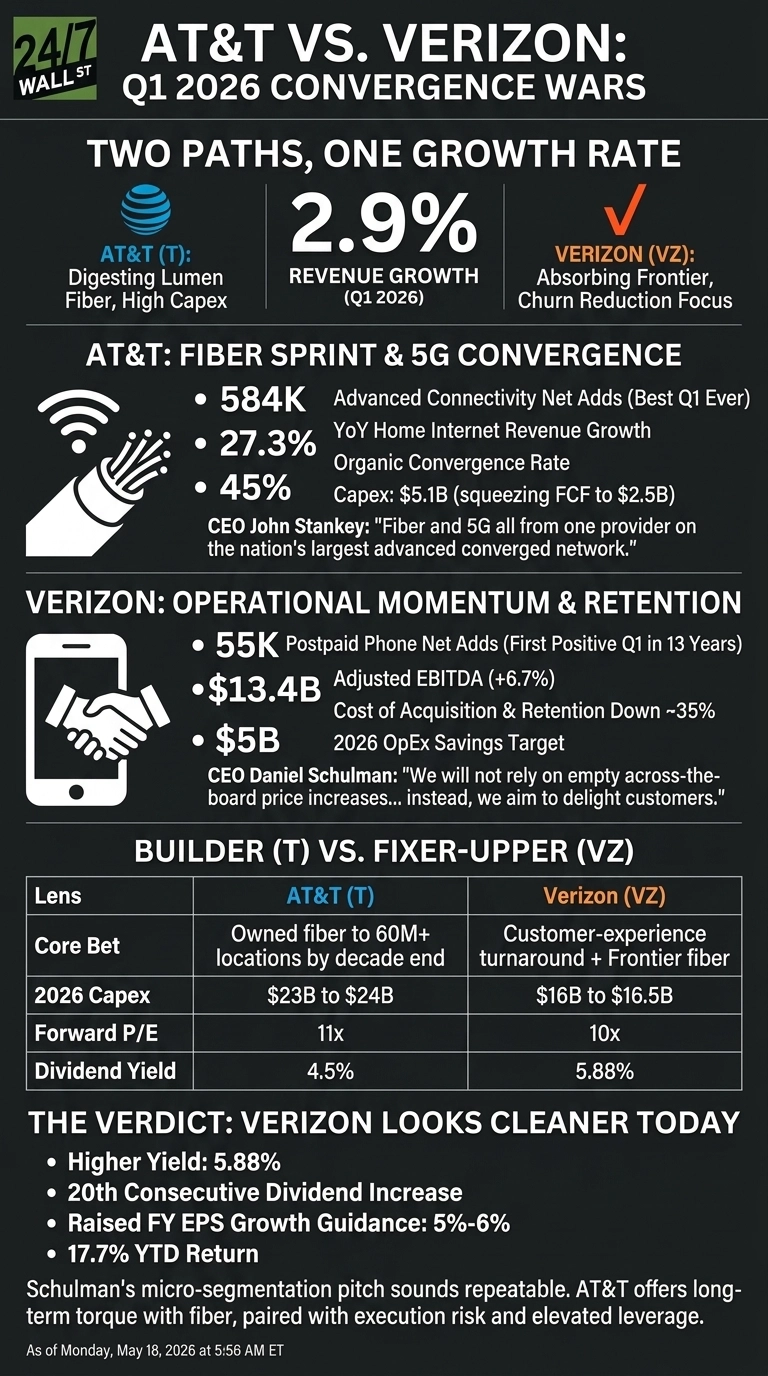

AT&T (NYSE:T | T Price Prediction) and Verizon Communications (NYSE:VZ) both posted 2.9% revenue growth in Q1 2026, yet the businesses behind those identical top lines look very different.

AT&T is digesting the Lumen fiber acquisition that closed in early February 2026, while Verizon is now run by Daniel Schulman and absorbing Frontier, which closed January 20, 2026. Two convergence stories, two very different execution styles.

Fiber Sprints for AT&T, Phones Finally Click for Verizon

AT&T leaned hard on broadband. The quarter brought 584,000 advanced connectivity net adds, the company’s best Q1 ever, with advanced home internet revenue up 27.3% year over year. Adjusted EPS landed at $0.57, up nearly 12%, on revenue of $31.51B.

CEO John Stankey framed the strategy plainly: “fiber and 5G all from one provider on the nation’s largest advanced converged network.” The catch is capex. AT&T spent $5.1 billion in the quarter, squeezing free cash flow to $2.5 billion.

Verizon’s headline was retention. Postpaid phone net adds came in at 55,000, the first positive Q1 in 13 years, and adjusted EBITDA hit $13.4 billion, up 6.7%. Adjusted EPS of $1.28 beat the $1.21 consensus by 5.8%.

Schulman is unapologetic about the new tone: “We will not rely on empty across-the-board price increases that create short-term financial gains that erode the long-term trust of our customers.” Management raised full-year EPS growth guidance to 5% to 6%.

Builder vs. Fixer-Upper

| Lens | AT&T | Verizon |

| Core Bet | Owned fiber to 60M+ locations by decade end | Customer-experience turnaround plus Frontier fiber |

| 2026 CapEx | $23B to $24B | $16B to $16.5B |

| Forward P/E | 11x | 10x |

| Dividend Yield | 4.5% | 5.88% |

Stankey is pouring capital into the ground. Verizon is pouring it into churn reduction. Schulman cited cost of acquisition and retention down roughly 35% since December, with consumer postpaid churn at 0.90% and trending lower.

AT&T’s organic convergence rate of 45% is the more structural metric, but the EchoStar spectrum deal will push net debt to EBITDA to roughly 3.2x before settling.

The Next Test Is Cash Flow

I will be watching whether AT&T can hold its $18B+ free cash flow guide while funding fiber and integrating Lumen. The Q1 FCF dip is explainable, but investors are clearly nervous. The stock fell 4.5% last week, with Stankey’s May 19 J.P. Morgan conference appearance looming as a credibility checkpoint.

For Verizon, the watchpoint is whether the $5 billion 2026 OpEx savings target actually flows through, and whether the Frontier integration produces the promised $1 billion+ run-rate synergies by 2028.

Where Verizon’s Story Looks Cleaner Right Now

Between these two, Verizon’s setup looks cleaner today. The 5.88% yield, 20th consecutive dividend increase, raised EPS guide, and 17.7% YTD return tell a coherent story of operational momentum at a cheap multiple. Schulman’s micro-segmentation pitch sounds repeatable in a way that promotional carpet-bombing never was.

AT&T may offer more long-term torque if the fiber math works out, and the 8x trailing P/E bakes in real skepticism. AT&T offers more long-term torque if the fiber math works out, paired with execution risk and elevated leverage. Verizon’s quarter, by contrast, was operationally cleaner with fewer surprises.

Contact [email protected] for any questions or corrections.