Retirees who want a monthly income without the wild ride of high-yield specialty funds often land on the Amplify CWP Enhanced Dividend Income ETF (NYSEARCA:DIVO). The pitch is straightforward: pair roughly 25 to 30 quality dividend stocks with a tactical covered call overlay that adds option premium on top of regular payouts. DIVO has raised $5.2 billion in assets by selling that combination to investors seeking JEPI-style income wrapped around blue-chip equity exposure. The catch is the one most DIVO holders never quite price in: the calls that fund the yield also cap a meaningful slice of the fund’s best months.

The Job DIVO Is Built To Do

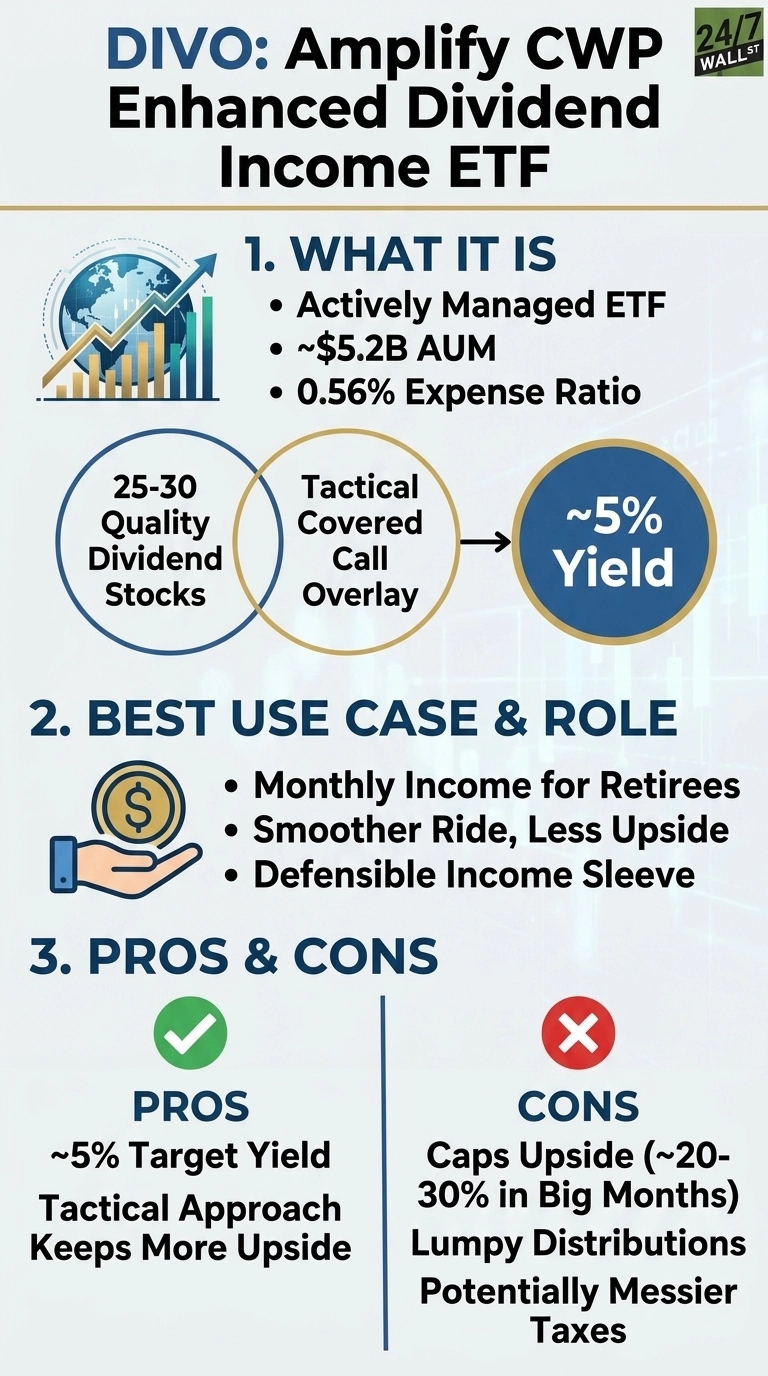

DIVO is an actively managed equity income ETF distributed by Amplify and sub-advised by Capital Wealth Planning. The core portfolio features a concentrated selection of large-cap dividend growers, and the fund carries a 0.56% expense ratio and benchmarks against the CBOE S&P 500 BuyWrite Index. Since its December 2016 launch, the overarching return engine has relied on two key components: ordinary dividends from high-quality underlying holdings and option premiums harvested by selectively selling call options on portions of the portfolio, driving total distribution yields into the 5%-6% range.

The critical operational differentiator here is tactical execution. DIVO overlays covered calls exclusively when market option premiums look highly lucrative and wraps them around chosen stock positions rather than mechanically capping upside by selling calls across the entire book every single month. This active style is engineered to capture far more equity appreciation than passive covered-call funds while generating sufficient premium income to maintain reliable monthly cash distributions to shareholders.

Capture Ratio Meets Reality

Over the past year, DIVO returned almost 18% on a price basis. The Schwab U.S. Dividend Equity ETF (NYSEARCA:SCHD), which holds quality dividend stocks but writes no calls, returned 26%. The S&P 500 returned 25%. Adding DIVO’s 5% distribution narrows the gap, but it does not disappear. Over five years, DIVO is up 65% on price, ahead of SCHD at 50% but behind the S&P 500 at 79%.

That spread is the capture ratio in action. The fund’s pattern suggests DIVO captures roughly 75% to 85% of equity upside in strong markets, meaning about 20% to 30% of the biggest monthly moves on the called positions are handed to the option buyer. Compare that to the JPMorgan Equity Premium Income ETF (NYSEARCA:JEPI), which used equity-linked notes on the S&P 500 to return about 8% over the past year. DIVO’s tactical approach kept more of the rally than JEPI’s mechanical one, and less than SCHD’s no-overlay book.

The income side delivered with DIVO paying $2.30 per share in 2025, helped by a $0.95 December special distribution reflecting unusually rich premium capture, up from $1.84 in 2024.

The Tradeoffs Inside the 5% Yield

- Capped upside-down on called names. A tech-heavy melt-up will leave DIVO trailing the index by design, and the gap shows up most in months when the called positions rip hardest.

- Lumpy distributions. The December 2025 special payout looked great in a strong year, but premium-driven income shrinks when volatility collapses and call writers get paid less for the same risk.

- Messier tax treatment. Option premium can flow through as ordinary income or short-term capital gains depending on how the calls settle, which complicates planning for taxable accounts compared with a pure qualified-dividend ETF.

Who DIVO Fits

A 67-year-old retiree allocating $250,000 to DIVO can realistically expect roughly $12,675 a year in baseline cash distribution income from high-quality blue-chip equities with a tactical hedge against full-portfolio call option risk. That remains a highly defensible income sleeve for an aging investor who has already accepted the structural trade: surrendering capital upside in roaring bull markets in exchange for a predictable monthly check and a significantly smoother portfolio ride. Investors who still require aggressive capital growth or who hold assets in taxable accounts and prioritize the tax character of distributions will likely keep more total dollars by pairing SCHD with a small cash-yield sleeve. The 5% headline payout rate is entirely real, so is the hidden opportunity cost of securing it.

Contact [email protected] for any questions or corrections.