Visa (NYSE:V | V Price Prediction) and Mastercard (NYSE:MA) just closed the books on calendar Q1 2026, and both networks beat expectations while pulling toward different strategic frontiers. Visa is selling itself as a “payments hyperscaler”. Mastercard is leaning into agentic commerce and stablecoins. The same swipe economy, two very different bets on what comes next.

Data Processing Carries Visa. Services Carry Mastercard.

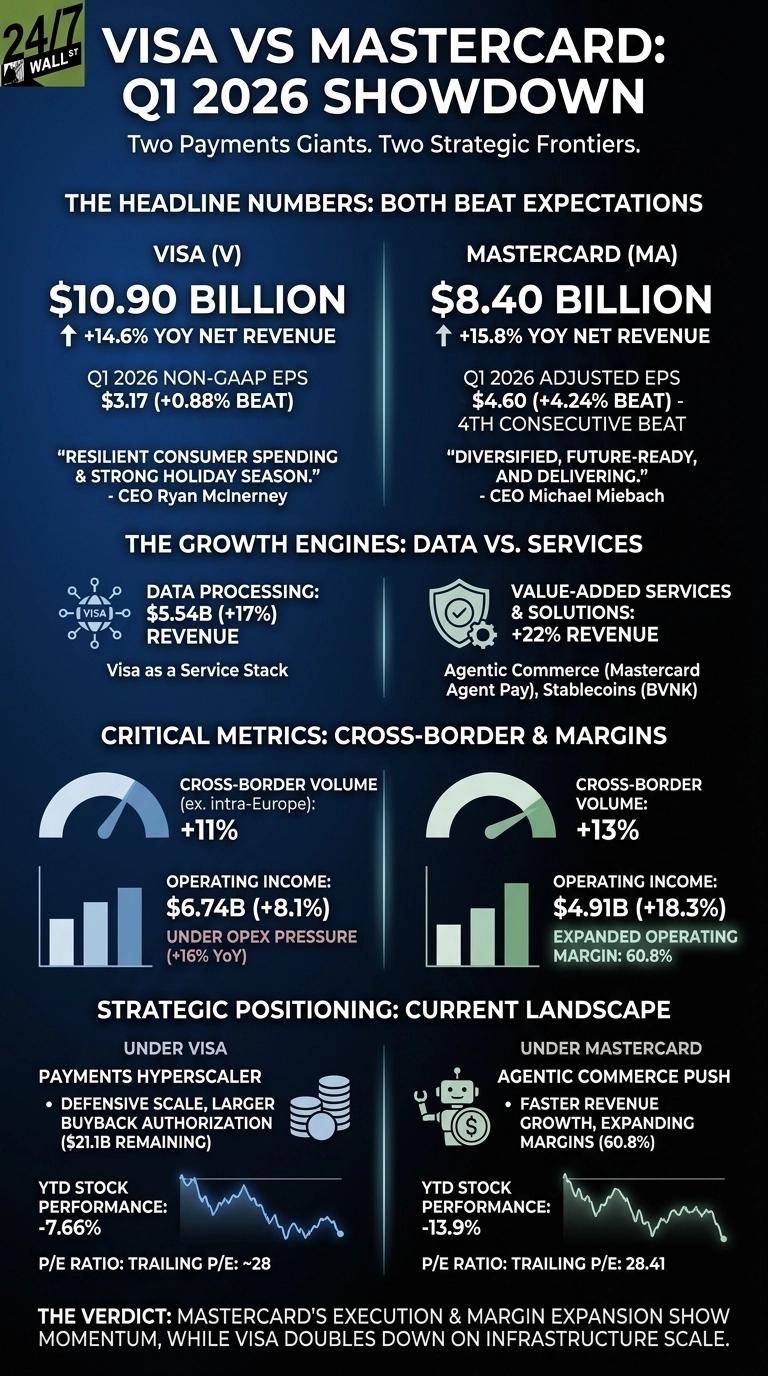

Visa pulled in $10.90 billion in net revenue, up 14.6% year over year, with Data Processing the standout at $5.544 billion and 17% growth. That is the engine, the rails Visa rents to issuers, fintechs, and merchants. Non-GAAP EPS came in at $3.17, a hair above the $3.1423 consensus. A clean beat, if not a thunderclap.

Mastercard ran hotter on the top line. Net revenue of $8.398 billion rose 15.83%, and adjusted EPS of $4.60 sailed past the $4.41 Street view, its fourth straight beat. The real story is Value-Added Services and Solutions, up 22%, with cyber, loyalty, and consulting now meaningfully pulling the wagon alongside the core network.

| Driver | Visa | Mastercard |

| Lead Segment Growth | Data Processing +17% | Value-Added Services +22% |

| Cross-Border Volume | +11% ex-Europe | +13% local |

| Operating Margin | Under opex pressure | 60.8%, expanded |

CEO Ryan McInerney framed Visa’s quarter around “resilient consumer spending and a strong holiday season”. Michael Miebach struck a different chord, calling Mastercard “diversified, future-ready, and delivering”. Visa sounds like a utility scaling up. Mastercard sounds like a product company chasing new buying centers.

One Builds the Stack. The Other Buys the Future.

Visa is doubling down on its own infrastructure, what McInerney calls the “Visa as a Service stack”, anchored in tokenization, real-time money movement, and AI-driven commerce. Mastercard is buying its way into the next layer.

The planned BVNK acquisition extends stablecoin rails, while Mastercard Agent Pay targets AI agents transacting on behalf of consumers. Both stories are credible. Mastercard’s feels more urgent.

Litigation tone also differs. Visa absorbed another $707 million interchange MDL provision, the latest in a long string. Mastercard booked a $202 million restructuring charge and continues to flag U.S. merchant class opt-outs. Neither overhang is going away soon.

The Next Test Is Cross-Border and Margins

I will be watching whether Visa’s Data Processing momentum can outrun the 16% YoY opex growth that is squeezing operating leverage.

For Mastercard, the question is whether services can keep compounding above 20% and whether Agent Pay produces actual transactions, not just headlines. Cross-border travel patterns, currently running stronger for Mastercard at +13%, will likely decide which network shows the bigger beat next quarter.

Where Mastercard Looks Stronger Right Now

If you want the larger, steadier rails business with a fatter buyback authorization at $21.1 billion and a lower trailing P/E near 28, Visa fits the defensive profile, and that case is reasonable.

But Mastercard’s setup looks stronger here. Faster revenue growth, an expanding 60.8% operating margin, and a sharper push into agentic commerce read like a company widening its moat while the other defends one. The stock is also down 13.9% year to date, which softens the valuation question.

If input from new initiatives stalls or interchange rulings escalate, I would reassess. For now, Mastercard’s quarter showed a business doing more with less, and that is the kind of execution worth tracking closely.

Contact [email protected] for any questions or corrections.