If you have $2,500 to put into payments networks today, the choice between Visa (NYSE:V | V Price Prediction) and Mastercard (NYSE:MA) is sharper than usual.

Both just posted Q1 FY2026 results that beat estimates, both leaned on resilient cross-border spending, and both rolled out new platforms aimed at agentic commerce and stablecoins. The businesses, however, are pulling in different directions.

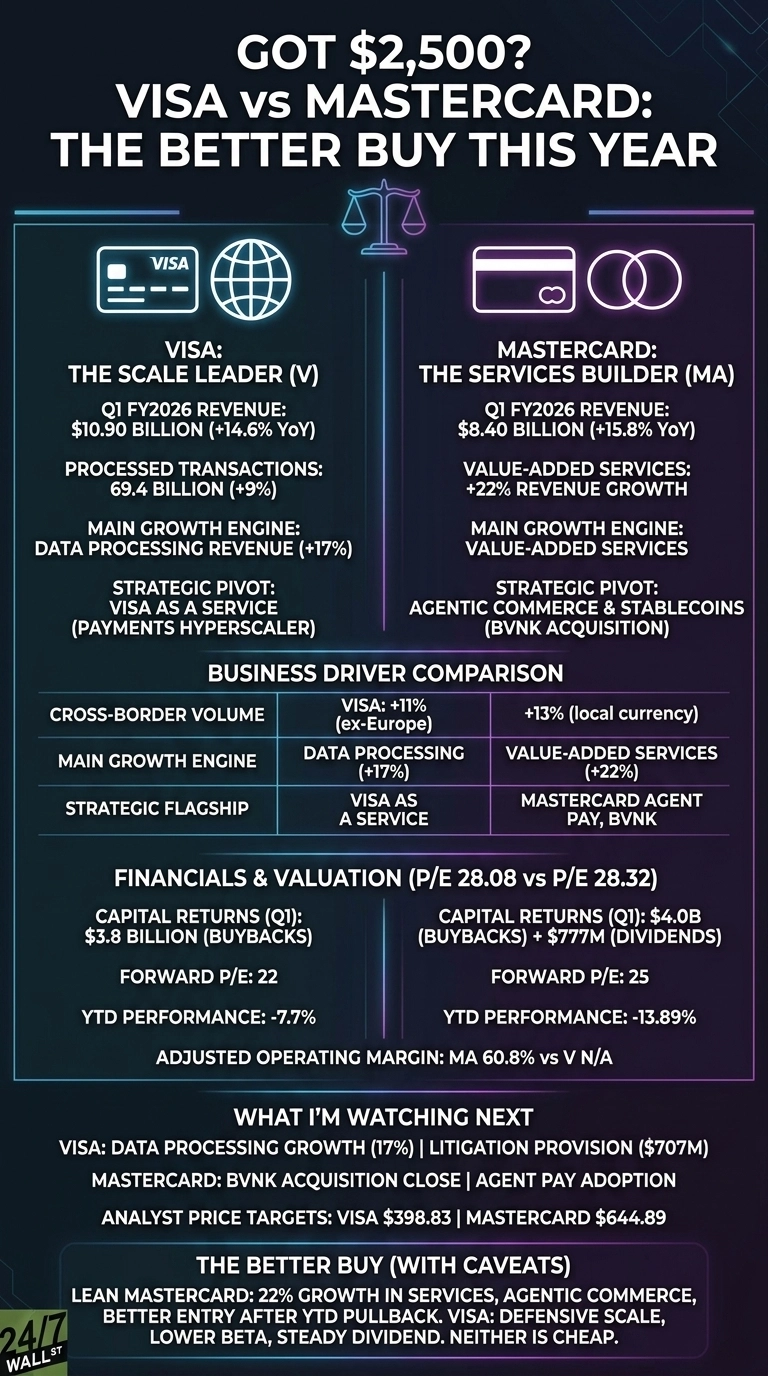

Cross-Border Strength Carried Both, But the Mix Differs

Visa’s quarter, reported January 29, 2026, delivered net revenue of $10.90 billion, up 14.6% year over year, with non-GAAP EPS of $3.17. The standout line was Data Processing Revenue at $5.544 billion, up 17%, which is the network’s highest-margin engine.

CEO Ryan McInerney framed the platform pivot directly: “Our purposeful investments in our Visa as a Service stack continue to position us as a payments hyperscaler.” A $707 million litigation provision tied to the interchange MDL case continues to weigh on GAAP results.

Mastercard’s quarter, reported April 30, 2026, landed net revenue of $8.40 billion, up 15.8%, with adjusted EPS of $4.60, a 4.24% beat. The real story is Value-Added Services and Solutions, up 22% year over year.

CEO Michael Miebach pointed to two specific bets: “advancing agentic commerce with Mastercard Agent Pay and expanding our stablecoin solutions through the planned acquisition of BVNK.”

Scale Leader vs. Services Builder

Visa is the heavyweight, with $613.1 billion in market cap and 69.4 billion processed transactions in the quarter alone. The buyback machine repurchased roughly 11 million shares for $3.8 billion.

Mastercard plays the higher-growth, higher-margin role. Adjusted operating margin reached 60.8%, up from 59.3%, and capital returns totaled $4 billion in buybacks plus $777 million in dividends. A $202 million restructuring charge and Pillar 2 tax pressure complicate the bottom line.

| Business Driver | Visa | Mastercard |

| Cross-border volume growth | +11% ex-Europe | +13% local currency |

| Main growth engine | Data Processing (+17%) | Value-Added Services (+22%) |

| Strategic flagship | Visa as a Service | Mastercard Agent Pay, BVNK |

Valuations sit remarkably close. Visa trades at a P/E of 28 with a forward multiple of 22. Mastercard carries a trailing P/E of 28 and forward 25. Both have been under pressure: Visa is down 7.7% year to date, while Mastercard has slid 13.89%.

What I’m Watching Next

I want to see whether Visa’s Data Processing line keeps printing 17% growth as AI commerce and tokenization scale, and whether the litigation provision tapers.

For Mastercard, I’ll be watching whether BVNK closes cleanly and whether Agent Pay actually drives merchant adoption rather than just headlines. Analyst price targets sit at $398.83 for Visa and $644.89 for Mastercard, implying meaningfully more upside for the smaller network.

Why I’d Split the $2,500 Toward Mastercard, With Caveats

If I had to pick one with fresh capital today, I lean Mastercard. The 22% growth in value-added services and the cleaner pivot into agentic commerce look like the more interesting growth story, and the wider YTD pullback gives a better entry.

Visa is the more defensive name for a conservative investor who wants beta of 0.77, a steady dividend, and dominant scale. Neither is cheap, and if interchange litigation or stablecoin disruption accelerates, I’d want to see another quarter before adding aggressively.

Contact [email protected] for any questions or corrections.