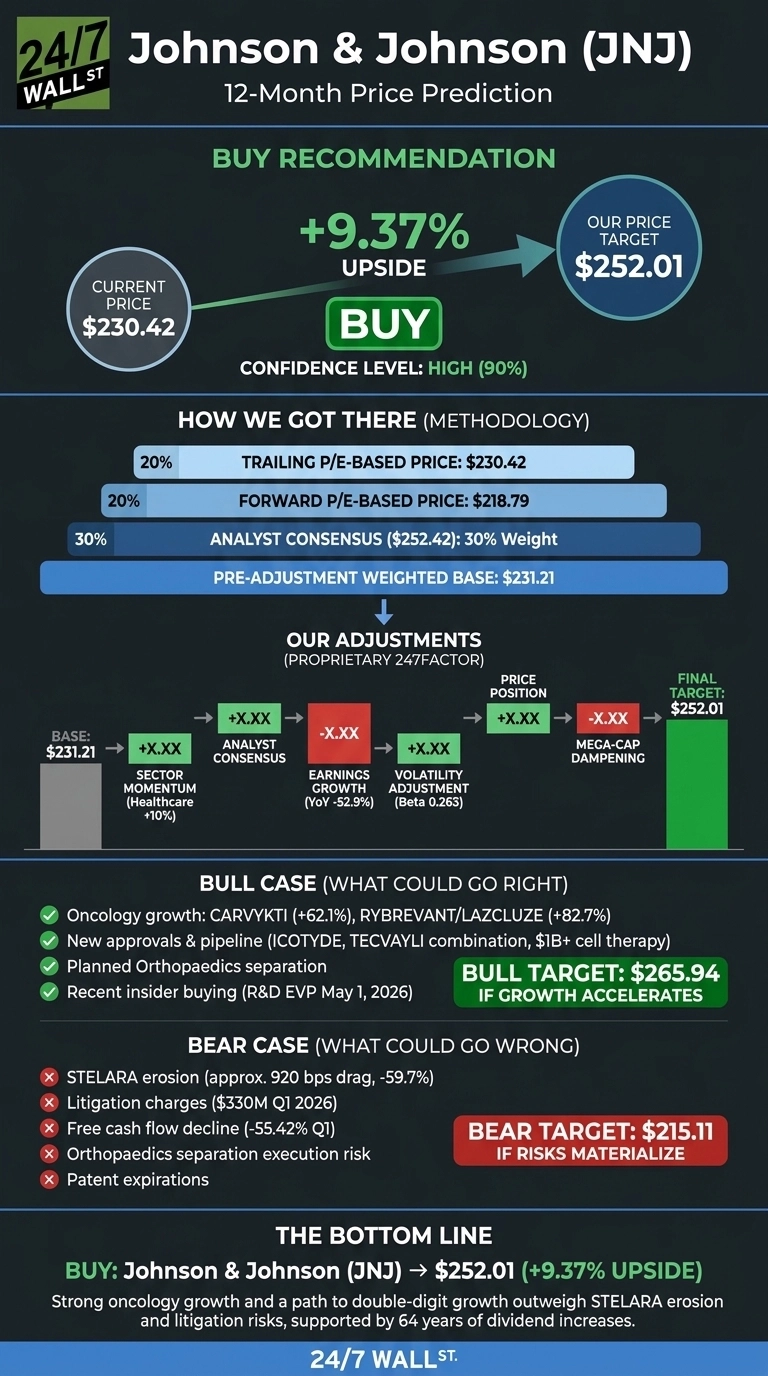

Johnson & Johnson (NYSE:JNJ | JNJ Price Prediction) closed the most recent session at $230.42, up 2.58% on the week as buyers rotated back into defensive healthcare names. Our 24/7 Wall St. price target for Johnson & Johnson is $252.01 over the next 12 months, implying 9.37% upside. The recommendation is buy, and our confidence level is 90%, the high end of our scale.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $230.42 |

| 24/7 Wall St. Price Target | $252.01 |

| Upside | 9.37% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Defensive Compounder Riding Oncology Strength

JNJ has been one of the strongest performers in large-cap pharma over the past year, rising 59.53% over twelve months and 11.93% year to date. The stock pulled back 3.17% over the past month after the Q1 earnings report, but the 14-day RSI has rebounded from oversold territory to 51.98, signaling renewed buying interest.

Q1 2026 was a clean beat. Revenue of $24.06 billion grew 9.9% year over year, and adjusted EPS of $2.70 extended the consensus beat streak to four consecutive quarters. Innovative Medicine grew 11.2% with DARZALEX at $3.96 billion and TREMFYA up 68.3%, more than absorbing a 59.7% STELARA decline from biosimilar competition. Management raised full-year revenue guidance to $100.3B to $101.3B and adjusted EPS to $11.45 to $11.65.

The Case for $266+

The bull scenario takes JNJ to $265.94, a 15.41% return. The driver is oncology. CARVYKTI grew 62.1% to $597 million, RYBREVANT/LAZCLUZE jumped 82.7%, and the new TECVAYLI plus DARZALEX FASPRO combination opens a second-line myeloma indication.

Add the ICOTYDE psoriasis launch, VARIPULSE Pro in Europe, and a $1 billion Pennsylvania cell therapy facility, and management’s framing of a path to double-digit growth by decade-end looks credible. Insider buying reinforces this: R&D chief John Reed acquired 25,255 shares on May 1, 2026. The planned Orthopaedics business separation could unlock a sum-of-the-parts rerating north of $270.

The Risks Worth Watching

The bear scenario lands at $215.11, a 6.64% drawdown. STELARA biosimilar erosion produced a 920 bps drag on Innovative Medicine, and IMBRUVICA, XARELTO, and REMICADE all declined. Free cash flow fell 55.42% in Q1, and net income dropped 52.4%.

Bulls would counter that those declines are largely tied to a one-time $330 million litigation charge and timing of working capital, with gross profit still up 9.77%. Talc litigation overhang, MedTech Surgery restructuring, and execution risk on the Orthopaedics spin remain real. One analyst still rates the stock Strong Sell.

I’d Buy It Here

The 24/7 Wall St. price target is $252.01, the recommendation is buy, and confidence sits at 90%. The factor that tips the scale is the combination of a 2.32% dividend yield backed by 64 consecutive years of increases, low beta, and an oncology pipeline that is finally offsetting STELARA losses.

I’d be a buyer here if JNJ holds the $235.39 50-day moving average and Q2 confirms the guidance raise. I’d stay sidelined if STELARA erosion accelerates beyond modeled levels or if the December 8, 2026 Enterprise Business Review reveals incremental restructuring charges.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $242.02 |

| 2027 | $252.01 |

| 2028 | $275.00 |

| 2029 | $299.00 |

| 2030 | $323.27 |

These projections assume Johnson & Johnson continues executing on guidance and completes the Orthopaedics separation without disruption. Significant upside could come from accelerating CARVYKTI and TREMFYA adoption, while downside risk centers on talc-related liabilities and faster-than-expected biosimilar erosion across the legacy portfolio.

Contact [email protected] for any questions or corrections.