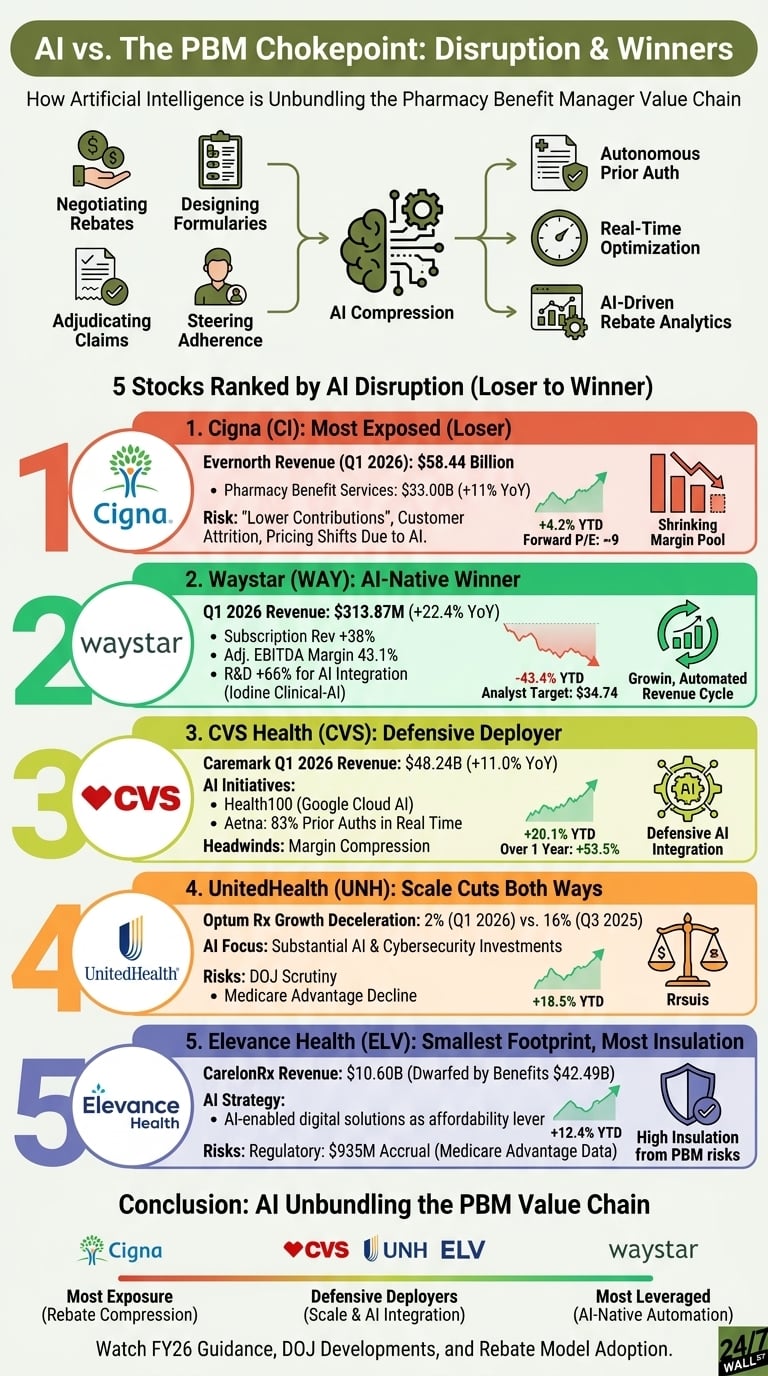

Pharmacy benefit managers (PBMs) sit at the chokepoint of U.S. drug distribution. They negotiate rebates, design formularies, adjudicate claims, and steer patient adherence. Modern artificial intelligence (AI) is designed to compress each of these high-volume, rules-driven processes. As autonomous prior authorization, real-time formulary optimization, and AI-driven rebate analytics scale, the Big Three PBMs face a structural threat to their legacy margin pools, while AI-native vendors and adjacent platforms stand to benefit. Below are five stocks ranked by the materiality of that disruption, from the most exposed (loser) to the most leveraged (winner).

1. Cigna: Most Exposed to PBM Disruption

Cigna Group (NYSE: CI | CI Price Prediction) owns Express Scripts in its Evernorth unit, now its dominant earnings engine. Evernorth generated $58.44 billion in Q1 2026 revenue, with Pharmacy Benefit Services alone at $33.00 billion (+11% YoY). Cigna Healthcare shrank 21% after the HCSC Medicare divestiture. Adjusted EPS of $7.79 beat estimates for the fourth consecutive quarter, and management raised FY26 adjusted EPS guidance to at least $30.35.

