Few mega-caps have ridden the AI infrastructure wave as cleanly as Broadcom (NASDAQ:AVGO | AVGO Price Prediction). With AI semiconductor revenue compounding at triple-digit rates and CEO Hock Tan publicly targeting $100 billion in AI sales by 2027, the question is no longer whether the company can grow, but how much of that growth is already priced in. Our 24/7 Wall St. price target frames the answer.

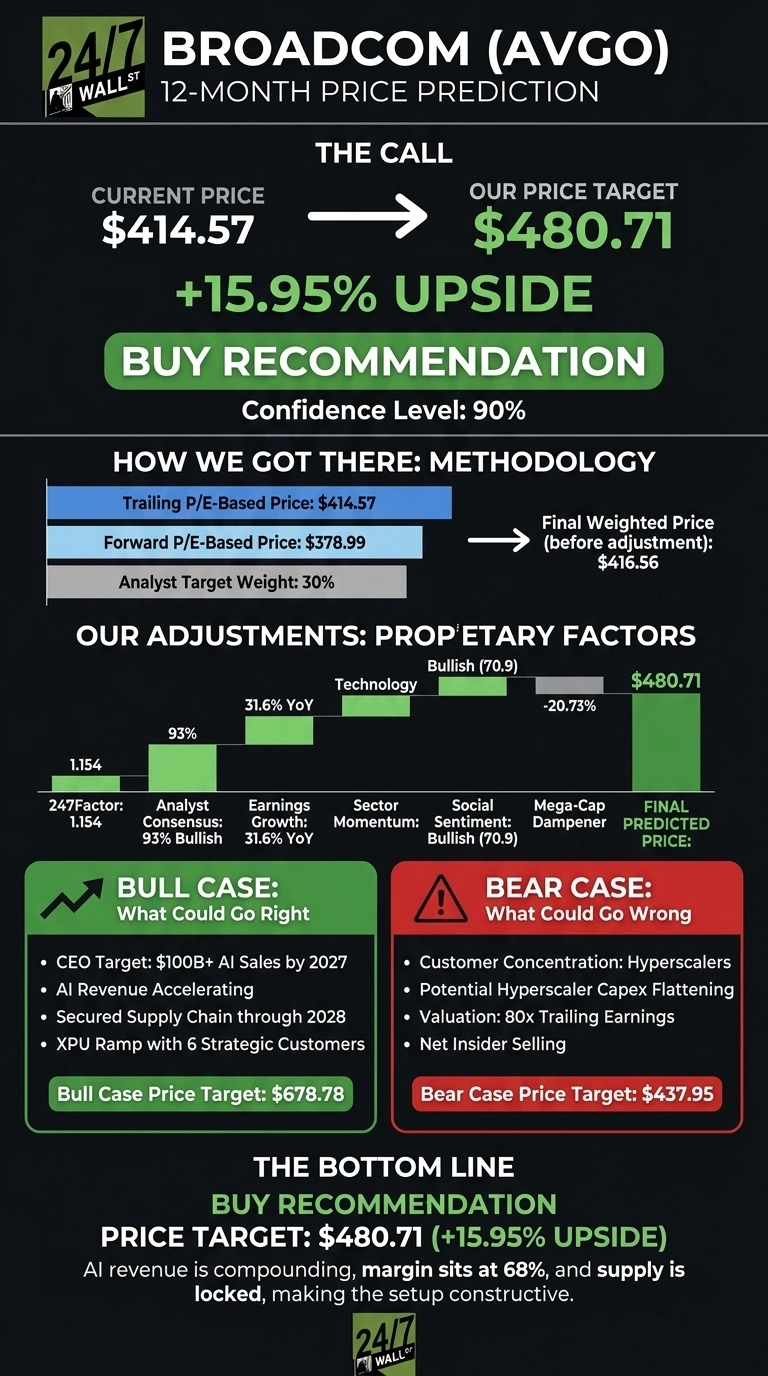

The 24/7 Wall St. price target for Broadcom is $480.71 over the next 12 months, pointing to 15.95% upside from the current price of $414.57. Our recommendation is buy, with confidence at 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $414.57 |

| 24/7 Wall St. Price Target | $480.71 |

| Upside | 15.95% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Record Quarter and a Cooling Stock

AVGO is up 20.02% year to date and 81.91% over the past year, though shares have slipped 5.73% in the past week and sit 9% below the 52-week high of $442.36.

Q1 FY2026 results, reported March 4, set the bull narrative. Revenue hit $19.31 billion, up 29.47% YoY, with non-GAAP EPS of $2.05 beating estimates. AI semiconductor revenue surged 106% YoY to $8.40 billion, and adjusted EBITDA margin reached a record 68%. Q2 guidance calls for revenue of $22 billion (+47% YoY) with AI revenue accelerating to $10.7 billion.

Why Bulls See a Breakout Ahead

Bulls argue the model still understates AVGO’s optionality. On the Q1 call, Hock Tan disclosed “line of sight to achieve AI revenue from chips, just chips, in excess of $100 billion in 2027” with capacity secured through 2028. The XPU franchise now spans six strategic customers including Google, Meta, Anthropic and a newly disclosed OpenAI deployment of over 1 gigawatt in 2027.

AI networking is scaling toward 40% of total AI revenue. Polymarket assigns a 97.1% probability of beating next earnings. If AI revenue runs ahead of plan, our bull case 2030 target is $678.78.

The Risks Worth Watching

The bear case is concentration risk. A handful of hyperscalers drive the AI book, and any pause in capex could compress growth fast. AVGO trades at 80x trailing earnings and 29x sales, leaving little room for error. 112 recent insider transactions skew net selling.

Counterpoint: insider sales at mega-caps often reflect routine compensation cycles, and the PEG of 0.894 suggests growth justifies the multiple. Our bear case 2030 target is $437.95.

Execution Is the Decisive Factor

Our 24/7 Wall St. price target of $480.71 reflects a buy rating at 90% confidence. The decisive factor is execution. AI revenue is compounding faster than the multiple, EBITDA margin sits at 68%, and supply is locked through 2028.

The setup looks constructive if AI revenue stays on the path to $100 billion by 2027. The thesis weakens if hyperscaler capex begins to flatten or custom silicon competition intensifies materially.

Broadcom Price Prediction 2026-2030

Looking further ahead, here is where the 24/7 Wall St. price target model projects AVGO could trade, assuming current growth and margin trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $418.65 |

| 2027 | $485.59 |

| 2028 | $549.12 |

| 2029 | $573.94 |

| 2030 | $613.02 |

These projections assume Broadcom continues converting hyperscale AI demand into custom silicon wins. Significant upside or downside could result from the trajectory of AI capex and the cadence of XPU deployments at Google, Meta, OpenAI and Anthropic.

Contact [email protected] for any questions or corrections.