Few mega-caps have shifted the narrative as decisively as Google (NASDAQ:GOOG | GOOG Price Prediction) has over the past year. After a 138.92% one-year run and a 26.65% year-to-date gain, the real question is whether the market has fully priced what comes next. Our model says it has not.

Our 24/7 Wall St. Price Target for Google

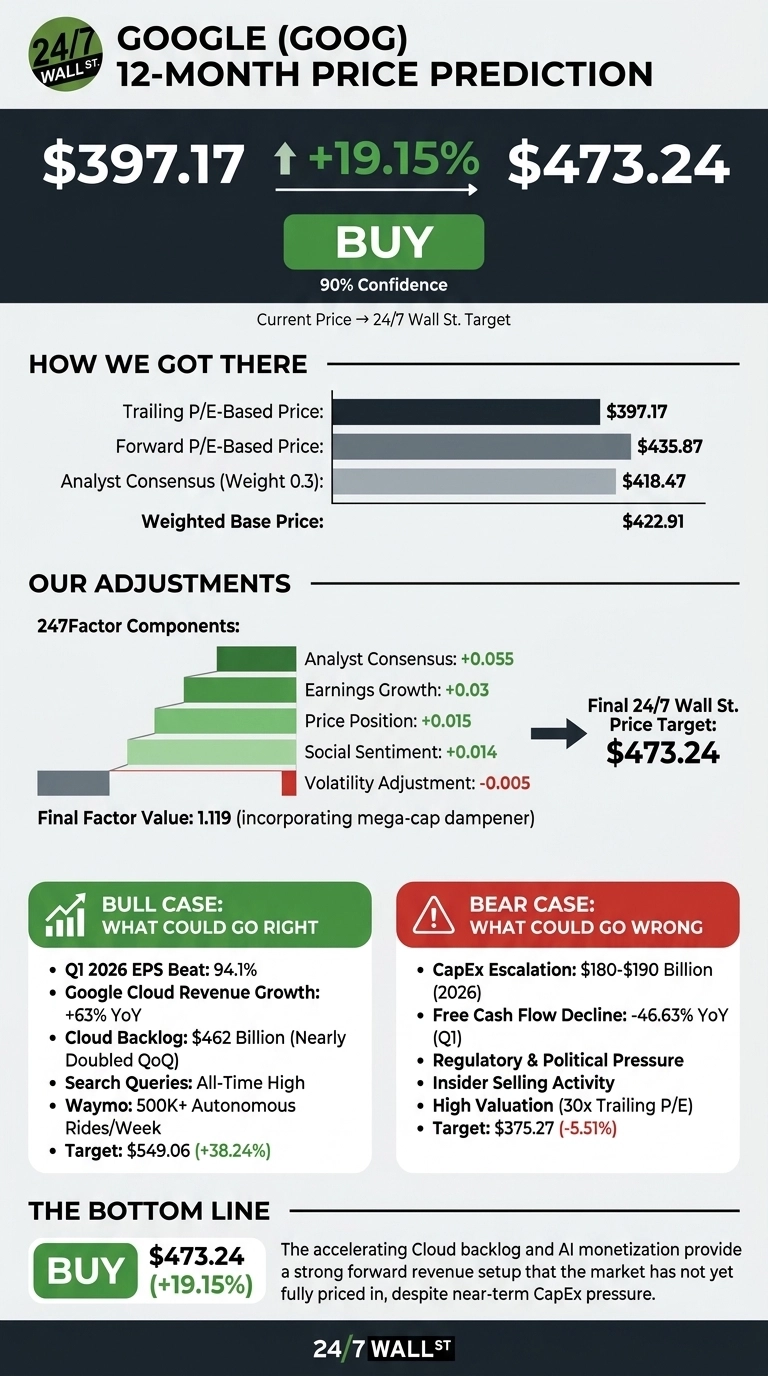

Google trades at $397.17. Our 24/7 Wall St. price target for Google is $473.24, implying 19.15% upside over the next 12 months. The recommendation is buy, with a 90% confidence level, supported by accelerating cloud growth, AI monetization across Search, and a still-reasonable forward multiple.

| Metric | Value |

|---|---|

| Current Price | $397.17 |

| 24/7 Wall St. Price Target | $473.24 |

| Upside | 19.15% |

| Recommendation | BUY |

| Confidence Level | 90% |

What Just Happened: A Blowout Q1 and a Cloud Backlog Explosion

Google posted a 94.1% EPS beat in Q1 FY2026, with revenue of $109.9 billion, up 21.79% year-over-year. Google Cloud revenue jumped 63% to $20.028 billion, with backlog nearly doubling sequentially to $462 billion. Shares moved +9.97% on the earnings report, then kept climbing. The stock now sits within 5% of its $399.93 52-week high, with the 200-day moving average at $289.27.

Reddit’s r/stocks thread “GOOG ain’t done yet” captured the retail tone, while Egerton Capital added 2.38 million shares and ARK Invest added 174,522 shares this month.

The Case for $549 and Beyond

Our bull case targets $549.06, a 38.24% return. The thesis rests on three legs. First, Cloud operating income tripled YoY with margins expanding from 17.8% to 32.9%, and Pichai noted GenAI product revenue grew nearly 800% year-over-year.

Second, Search queries hit an all-time high, with AI Overviews monetizing better than the bears expected and ads relevance improving by nearly 10%.

Third, Waymo crossed 500,000 autonomous rides per week, and the SpaceX orbital data center talks hint at the kind of infrastructure optionality Wall Street rarely models. With 60 buy ratings and zero sells across 66 analysts, the consensus is leaning in.

The Risks Worth Watching

Our bear case lands at $375.27, a modest 5.51% drawdown. CapEx is the headline risk: $180 billion to $190 billion in 2026, with 2027 set to climb further. Free cash flow fell 46.63% YoY in Q1.

Bulls would counter that $35.674 billion in quarterly infrastructure spend underwrites the $462 billion backlog, half of which converts to revenue within 24 months.

Other risks include Senator Warren’s investigation into AI data center energy, a Waymo recall of 3,791 robotaxis, and a Form 144 filing for 409,000 Sergey Brin-linked shares. Valuation at a 30x trailing P/E and 28x forward leaves no slack for a miss.

Google Price Prediction 2026-2030

The 24/7 Wall St. price target sits at $473.24 with confidence at 90%. The tipping factor is Cloud backlog: $462 billion with management compute-constrained is a forward revenue setup the Street has not fully digested.

The bullish setup strengthens if Cloud growth holds above 50% next quarter. The thesis weakens if 2027 CapEx blows past $250 billion without commensurate backlog conversion.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $473 |

| 2027 | $528 |

| 2028 | $585 |

| 2029 | $635 |

| 2030 | $683 |

These projections assume Google continues converting Cloud backlog and defending Search share against AI-native competitors. Material upside could come from Waymo commercialization or TPU external sales; material downside could come from regulatory action on AI energy use or a step-change in CapEx without revenue follow-through.

Contact [email protected] for any questions or corrections.