I’m putting a fresh stake in the ground on Alibaba (NYSE:BABA | BABA Price Prediction) after a messy but strategically important quarter. Alibaba is sacrificing near-term profitability to scale its AI and cloud franchise, and the market is still digesting what that trade-off means. My read: the setup is constructive, even if the headline numbers look ugly.

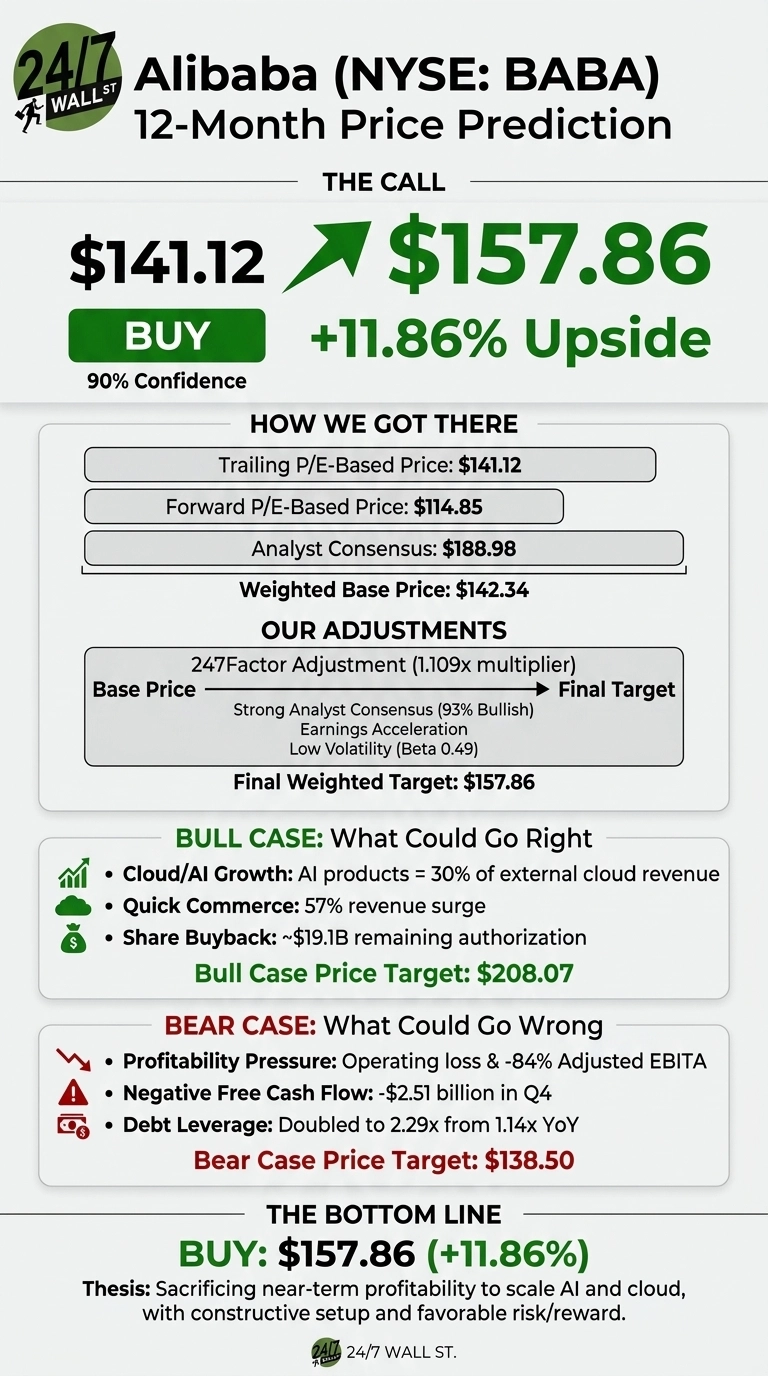

Our 24/7 Wall St. price target for Alibaba is $157.86 over the next 12 months, implying 11.86% upside from $141.12. Our model rates the stock a buy with high confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $141.12 |

| 24/7 Wall St. Price Target | $157.86 |

| Upside | 11.86% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Quarter That Reframed the Story

Alibaba reported fiscal Q4 2026 on May 13, 2026. Revenue came in at $35.28 billion, up 3% year over year, with EPS of $0.09. Adjusted EBITA fell 84% to $740 million and free cash flow swung to negative $2.51 billion. The market’s reaction was muted: shares closed at $141.12, down 3.22% on the session.

Alibaba Cloud grew 38% to $6.04 billion, with external revenue accelerating to 40% growth. AI-related products now represent 30% of external cloud revenue, marking the eleventh consecutive quarter of triple-digit AI growth. Quick commerce (Taobao Instant Commerce and Ele.me) surged 57%. Shares are up 7.44% over the past month and 7.08% over the past year, though still 3.72% lower year to date.

The Case for $200+

Bulls have a credible roadmap. The Street’s average target sits at $188.98, with 31 Buy and 8 Strong Buy ratings. Our bull-case scenario points to $208.07 within 12 months. The drivers: Qwen LLM with 300 million monthly active users, over 100,000 Zhenwu PPU AI chips deployed, and Alibaba Cloud holding 35.8% of China’s AI cloud market.

CEO Eddie Wu summed up the posture: “Alibaba’s full-stack AI investments have progressed from incubation to commercialization at scale.” A $19.1 billion remaining buyback authorization through March 2027 adds a floor.

The Risks Worth Watching

Operating income swung to a $123 million loss and total debt-to-EBITDA doubled to 2.29x from 1.14x. Capex hit $3.90 billion in the quarter, and Alibaba raised $3.2 billion in convertible notes plus HK$12 billion in exchangeable bonds. Customer Management revenue grew just 1% headline, suggesting the core e-commerce engine is cooling. Our bear-case path lands at $138.50.

That said, bulls would argue these are deliberate choices. The 84% EBITA decline reflects user-acquisition spend on the Qwen app and quick commerce. On a like-for-like basis stripping out subsidy reclassification, customer management revenue grew 8%.

Alibaba Price Prediction 2026-2030

My 24/7 Wall St. price target stays at $157.86 with a buy rating and 90% confidence. The tipping factor is AI commercialization velocity at the cloud unit. The thesis strengthens if cloud growth holds above 35% and quick commerce unit economics keep improving. The thesis weakens if free cash flow stays negative through fiscal 2027 and debt leverage drifts past 3x.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $157.86 |

| 2027 | $172 |

| 2028 | $185 |

| 2029 | $197 |

| 2030 | $208.73 |

These projections assume Alibaba executes on its AI and cloud strategy. Material upside or downside could come from US-China policy shifts or a sharper-than-expected pivot back to GAAP profitability.

Contact [email protected] for any questions or corrections.