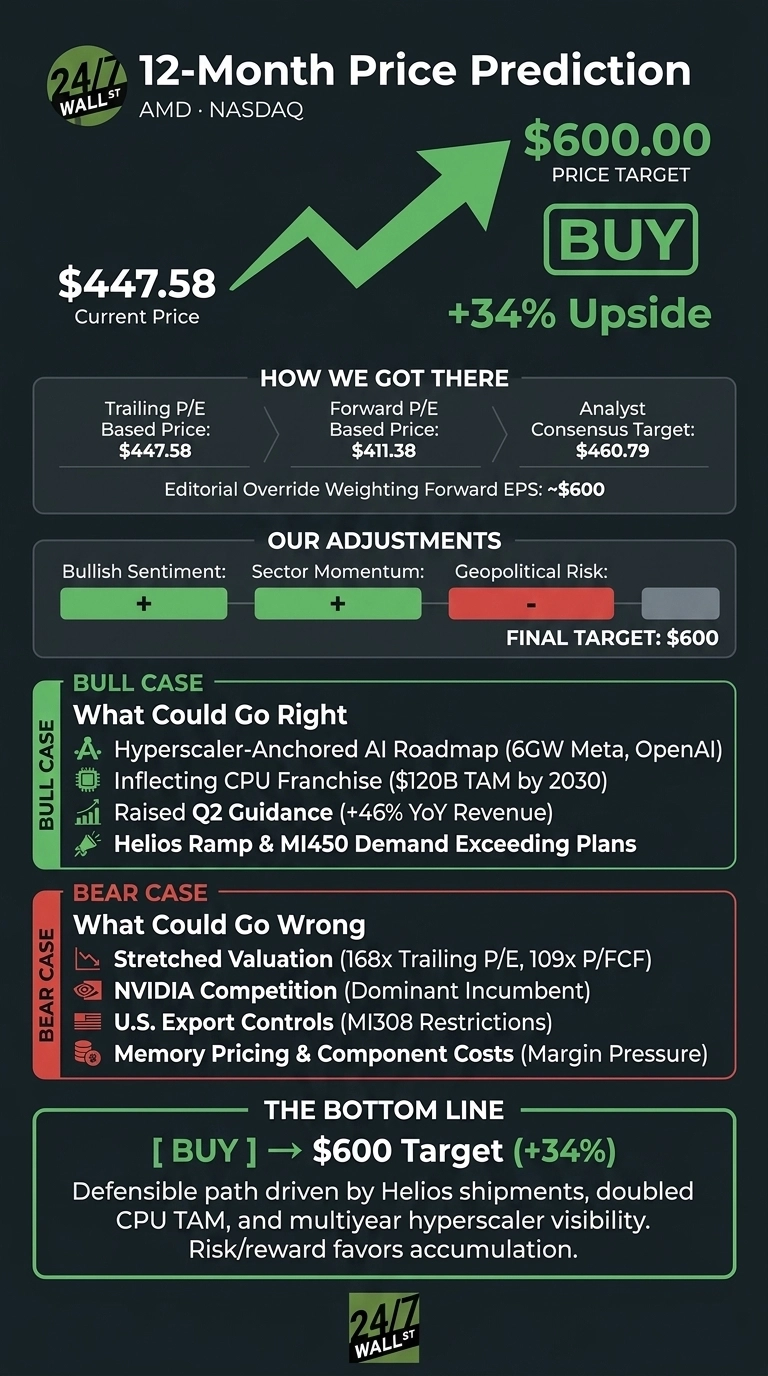

AMD (NASDAQ: AMD | AMD Price Prediction) has a 24/7 Wall St. price target of $600 over the next 12 months, with the stock currently trading at $447.58. That implies roughly roughly 34% upside, and we are rating the shares buy with high confidence.

AMD now combines a hyperscaler-anchored AI roadmap, an inflecting CPU franchise, and guidance that just raised the bar. The bull case now rests on signed hyperscaler commitments and raised guidance.

| Metric | Value |

|---|---|

| Current Price | $447.58 |

| 24/7 Wall St. Price Target | $600 |

| Upside | ~34% |

| Recommendation | BUY |

| Confidence Level | High |

From $343 to $448: AMD’s Post-Earnings Reset

AMD shares are up 62.79% in the past month and 108.99% year to date, with the most recent session adding 8.1%. Q1 drove the move: $10.25 billion in revenue (+37.85% YoY), EPS of $1.37 beating the $1.29 consensus, Data Center revenue of $5.78 billion (+57% YoY), and free cash flow of $2.57 billion, up 252.96%. Q2 guidance of approximately $11.2 billion, or 46% YoY growth, sealed the rerating.

The Case for $600+

The bull case anchors to Lisa Su’s revised server CPU TAM. On the Q1 call she said AMD expects the server CPU TAM to grow at “greater than 35% annually, reaching over $120 billion by 2030”, roughly double the prior outlook.

Meta’s commitment to deploy up to 6 gigawatts of AMD Instinct GPUs, the OpenAI 6 GW partnership, and Oracle’s 27,000-node MI355X cluster provide multiyear visibility. Su stated customer MI450 forecasts are now “above our initial plans that we had planned for 2027.”

Of 50 covering analysts, 37 rate AMD a Buy with zero Sells. If Helios ramps cleanly in H2 and Venice EPYC takes share, analyst consensus of $460.79 moves higher quickly, and $600 becomes the new midpoint.

The Risks Worth Watching

AMD trades at a 168 trailing P/E and 109 times free cash flow. Composite sentiment fell 30.85 points in seven days, and our internal AI model pegs fair value at $401.37. NVIDIA remains the dominant accelerator incumbent, U.S. export controls on the MI308 cost AMD roughly $440 million net in FY25, and memory pricing is tight enough that gaming and client could decline in H2. A bear scenario lands closer to the model’s $373.74 downside.

The elevated multiple reflects a business that grew operating cash flow 214.7% YoY. On a forward basis the multiple compresses meaningfully as the MI450 ramp lands.

AMD Price Prediction 2026-2030

The 24/7 Wall St. price target of $600 reflects a defensible path driven by Helios shipments, a doubled CPU TAM, and hyperscaler contracts already on paper. The risk/reward favors accumulation for investors who can stomach a 2.4 beta and post-earnings volatility.

More conservative positioning may wait for MI450 to be revenue-positive before committing, as that proof point lands in Q3 and Q4. Lisa Su’s “clear path to exceed” $20 in long-term EPS tips the scale. Buy.

Here is where our model projects AMD could trade if the AI infrastructure cycle plays out as Lisa Su has guided.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $600 |

| 2027 | $685 |

| 2028 | $760 |

| 2029 | $830 |

| 2030 | $900 |

These projections assume AMD executes the Helios ramp, captures meaningful share of the $120 billion 2030 server CPU TAM, and delivers Su’s “tens of billions of dollars in annual Data Center AI revenue in 2027.”. Significant downside could come from intensified export controls, an NVIDIA roadmap leap, or a broader semiconductor cyclical reset.

Contact [email protected] for any questions or corrections.