SanDisk (NASDAQ:SNDK | SNDK Price Prediction | SNDK Price Prediction) has done something almost no mega-cap technology stock does. It went up 3,807.74% in twelve months. The NAND flash spinoff from Western Digital is now a $218.9 billion AI memory pure-play, with the Datacenter segment growing 645% year over year in Q3 FY2026 and gross margins exploding to 78.4% from 22.5% a year earlier.

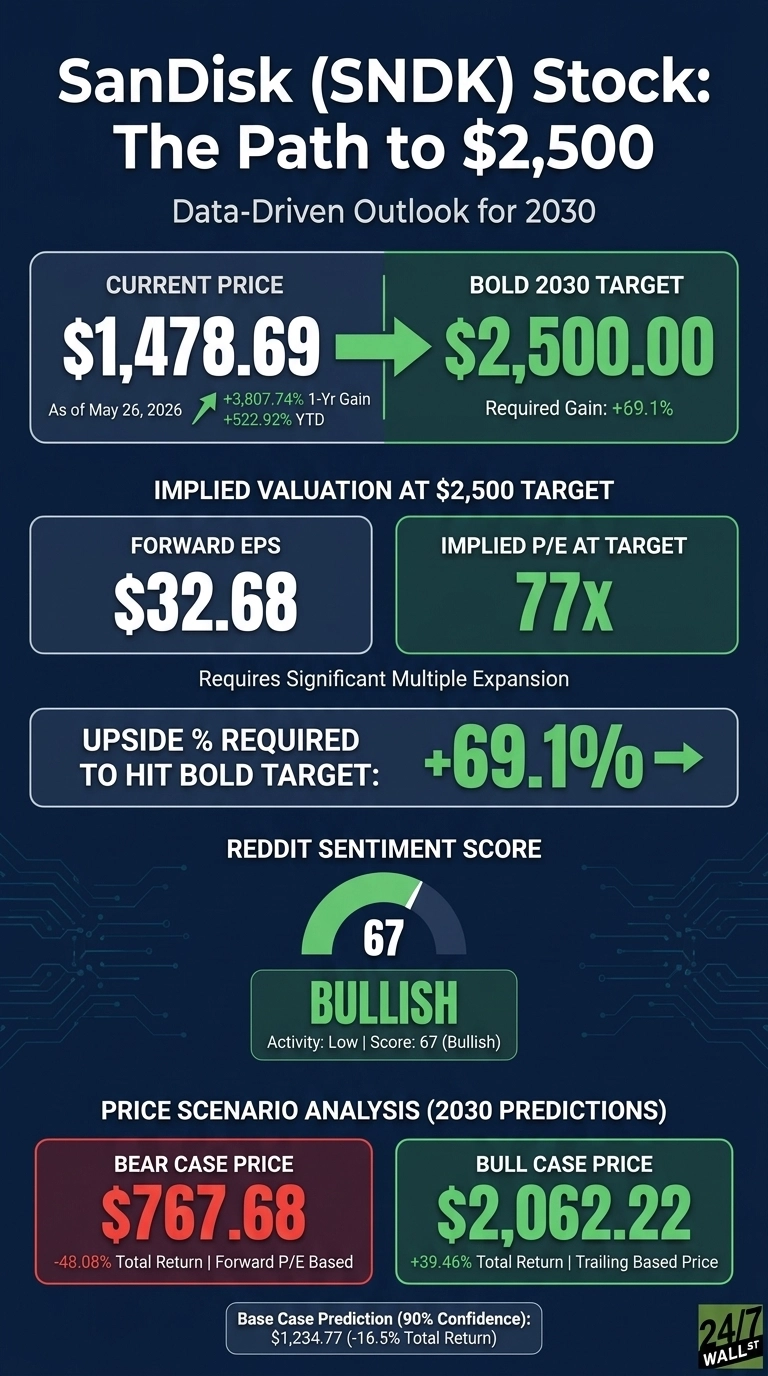

SanDisk is up 522.92% year to date. Can SNDK hit $2,500 by 2030?

Why SanDisk Shares Have Cooled Off This Month

Shares hit a 52-week high of $1,600 before pulling back to 7% below that mark. The most recent trading day was a -4.12% drop. With a one-week gain of 5.05% and one-month surge of 51.03%, investors are digesting whether this rally has run too far. The trailing 12-month P/E sits at 51, including loss quarters from the prior year. The question: is the structural margin story durable, or did NAND pricing simply overshoot?

Wall Street Sees Modest Upside. Our Model Sees a Pullback

Consensus is bullish but stretched. The Wall Street analyst target is $1,493.36, basically flat with today’s price. The rating distribution: 2 Strong Buy, 14 Buy, 4 Hold, 0 Sell, and 1 Strong Sell, with 76% bullish sentiment.

Our base case 2030 price is $1,234.77 (a -16.5% total return) at 90% confidence. The bull case lands at $2,062.22 and the bear case at $767.68. The model’s mega-cap dampener strips 50% of upside contribution. If the New Business Model contracts hold, that dampener is too punitive.

The Path to $2,500 Per Share

Reaching $2,500 from today’s price of $1,478.69 requires a gain of 69.1%. With forward EPS of $32.68, a price of $2,500 implies a forward P/E of 77x. Our base case of $1,234.77 already implies 48x, meaning the bold target needs roughly 29x of additional multiple expansion.

That sounds steep until you look at the earnings trajectory. Q4 FY2026 guidance calls for revenue of $7.75 billion to $8.25 billion and Non-GAAP EPS of $30 to $33. The implied annualized EPS run rate is around $93.64. If EPS compounds through 2030, the forward multiple compresses sharply.

CEO David Goeckeler called this “a fundamental inflection point for Sandisk” driven by Datacenter, and noted “multi-year customer engagements backed by firm financial commitments” with five signed NBM agreements. The primary risk is a NAND pricing reversal that pulls margins back toward historical norms before 2028.

Where SanDisk Trades Today vs Its Earnings Power

Today’s forward P/E is 45x against forward EPS of $32.68. The Alpha Vantage forward P/E reads 23 on a different EPS assumption, suggesting consensus may be too low. Shares trade between a 52-week low of $36.21 and high of $1,600, with 2,942.57% returns since separation. If Datacenter EPS compounds at half the recent pace, today’s multiple looks cheap.

Can SanDisk Really Hit $2,500? My Verdict

$2,500 by 2030 requires a 69.1% gain from here. A stretch, but defensible.

Three things must break right. NAND pricing power must hold through the structural memory shortage that analysts expect to persist through 2028. The New Business Model must scale beyond five contracts and lock in firm hyperscaler commitments.

BiCS8 and High Bandwidth Flash ramps must translate into AI inference design wins. A NAND price collapse or Kioxia partnership disruption would derail it. We’ve outlined the blueprint for how SanDisk could reach $2,500 in 2030.

Contact [email protected] for any questions or corrections.