Cisco Systems (NASDAQ: CSCO | CSCO Price Prediction) and CrowdStrike (NASDAQ: CRWD) delivered very different earnings stories. Cisco posted $15.84 billion in Q3 FY26 revenue, while CrowdStrike closed FY26 with $5.25 billion in ending annual recurring revenue (ARR). Both stocks have risen sharply, raising a harder question: which carries the weaker risk/reward from here?

The Cisco Bear Case: Cost Cuts Dressed Up as Growth

Cisco looks healthy on the surface. Networking revenue jumped 25% year over year, and operating income climbed 23.67%. Look closer, and the picture gets messier. Security was flat, Collaboration slipped 1%, and Services fell 1%. Only one engine is firing.

Gross margins are quietly bleeding. Q4 FY26 gross margin guidance is 65.5% to 66.5%, compressed from 68.4% a few quarters back, as AI hardware mix dilutes profitability. Operating cash flow fell 7.39% year over year while capital spending spiked 58.62%. Management announced restructuring charges up to $1 billion, a familiar Cisco playbook of pruning costs to flatter EPS.

Cisco is chasing silicon, optics, security, AI infrastructure, and post-quantum networking simultaneously. Insiders took note. On May 10, 2026, seven senior executives, including CEO Chuck Robbins, sold shares at $96.57. The stock is now up 49.8% year to date.

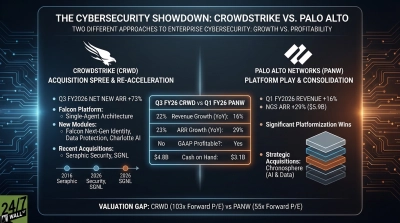

The CrowdStrike Bear Case: Premium Price, Premium Risk

CrowdStrike’s fundamentals are arguably the cleanest in software. Net new ARR hit a record $330.7 million in Q4, up 47% year over year. Falcon Flex ARR grew 120%+. Free cash flow margin reached 29%. Growth is accelerating.

The problem is the price tag. Shares trade at a price-to-sales of 32.73 and a forward P/E near 109x. GAAP operations still lose money, with an FY26 operating loss of $293.3 million, widened by stock-based compensation. Falcon sensor incident costs continued at $117.7 million for the year.

Insider behavior is concerning. CEO George Kurtz executed 100+ separate transactions between April 20 and May 14, 2026, selling a total of 14,197 shares at prices from $418 to $583. President Michael Sentonas dumped 55,000 shares across three days. Director Sameer Gandhi cleared 10,000 shares in a single session. No insider bought a single share.

| Lens | Cisco | CrowdStrike |

| Forward P/E | 21x | 109x |

| YTD Performance | +49.8% | +31.6% |

| Core Bear Trigger | Margin compression | Insider exodus |

Why CrowdStrike Is the Better Short Right Now

CrowdStrike is the cleaner setup. Cisco’s bear case is valid, but the stock pays a 1.5% dividend, trades at a reasonable forward multiple, and has a $9.6 billion buyback cushion. Shorting steady cash flow at 21x forward earnings is expensive carry.

CrowdStrike has an aggressive insider selling cluster at all-time highs, a price-to-sales above 32, persistent GAAP losses, and a stock that ran 45.5% in one month. Fundamentals are excellent, but expectations have detached from them. If Q1 net new ARR disappoints, the air pocket below $600 could be steep. That is where the asymmetric downside risk lies.

Contact [email protected] for any questions or corrections.