Rambus (NASDAQ:RMBS | RMBS Price Prediction) has been one of the loudest AI memory winners of the past year, with shares up 162.25% over the trailing 12 months and 55.6% year to date. After that move, my proprietary model says the easy money has been made.

The 24/7 Wall St. Price Target Says Take Some Off the Table

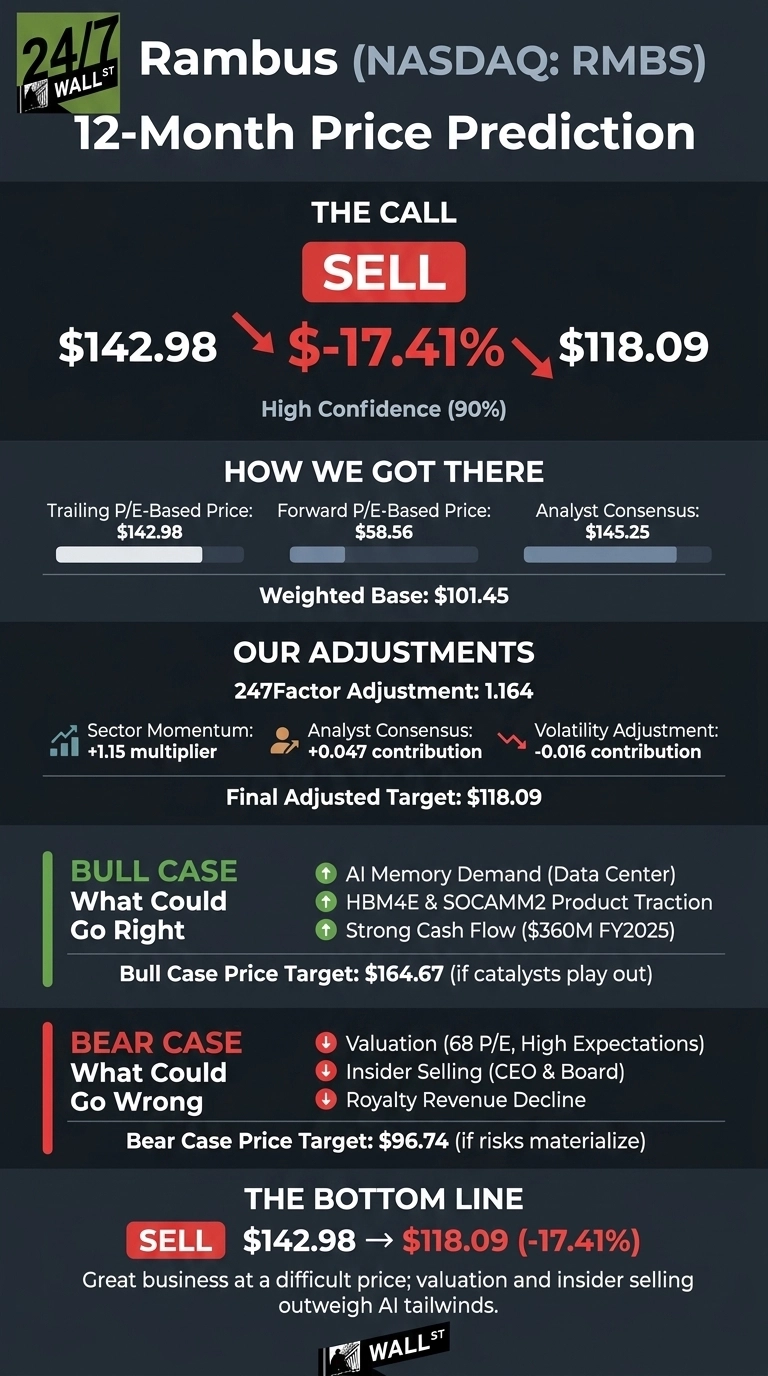

Our 24/7 Wall St. price target for Rambus is $118.09, against a current price of $142.98. That implies 17.41% downside over the next 12 months, and our recommendation is sell. Confidence on the model is high at 90%, reflecting strong analyst data, clean earnings history, and a stretched valuation profile.

| Metric | Value |

|---|---|

| Current Price | $142.98 |

| 24/7 Wall St. Price Target | $118.09 |

| Upside/Downside | -17.41% |

| Recommendation | SELL |

| Confidence Level | 90% |

Why We Could Be Wrong

Our 24/7 Wall St. price target of $118.09 sits below where Rambus trades today, and the bull narrative is real. HBM4E controller IP described as the industry’s fastest and the LPDDR5X SOCAMM2 server chipset could re-rate the multiple if hyperscaler design wins accelerate. Treat our number as one datapoint.

A Rally Built on AI Memory Demand

RMBS is up 12.54% in the past week and 8.69% over the past month, sitting roughly 10% off its 52-week high of $161.80.

The catalyst has been AI memory. Q1 2026 revenue came in at $180.19 million, up 8.1% YoY, with product revenue of $88 million growing 15% YoY on data center demand. Non-GAAP EPS of $0.63 missed the $0.6363 consensus by 0.99%, and an analyst downgrade flagging tightening DRAM supply briefly pressured shares before the recent rebound.

The Case for $165+

Bulls have a clean thesis. FY2025 revenue grew 27.13% to $707.63 million, with operating income up 45.34% and operating cash flow hitting $360 million. Q2 2026 product revenue is guided to $95 to $101 million, marking another sequential record.

CEO Luc Seraphin noted that “the growth of AI inference and agentic workloads in the data center continues to drive demand for higher memory bandwidth.” Our bull scenario lifts RMBS to $164.67, a 15.17% gain, broadly in line with the 7 buy ratings and $145.25 average analyst target.

What Could Go Wrong

The bear case starts with valuation and ends with insiders. Royalty revenue declined from $74 million to $69.6 million YoY, R&D rose 18%, and non-GAAP operating margin compressed from 46% to 42%. Bulls counter that the R&D step-up funds HBM4E and SOCAMM2 IP that should monetize through 2027.

CEO Luc Seraphin executed 10 separate sell transactions across March and April, and four board members have sold recently, including Necip Sayiner selling 9,824 shares at $130.18 on May 8. Our bear scenario points to $96.74, a 32.34% decline.

Rambus Price Prediction 2026-2030

The 24/7 Wall St. price target of $118.09 and sell rating at 90% confidence reflect a great business at a difficult price. The tipping factor is the gap between a 68 P/E and 8.1% Q1 revenue growth. A pullback to the $115 to $120 range or a re-acceleration in royalty revenue would meaningfully improve the risk/reward, while continued CEO selling and tightening DRAM supply argue for patience.

Here is where our model projects RMBS could trade, assuming current growth trajectories and AI memory demand hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $118.09 |

| 2027 | $112.00 |

| 2028 | $108.00 |

| 2029 | $107.00 |

| 2030 | $107.17 |

These projections assume Rambus continues executing on DDR5 and HBM IP monetization. Material upside could come from a hyperscaler design-win at HBM4E or accelerating royalty billings.

Contact [email protected] for any questions or corrections.