A 67-year-old retiree comparing core bond funds usually meets two pitches: PIMCO’s actively managed lineup, or the Vanguard Total Bond Market ETF (NASDAQ:BND). BND sounds boring next to a star manager promising credit selection and tactical duration calls, yet it owns roughly 11,000 individual bonds across the investment-grade U.S. market for 0.03% a year. On a $300,000 sleeve, that is about $90 in annual fees versus $1,650 for PIMCO’s flagship active ETF. The question is whether BND has actually earned that cost edge or simply collected it.

What BND Is Built To Do

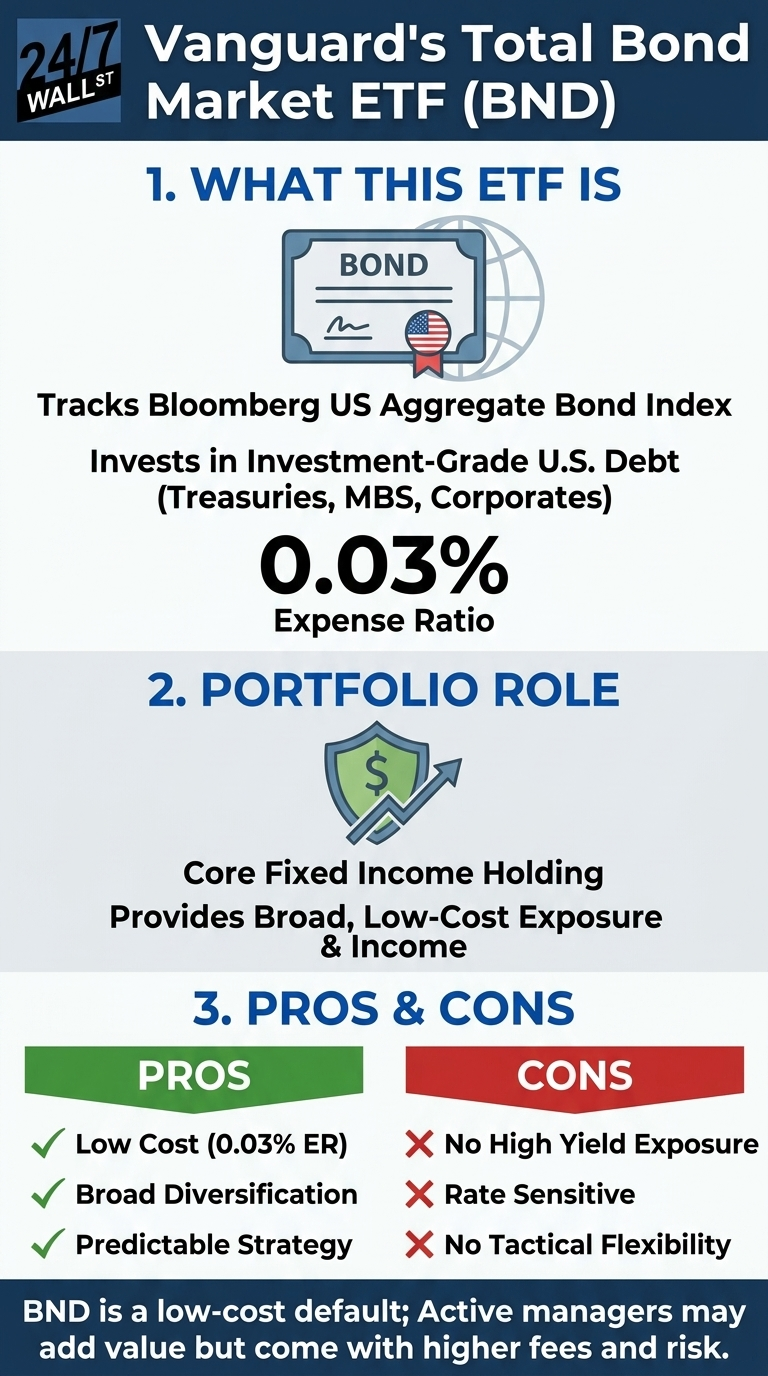

BND tracks the Bloomberg US Aggregate Bond Index, the standard benchmark for U.S. taxable investment-grade debt. The portfolio weights holdings by outstanding issuance, which tilts heavily toward U.S. Treasuries, agency mortgage-backed securities, and investment-grade corporates. The return engine is straightforward: the fund collects coupon income from the underlying bonds, passes it through to shareholders as monthly distributions, and lets the index handle rebalancing.

The big takeaways are that there is no manager picking credits, timing duration, or reaching into high yield. With around $130 billion in assets and a current distribution yield near 4.0%, the fund functions as the bond market in a single ticker.

Testing The Pitch Against PIMCO

The case for active bond management is that skilled managers can outperform a passive index after fees, and, unfortunately, the data does not cleanly favor BND here. The PIMCO Active Bond ETF (NYSEARCA:BOND) returned about 5% over the past year and roughly 1% over five years on a total return basis. BND returned about 4% and was slightly negative over the same windows. PIMCO Multisector Bond ETF (NYSEARCA:PYLD), which can stretch into non-investment-grade credit, gained about 6% over the past year.

So the headline reverses on these two PIMCO products. What BND does win on is consistency and predictability relative to the broader active bond fund universe, where most managers fail to beat the Aggregate net of fees over rolling-decade windows. The honest read: BND is the right default, but PIMCO’s better active mandates have added value here for investors willing to pay for it.

The Rate Backdrop Matters

The 10-year Treasury yield sits at 4.589%, hitting a fresh 12-month high after climbing roughly a third of a percentage point over the past month. This upward move in rates explains the soft five-year price performance of BND, because existing fixed-income assets naturally repriced lower as new bonds with higher coupons entered the market. The clear upside to this shift is that today’s yield environment finally rewards bondholders with meaningful income, and the reset is directly reflected in BND’s current distribution yield.

Where BND Falls Short

- No high yield or non-U.S. exposure. The Aggregate is investment grade and dollar-denominated. Investors seeking a broader reach typically pair BND with the Vanguard Total International Bond ETF (NASDAQ: BNDX) for international bonds, or with a separate credit sleeve.

- Rate sensitivity. With an intermediate duration profile, BND moves inversely to rates. The past five years have shown what that looks like in a tightening cycle.

- No tactical flexibility. When credit spreads blow out, or specific sectors offer outsized yield, BND cannot lean in. PIMCO’s mandates can.

Who This Fund Fits

The bottom line is that BND can and often does serves as the core fixed-income holding for retirees and accumulators seeking broad investment-grade exposure at the lowest available cost. The iShares Core U.S. Aggregate Bond ETF (NYSEARCA:AGG) is essentially identical at the same 0.03% expense ratio, so the choice between them is a coin flip. Investors who want a manager actively hunting yield and who accept the higher fee and tracking risk that come with it have a legitimate case for adding a sleeve of BOND or PYLD alongside. The mistake is paying active fees expecting passive reliability, or owning passive expecting active alpha.

Contact [email protected] for any questions or corrections.