Eli Lilly (NYSE:LLY | LLY Price Prediction) just delivered one of the most impressive quarters in big pharma history, and the stock is responding. After a sharp drawdown in early 2026, shares have rebounded 9.27% over the past month as Mounjaro and Zepbound continue to redefine the obesity and diabetes treatment landscape. Our 24/7 Wall St. price target points to meaningful upside from here.

The 24/7 Wall St. Price Target for Eli Lilly

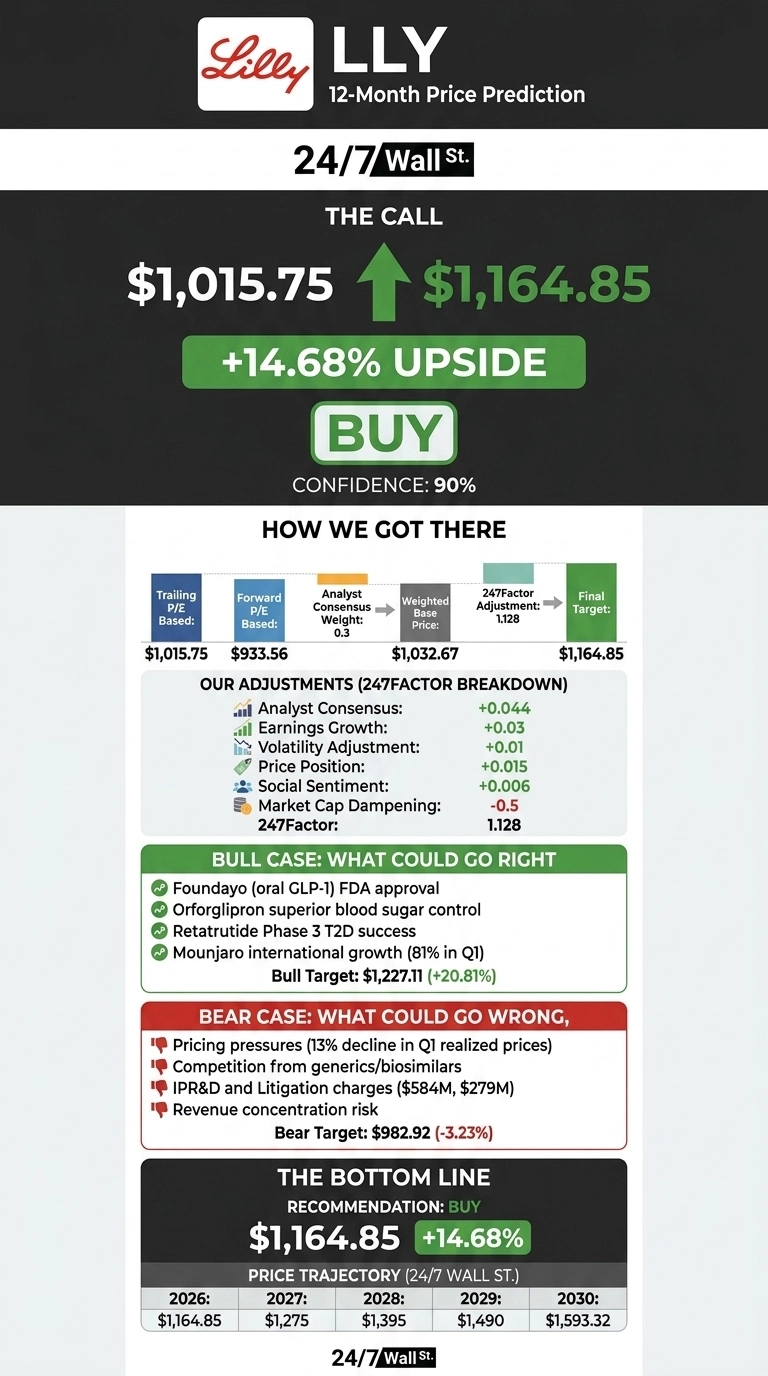

Our 24/7 Wall St. price target for Eli Lilly is $1,164.85, implying 14.68% upside from the current price of $1,015.75. We rate Lilly a buy with a 90% confidence level, reflecting strong analyst consensus, accelerating earnings, and defensive sector positioning.

| Metric | Value |

|---|---|

| Current Price | $1,015.75 |

| 24/7 Wall St. Price Target | $1,164.85 |

| Upside | 14.68% |

| Recommendation | BUY |

| Confidence Level | 90% |

Q1 Blowout Resets the Narrative

Lilly’s Q1 2026 earnings report on April 30 was the catalyst the bulls needed. Revenue came in at $19.799 billion, beating consensus by 11.25% and growing 55.55% YoY. Non-GAAP EPS of $8.55 handily beat the $6.79 consensus estimate. Mounjaro alone delivered $8.662 billion (up 125%), and Zepbound added $4.16 billion.

Management raised full-year 2026 revenue guidance to $82 billion to $85 billion and Non-GAAP EPS to $35.5 to $37. Even after the rally, LLY is still down 5.33% YTD and sits 7% below its 52-week high of $1,132.06, leaving room to run.

Why Bulls See a Breakout Ahead

The bull case rests on Foundayo (orforglipron), Lilly’s newly approved oral GLP-1 pill that requires no food or water restrictions. In a head-to-head trial published in The Lancet, orforglipron beat oral semaglutide on blood sugar and weight loss. Retatrutide, Lilly’s triple agonist, hit its Phase 3 endpoints in T2D. Add Mounjaro’s China NRDL inclusion driving 81% rest-of-world growth, and bulls have a clear path higher.

The consensus analyst target sits at $1,209.14 with 24 Buy ratings. Our bull case scenario sees LLY reaching $1,227.11 over the next 12 months, a 20.81% total return.

The Risks Worth Watching

The bear case starts with pricing. Realized prices fell 13% in Q1 as Zepbound cash pay prices dropped and China reimbursement compressed international margins. Lilly also took $584 million in IPR&D charges and $279 million in litigation and restructuring. Revenue concentration in the incretin franchise remains the central risk, and prediction markets price the federal government taking a stake at just 19%, suggesting policy noise will persist.

That said, bulls would counter that the IPR&D charge is actually down from $1.6 billion a year ago, and that 65% volume growth more than offset price declines. Our bear case lands at $982.92, a 3.23% decline.

Our Take on Lilly From Here

The price target of $1,164.85 and buy rating reflect 90% confidence in Lilly’s earnings trajectory. The tipping factor is Foundayo: an oral GLP-1 that opens a massive new patient pool without the friction of injection.

The setup looks more constructive if Foundayo’s commercial launch tracks ahead of expectations and Mounjaro keeps compounding internationally. The thesis weakens if pricing pressure accelerates beyond the 13% realized-price decline. On balance, the risk/reward skews favorably.

Looking further ahead, here is where our model projects Lilly could trade in the coming years, assuming current growth trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $1,164.85 |

| 2027 | $1,275 |

| 2028 | $1,395 |

| 2029 | $1,490 |

| 2030 | $1,593.32 |

These projections assume Lilly continues executing on its GLP-1 franchise and pipeline. Significant upside could come from retatrutide approval; downside risk centers on biosimilar competition late in the decade.

Contact [email protected] for any questions or corrections.