Few legacy tech names have staged a comeback like Cisco Systems (NASDAQ:CSCO | CSCO Price Prediction). After spending more than two decades in the wilderness post dotcom, the networking giant is suddenly an AI infrastructure story, and the stock has responded with a vertical move that has even long-time holders asking how much further this can go.

The 24/7 Wall St. Price Target for Cisco

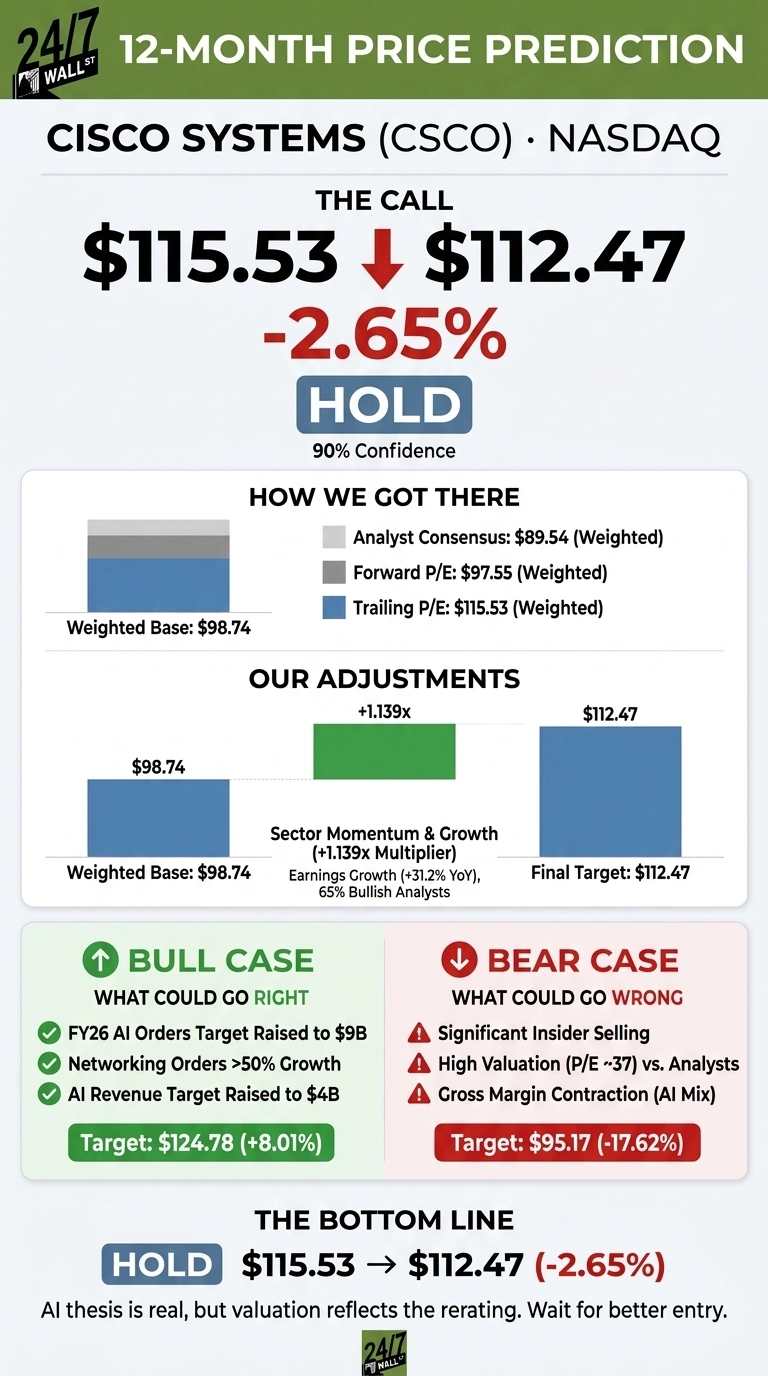

Cisco trades at $115.53 after a 25.36% one-week surge tied to the Q3 FY26 print. Our 24/7 Wall St. price target for Cisco is $112.47 over the next 12 months, implying -2.65% downside. The recommendation is hold with a 90% confidence level. In plain language: the AI thesis is real, but the rerating has happened.

| Metric | Value |

|---|---|

| Current Price | $115.53 |

| 24/7 Wall St. Price Target | $112.47 |

| Upside/Downside | -2.65% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Our 24/7 Wall St. price target sits just below where Cisco trades today. The bull argument is straightforward: AI infrastructure orders just got raised to $9 billion for FY26, and the campus refresh cycle is in early innings. If either catalyst overshoots, our model will look conservative.

A Run That Started With Earnings

Cisco is up 51.59% YTD, 39.85% over the past month, and 92.8% over the past year, with shares 25% below a 52-week high of $119.36. Q3 FY26 delivered record revenue of $15.841 billion (+11.96% YoY) and non-GAAP EPS of $1.06, the fourth consecutive beat.

Networking revenue grew 25%, and total product orders surged 35% YoY. CEO Chuck Robbins said “Cisco is well-positioned as the critical infrastructure for the AI era.”

HSBC upgraded Cisco to Buy from Hold with a price target of $137, up from $77. The firm cites stronger AI infrastructure momentum and better earnings visibility for its raised target and rating.

The Case for $125 and Higher

Bulls have plenty to point to. AI infrastructure orders hit $5.3 billion YTD, with FY26 guidance raised to $9 billion from $5 billion, and AI revenue to $4 billion. Data center switching orders jumped 40% and the multi-year campus refresh is ramping faster than prior cycles.

The AT&T post-quantum cryptography SD-WAN partnership and Splunk integration broaden the security and observability story. The bull scenario lands at $124.78, an 8.01% gain, if order momentum holds and forward P/E expands toward 28x.

What Could Go Wrong

The sober view starts with valuation. The trailing P/E is 37, and analyst mean target sits at $89.54, well below today’s print. Insider activity in February through April skewed heavily toward selling, including the CFO and several EVPs at prices between $76.21 and $83.17.

Operating cash flow fell 7.39% YoY, services revenue dipped 1%, and gross margins are compressing as AI hardware mix grows. Bulls counter that margin pressure reflects deliberate volume growth in AI silicon, and the up to $1 billion restructuring charge funds next-gen silicon, optics, and security. The bear case lands at $95.17, a 17.62% drawdown.

Cisco Price Prediction 2026-2030

The 24/7 Wall St. price target is $112.47, a hold with 90% confidence. The key swing factor is whether AI orders sustain a $9 billion annual run rate or accelerate beyond it. The bullish setup strengthens if Q4 FY26 shows hyperscaler orders above $3 billion and gross margin stabilizing in the 65.5% to 66.5% range. The thesis weakens if order growth decelerates or insider selling continues at higher prices.

Looking further out, here is where our model projects Cisco could trade, assuming current AI order momentum and margin trajectory hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $112.47 |

| 2027 | $116.50 |

| 2028 | $119.75 |

| 2029 | $122.00 |

| 2030 | $124.12 |

These projections assume Cisco continues executing on AI infrastructure and the campus refresh. Significant upside could come from sustained hyperscaler share gains, while downside risk centers on tariff-driven margin compression and hyperscaler concentration.

Contact [email protected] for any questions or corrections.