Verizon (NYSE: VZ | VZ Price Prediction) and AT&T (NYSE: T) just reported Q3 results revealing two telecom giants chasing different growth paths. Verizon leaned on wireless pricing discipline and a new CEO’s customer-first mandate. AT&T bet on fiber broadband convergence and a massive spectrum purchase to fuel its 5G future.

Wireless Carries Verizon. Fiber Lifts AT&T.

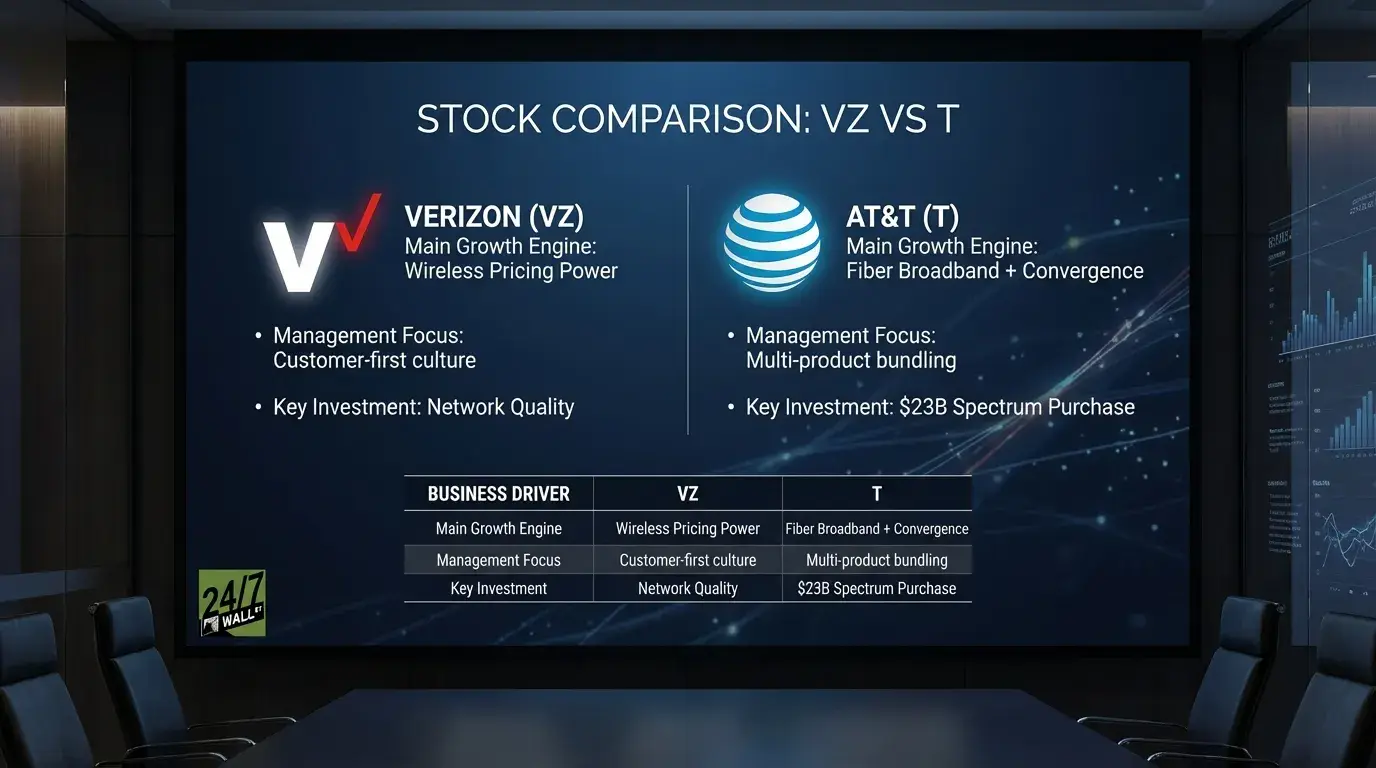

Verizon posted $33.82B in revenue, missing estimates of $35.31B but growing 1.5% year-over-year. Wireless service revenue climbed 2.1% to $21.0B, driven by pricing power. Equipment revenue jumped 5.2% to $5.6B as device upgrade cycles accelerated. Net income surged to $5.06B from $3.41B a year earlier. New CEO Dan Schulman emphasized a culture shift toward customer retention, signaling Verizon will prioritize quality over aggressive acquisition.

AT&T delivered $30.70B in revenue, slightly below the $30.89B estimate, with 1.6% growth. Mobility service revenue rose 2.3% to $16.9B, but fiber broadband surged 16.8% to $2.2B. CEO John Stankey highlighted convergence success: 41% of fiber households now bundle AT&T Mobility service, underscoring the strategy to lock customers into multi-product ecosystems. Net income hit $9.7B, though $9.3B came from the DIRECTV sale. Free cash flow reached $4.9B, and AT&T repurchased $1.5B in shares while announcing a $23B spectrum acquisition from EchoStar to bolster 5G capacity.

| Business Driver | Verizon | AT&T |

| Main Growth Engine | Wireless pricing power | Fiber broadband + convergence |

| Management Focus | Customer-first culture | Multi-product bundling |

| Key Investment | Network quality | $23B spectrum purchase |

One Defends Premium Wireless. One Bets on Convergence.

Verizon’s strategy centers on protecting its premium network positioning. The company raised its dividend for the 19th consecutive year, reinforcing its appeal to income investors with a 6.77% yield. Guidance projects wireless service revenue growth of 2.0% to 2.8% and adjusted EBITDA growth of 2.5% to 3.5%, with free cash flow expected between $19.5B and $20.5B. Operating margins stand at 23.9%, the highest among peers, but profit margins lag AT&T at 14.4% versus 17.9%. High debt limits flexibility for aggressive expansion.

AT&T is pursuing a convergence play tying fiber internet to mobile service. Fiber revenue growth of 16.8% outpaces the broader industry, and the 41% convergence rate suggests the strategy is working. Guidance calls for mobility service revenue growth above 3% and fiber revenue growth in the mid-to-high-teens range, both ahead of Verizon’s projections. The $23B spectrum deal positions AT&T to compete more aggressively in 5G, though it adds near-term financial pressure. Business Wireline continues to decline due to legacy product erosion.

T-Mobile and Comcast Add Context

T-Mobile (NASDAQ: TMUS) posted $21.96B in revenue, up 8.9%, and added 2.3M postpaid customers, its best Q3 in a decade. Service revenue grew 9%, and the company raised guidance for postpaid adds to 7.2M to 7.4M. T-Mobile’s aggressive customer growth pressures both Verizon and AT&T to justify premium pricing. Comcast (NASDAQ: CMCSA) reported $31.20B in revenue, down 2.7%, highlighting the threat AT&T’s fiber push poses to cable broadband incumbents.

I’m Watching Fiber Momentum and Spectrum Execution

AT&T offers upside tied to fiber and convergence. The 16.8% fiber growth rate and rising bundle penetration suggest a durable competitive advantage Verizon lacks. AT&T’s PEG ratio of 1.00 versus Verizon’s 1.97 signals better growth potential relative to valuation. However, the $23B spectrum commitment introduces execution risk, and Business Wireline remains a headwind.

Verizon fits income-focused investors better. The 6.77% yield and 19-year dividend streak provide stability, and the company’s premium network reputation supports pricing power. But if fiber convergence proves as sticky as AT&T’s numbers suggest, Verizon may struggle to justify its premium without a comparable growth engine.

Contact [email protected] for any questions or corrections.