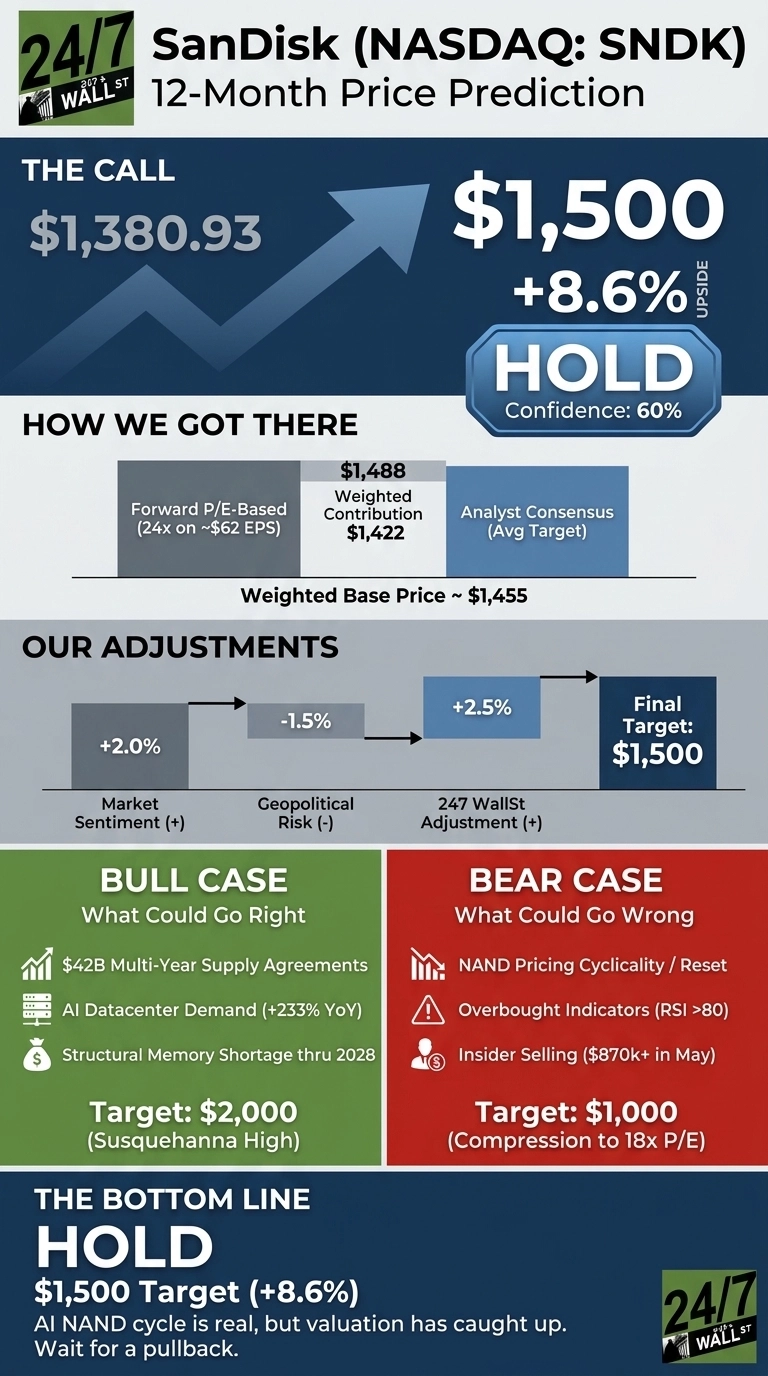

Our 24/7 Wall St. price target for SanDisk is $1,500, implying roughly 8.6% upside over the next 12 months. We rate the stock a hold with 60% confidence. The AI NAND cycle is real, but valuation has caught up to the story.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $1,380.93 |

| 24/7 Wall St. Price Target | $1,500 |

| Upside | 8.6% |

| Recommendation | HOLD |

| Confidence Level | 60% |

A Parabolic Run Meets a Blowout Quarter

SanDisk is up 401.72% year to date and 49.94% over the past month, though the stock has cooled 10.77% over the past week as profit-takers stepped in.

The catalyst was a Q3 FY26 report: revenue of $5.95 billion, up 251% year over year, and non-GAAP EPS of $23.41 against a $14.66 consensus, a 59.69% beat. Gross margin expanded to 78.4% as Datacenter revenue surged 233% sequentially, and management guided Q4 revenue to $7.75B to $8.25B. The company also signed $42 billion in newly signed multi-year supply agreements and maintains a zero long-term debt balance sheet.

The Case for $2,000

Bulls have ample ammunition. Susquehanna’s $2,000 target is the Street high, with Mizuho at $1,625 on a Buy rating. The bull thesis rests on a structural memory shortage running through 2028, the BiCS8 technology ramp, and High Bandwidth Flash for AI inference.

CEO David Goeckeler called the quarter “a fundamental inflection point” driven by mix shift into Datacenter, the highest-margin end market. If FY27 EPS approaches $90 and the market awards a 25x multiple, fair value clears $2,200.

What Could Go Wrong

NAND has always been cyclical, and a price reset would compress the 79% to 81% gross margin guide quickly. Barclays maintains a Hold at $1,200, implying mid-teens downside. The consumer segment already declined 10% sequentially, and insider selling has picked up, including a $870,300 open-market sale by a director in early May.

Bulls counter that most insider activity reflects routine tax withholding and estate planning near record highs, and that the $42 billion in firm contracts cushions any pricing reset. If sentiment turns and the multiple compresses to 18x on $55 of FY27 EPS, downside lands closer to $1,000.

Hold for Now, but Keep It on the List

The 24/7 Wall St. price target of $1,500 reflects a stock that has priced in substantial good news. The setup improves if SanDisk pulls back into the $1,100 to $1,200 range or delivers another guide-raise next quarter. Caution is warranted if NAND spot pricing softens or if histogram exhaustion in MACD confirms a broader trend reversal. The story is real. The entry price matters.

Our model projects SanDisk could trade in the coming years, assuming current growth trajectories and AI memory demand hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $1,500 |

| 2027 | $1,725 |

| 2028 | $1,925 |

| 2029 | $2,050 |

| 2030 | $2,200 |

These projections assume SanDisk continues executing on its Datacenter mix shift and NAND pricing remains structurally tight. Significant upside or downside could result from the timing of the next memory down-cycle.

Contact [email protected] for any questions or corrections.