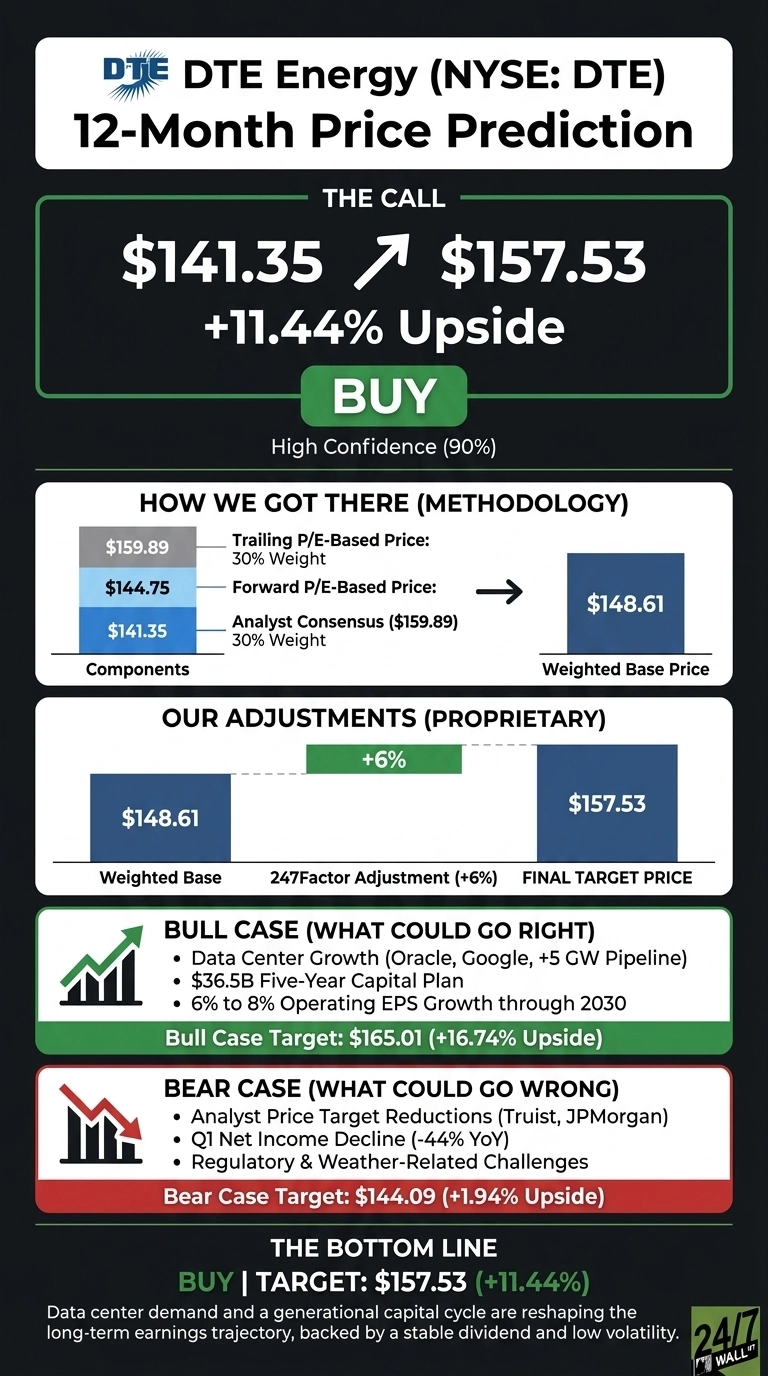

Our DTE Energy (NYSE:DTE | DTE Price Prediction) call is constructive heading into the back half of 2026. The Detroit-based utility is in the middle of a generational capital cycle, with hyperscale data center demand reshaping the long-term earnings trajectory. The 24/7 Wall St. price target for DTE Energy is $157.53, implying 11.44% upside from $141.35. We rate shares a buy with high (90%) confidence.

| Metric | Value |

|---|---|

| Current Price | $141.35 |

| 24/7 Wall St. Price Target | $157.53 |

| Upside | 11.44% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Data Center Story Wrapped in a Regulated Utility

DTE has had a constructive 2026, with shares up 10.45% year to date, even after a 3.83% pullback over the past month. The stock trades about 4% below its 52-week high of $153.72 against a low of $125.25.

Q1 2026 operating EPS came in at $1.95, missing expectations of $2.03 by 4.14%. Management reaffirmed full-year guidance of $7.59 to $7.73, with confidence in the high end due to RNG tax credits at DTE Vantage.

The bigger story is structural. DTE secured a 1.4 GW Oracle data center agreement in Saline Township and is moving a 1 GW Google project through MPSC approval, with roughly 5 GW of additional hyperscale load in late-stage negotiations. Management announced a two-year moratorium on rate hike requests after the upcoming filing, neutralizing a key political risk.

Why Bulls See a Breakout Ahead

The bull case rests on the $36.5 billion five-year capital plan, an increase of $6 billion driven by data center infrastructure. Management is guiding for 6% to 8% operating EPS growth through 2030, with potential for a CAGR above 8% from 2027 to 2030 if additional hyperscaler deals close.

Mizuho raised its price target on hyperscale demand. Our bull case scenario points to $165.01, a 16.74% return, if data center contracts ramp on schedule and the September 2026 MPSC rate case lands favorably with the requested 10.25% ROE.

What Could Go Wrong

The bear case starts with analyst sentiment. Truist trimmed its target from $165 to $158, and JPMorgan cut from $160 to $155 with a Neutral rating. Q1 net income fell 44.37% year over year, though bulls counter that timing of taxes and higher interest expense drove the decline rather than core operating deterioration.

Operating earnings at DTE Electric rose to $218 million from $147 million. Severe weather outages and tree-trimming backlash remind investors that reliability and community relations remain pressure points. Our bear case lands at $144.09.

DTE Energy Price Prediction 2026-2030

The 24/7 Wall St. price target of $157.53 reflects a constructive but disciplined view on DTE, with our recommendation set at buy and 90% confidence. The durability of the data center pipeline against a regulated rate base with a 3.14% dividend yield and beta of 0.41 tips the scale.

I’d be a buyer here if the September 2026 MPSC order approves the requested ROE and Google contracts clear. I’d stay on the sidelines if data center deals slip into 2027 or the equity issuance plan of $500 to $600 million annually dilutes EPS faster than rate base growth offsets it.

Looking ahead, here is where our model projects DTE could trade, assuming current growth trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $157.53 |

| 2027 | $170.13 |

| 2028 | $183.66 |

| 2029 | $195.48 |

| 2030 | $207.25 |

These projections assume DTE executes on its capital plan. Significant upside could come from additional hyperscaler contracts beyond the current pipeline, while downside risk centers on regulatory disallowances or stranded asset exposure if data center demand softens.

Contact [email protected] for any questions or corrections.