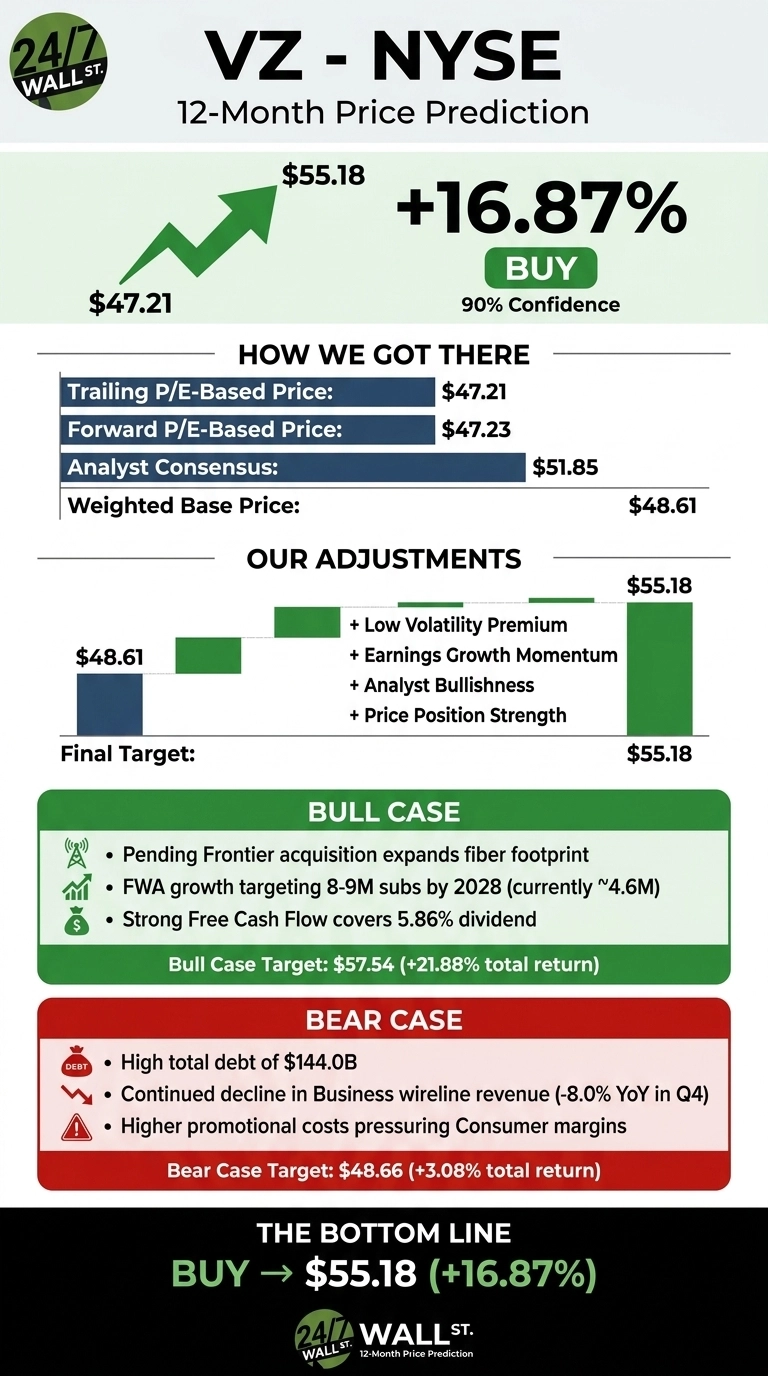

Our Verizon (NYSE:VZ | VZ Price Prediction) call is straightforward: the stock is undervalued, the dividend is well covered, and the model points to meaningful upside over the next 12 months. With shares trading at $47.21 as of May 13, 2026, our 24/7 Wall St. price target for Verizon is $55.18, implying 16.87% upside. Our recommendation is buy with a 90% confidence level, which we consider high.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $47.21 |

| 24/7 Wall St. Price Target | $55.18 |

| Upside | 16.87% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Quiet Rerating Has Already Begun

Verizon has been one of the better-performing defensive names in 2026. Shares are up 19.73% year to date and 18.19% over the past year, with the stock recovering sharply from a $39.36 low in January 2026 to within striking distance of the $50.91 52-week high.

The most recent earnings report (Q4 2024) showed revenue of $35.68 billion, beating expectations, alongside EPS of $1.10 in line with estimates. The standout was operations: 568,000 postpaid phone net adds, the best in over a decade, and FWA revenue of $611 million, up 51.6% YoY.

The Case for $57+

Bulls focus on three catalysts. First, the pending Frontier Communications acquisition meaningfully expands Verizon’s fiber footprint and gives it a credible converged offering against cable.

Second, FWA is on a tear, with management targeting 8 to 9 million subscribers by 2028 versus roughly 4.6 million today.

Third, free cash flow of $19.82 billion in 2024 comfortably covers the 5.86% dividend yield. Our bull case scenario points to $57.54, a 21.88% total return. Insider confidence supports the read: senior executives including CEO Hans Vestberg and CFO Anthony Skiadas have been steady buyers through March and April 2026.

The Risks Worth Watching

The bear case centers on the $144 billion debt load and continued declines in legacy business wireline, which fell 8% YoY in Q4. Higher promotional spend is also pressuring consumer margins. Our bear case scenario points to $48.66, still a positive 3.08% total return when factoring the dividend. It should be noted that the high debt reflects multi-year C-Band buildout that is now monetizing through FWA, and capex already fell from $18.77 billion in 2023 to $17.09 billion in 2024.

Verizon Price Prediction 2026-2030

The 24/7 Wall St. price target stands at $55.18 with a buy rating and 90% confidence. The tipping factor is valuation: at a forward P/E near 10, you are getting a defensive cash flow machine for less than the market multiple. The setup favors investors seeking yield plus modest capital appreciation. Key risks to monitor include a sharp spike in rates or a collapse of the Frontier deal.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $55.18 |

| 2027 | $62.08 |

| 2028 | $67.47 |

| 2029 | $72.47 |

| 2030 | $77.49 |

These projections assume Verizon executes on FWA, closes Frontier, and holds dividend coverage. Significant upside or downside could come from interest rate moves or a competitive break in wireless pricing.

Contact [email protected] for any questions or corrections.