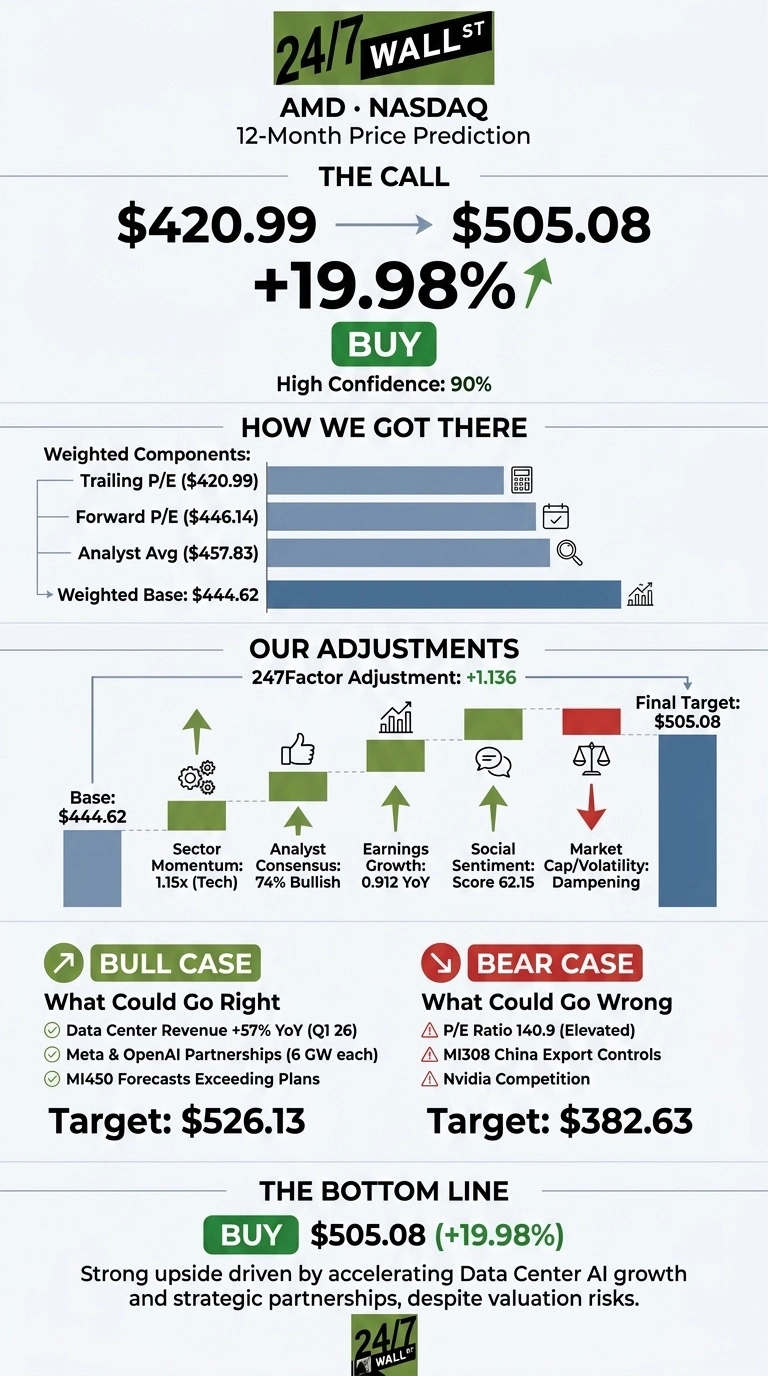

The question on every Advanced Micro Devices (NASDAQ:AMD | AMD Price Prediction) shareholder’s mind is whether the stock can stretch from the low $400s to $500 before year-end. After running the numbers through our proprietary model, the answer is a qualified yes.

Our 24/7 Wall St. price target for AMD is $505.08 over the next 12 months, implying 19.98% upside from the current $420.99 quote. Our recommendation is buy with high confidence at 90%.

| Metric | Value |

|---|---|

| Current Price | $420.99 |

| 24/7 Wall St. Price Target | $505.08 |

| Upside | 19.98% |

| Recommendation | BUY |

| Confidence | 90% |

A Year That Rewrote AMD’s Story

AMD has been one of 2026’s defining trades. Shares are up 96.58% year to date and 259.3% over the trailing 12 months, with a one-month surge of 51.22% that took the stock to a 52-week high of $469.22. An 8.24% pullback last week provides the entry point we are using today.

Q1 2026, reported May 5, was the catalyst. Revenue hit $10.253 billion (+37.85% YoY), non-GAAP EPS came in at $1.37 beating expectations, and Data Center revenue exploded 57% to $5.775 billion. Q2 guidance of $11.2 billion implies 46% YoY growth.

The Case for $525+

The bull case rests on AI infrastructure scaling faster than the model assumes. Lisa Su told investors on the Q1 call that AMD now sees the server CPU TAM growing at “greater than 35% annually, reaching over $120 billion by 2030.”

She added that customer forecasts for MI450 and Helios are “exceeding our initial expectations”, supporting “tens of billions of dollars in annual Data Center AI revenue in 2027.”

Signed commitments include OpenAI (6 GW), Meta (up to 6 GW with custom MI450), Oracle’s Helios supercluster, and a Samsung HBM4 collaboration for the MI455X. Su’s longer-term EPS target exceeds $20. Our bull case scenario lands at $526.13 with a within-period peak near $526.49. With 37 buys and zero sell ratings, Wall Street is firmly bullish.

What Could Drag AMD Back to $380

The bear case begins with valuation. AMD trades at a trailing P/E of 141 and an EV/EBITDA of 91, leaving little margin for error. Reddit sentiment has cooled from a bullish peak of 85 on May 15 to 36 today, with our composite sentiment index at a neutral 47.26.

Risks include U.S. export controls on MI308 to China (which caused a $800 million Q2 2025 charge), TSMC dependence, and competitive pressure from NVIDIA. Free cash flow tripled to $2.56 billion in Q1, and forward P/E sits at 65. Our bear scenario bottoms at $376.31 before recovering to $382.63.

Why the Setup Looks Compelling Here

The 24/7 Wall St. price target of $505.08 is a buy rating at 90% confidence. Data Center acceleration from 14% YoY in Q2 2025 to 57% in Q1 2026, paired with multi-gigawatt customer commitments, tips the scale.

Attractive entry zones would be on a pullback toward the 50-day moving average of $279.21 or near $400. The thesis weakens if Q2 2026 results miss the $11.2 billion revenue guide or if MI450 shipments slip into 2027.

Our model projects the following trajectory, assuming AMD executes on its AI roadmap and the server CPU TAM expands as guided.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $505 |

| 2027 | $575 |

| 2028 | $635 |

| 2029 | $685 |

| 2030 | $735 |

These projections assume AMD delivers on Lisa Su’s pathway to $20+ in EPS. Downside could result from sustained China export restrictions, NVIDIA maintaining accelerator dominance, or memory cost inflation pressuring margins.

Contact [email protected] for any questions or corrections.