Here’s the risk: Cigna flagged “expected lower contributions from large Pharmacy Benefit Services client relationships,” pharmacy customer attrition, and “drug pricing changes or industry pricing benchmark shifts.” AI-driven transparency tools and the company’s rebate-free pharmacy benefit model are reshaping the rebate economics that historically powered Express Scripts. Shares are up just 4.2% year to date at $286.69, trading at a forward price-to-earnings (P/E) near 9, reflecting investor caution despite operational beats.

2. Waystar: The AI-Native Winner

Waystar (NASDAQ: WAY) is the clearest beneficiary of healthcare’s payment-workflow automation. Q1 2026 revenue rose 22.4% year over year to $313.87 million, with subscription revenue up 38% and adjusted EBITDA margin expanding to 43.1%. Net revenue retention reached 111%, and clients generating more than $100K LTM reached 1,433 (+15% year over year). R&D spending jumped 66% year over year to $18.4 million as the company integrates the Iodine clinical-AI acquisition and rolls out its AI-powered recoupment solution.

CEO Matt Hawkins says Waystar is “leading healthcare’s AI transformation by advancing the autonomous revenue cycle.” Yet the stock is down 43.4% year to date to $18.55, creating a gap between its fundamentals and its share price. The analyst consensus target stands at $34.74, with a forward P/E of 13.

3. CVS Health: Defensive Deployer of AI

CVS Health (NYSE: CVS) operates Caremark, which produced $48.24 billion (+11.0% year over year) in Q1 2026 Health Services revenue. Q1 adjusted EPS of $2.57 beat consensus by 16.47%, and FY26 adjusted EPS guidance was raised to $7.30 to $7.50. CVS launched Health100, a Google Cloud AI-powered subsidiary, while Aetna now processes 83% of prior authorizations in real time, eliminating over 1 million provider calls.

Management cited pharmacy reimbursement pressure and client price concessions compressing Health Services margins as headwinds. CVS is up 20.1% year to date and 53.5% over one year to $95.99. That suggests investors credit CEO David Joyner’s AI-led integration strategy.

4. UnitedHealth: Scale Cuts Both Ways

UnitedHealth Group (NYSE: UNH) houses Optum Rx, the largest PBM by volume. Q1 2026 Optum Rx revenue grew just 2% to $35.74 billion, a sharp deceleration from 16% growth in Q3 2025. Consolidated revenue rose 2.0% to $111.72 billion, with adjusted EPS of $7.23 beating by 9.38%. Medicare Advantage membership fell 965,000 in the quarter, and Justice Department scrutiny remains a structural overhang.

CEO Stephen Hemsley is funding “substantial artificial intelligence and cybersecurity investments” across prior authorization, interoperability, and pharmacy workflows. The pending Alegeus acquisition would extend Optum into consumer-directed healthcare accounts. Shares trade at $391.13, up 18.5% year to date, with FY26 adjusted EPS guidance raised to greater than $18.25.

5. Elevance Health: Smallest PBM Footprint, Most Insulation

Elevance Health (NYSE: ELV) operates CarelonRx, the smallest integrated PBM covered here. CarelonRx Q1 2026 revenue of $10.60 billion (+4.8% year over year) is dwarfed by the Health Benefits segment at $42.49 billion. Adjusted EPS of $12.58 beat by 16.78%, and FY26 adjusted EPS guidance was raised to at least $26.75.

CEO Gail Boudreaux pointed to “AI-enabled digital solutions” as a key affordability lever. The principal risk is regulatory: a $935 million accrual tied to CMS Medicare Advantage risk adjustment data, and a 15.8% year-over-year drop in Medicare Advantage membership. Shares trade at $394.07, up 12.4% year to date.

Conclusion

AI is unbundling the PBM value chain. Companies with the heaviest pharmacy-benefit revenue concentration, led by Cigna, carry the most exposure to rebate compression, transparency mandates, and client churn. Diversified incumbents like CVS, UnitedHealth, and Elevance can defend margins by deploying AI inside prior authorization, claims, and adherence workflows. However, Optum Rx’s growth deceleration signals that scale alone is no longer a moat. Waystar offers the cleanest direct exposure to the automation tailwind, though execution and leverage at 2.7x net debt remain key variables. Watch FY26 guidance revisions, Justice Department developments, and rebate-model adoption rates to determine which side of the AI ledger each company lands on.

Contact [email protected] for any questions or corrections.