Eli Lilly (NYSE:LLY | LLY Price Prediction) is growing like a software company. Q1 2026 revenue hit $19.80B, up 55.5% year over year, with Mounjaro at $8.66B (+125%) and Zepbound at $4.16B (+80%).

CEO David Ricks told investors “2026 is off to a strong start, we delivered 56% revenue growth in the first quarter and raised our full-year revenue guidance by $2 billion.” Yet shares trade at $1,021.41, down on the year. Can Lilly hit $1,800 by 2030?

What’s Holding Lilly Back Right Now

Lilly is down 4.63% year to date even after a 10.37% one-month bounce and a 3.36% one-week move. Two pressures on the multiple: First, pricing. Realized prices fell 13% in Q1 as Mounjaro hit China’s national reimbursement list and U.S. cash-pay rates came down.

Second, competitive read. Novo Nordisk’s Wegovy pill is still outselling Lilly’s Zepbound at a comparable launch stage by roughly 1.5x. Add the Supreme Court rejecting Lilly’s Medicaid fraud appeal, and buyers stay cautious. Beta of 0.481 means this stock moves on earnings.

Wall Street Sees 18% Upside. Our Model Sees More

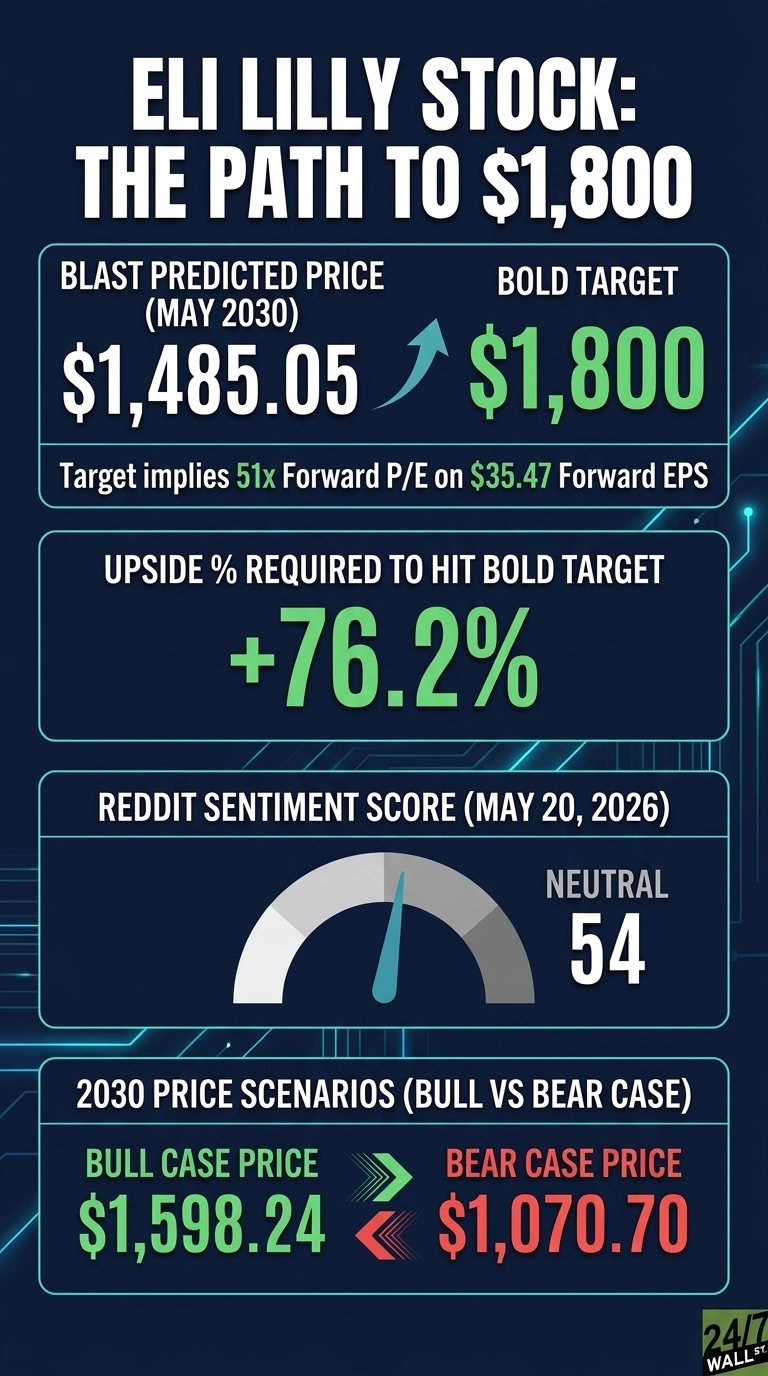

Analysts are constructive. The Street has 6 Strong Buy, 18 Buy, 6 Hold, and 1 Sell ratings, with a consensus target of $1,210. That implies roughly 18% upside. Our base-case model lands at $1,485.05 by May 2030, with a bull case of $1,598.24 and bear case of $1,070.70.

Confidence is 90%. Analysts are anchoring on near-term pricing noise and underweighting the orforglipron ramp. 77% of analysts are already bullish, and trailing earnings growth of 169.9% YoY is doing the heavy lifting that consensus has not fully priced.

The Path to $1,800 Per Share

Reaching $1,800 from today’s price of $1,021.41 requires a 76.2% gain. With forward EPS of $35.47, a price of $1,800 implies a forward P/E of 51. Our base case of $1,165.39 already implies 35x, meaning the bold target needs roughly 16 turns of additional multiple expansion on today’s EPS base.

EPS is moving fast. 2026 guidance is $35.5 to $37, up from a prior $33.5 to $35. If EPS compounds toward $60+ by 2030 on Foundayo, retatrutide and a 47% performance margin, the implied multiple at $1,800 collapses to roughly 30. That is the forward P/E compression story.

Lilly was ranked #1 in both innovation and invention by IDEA Pharma, just raised guidance to $82-$85B on Q1, and closed a $2.3B Ajax acquisition. Primary risk: orforglipron stalls against Novo’s pill or pricing reform accelerates.

Where Lilly Trades Today vs Its Earnings Power

At $1,021.41, Lilly trades at roughly 29 forward EPS. For a company guiding 28% revenue growth and 50% EPS growth in 2026, that is not expensive. Shares sit about 7% below the 52-week high of $1,130.12 and well off the 52-week low of $619.40.

The 10-year return tells the structural story: +1,504.34%. This is one of the highest-quality compounders in pharma, and the current multiple does not reflect the obesity franchise at scale.

Is $1,800 Realistic?

Reaching $1,800 by 2030 requires a 76.2% gain from here. It is a stretch but defensible.

Three things need to go right: Foundayo and retatrutide must scale globally (over 1 billion people with obesity and related conditions is the addressable pool), performance margin must hold near 48%, and capacity from the $21B+ in new U.S. and EU manufacturing must come online on schedule. A serious pricing reform shock or clinical setback on retatrutide would derail it. We’ve outlined the blueprint for how Eli Lilly could reach $1,800 in 2030.

Contact [email protected] for any questions or corrections.