The stock-split conversation is heating up again. KLA announced a 10-for-1 forward split in May 2026, and Booking Holdings completed a 25-for-1 split announced in February 2026. With two marquee names in the four-digit club resetting their share prices in the same year, investors are combing through the rest of the high-priced list looking for the next candidate.

Among the names mentioned most often are ASML Holding (NASDAQ: ASML | ASML Price Prediction), GE Vernova (NYSE: GEV), SanDisk (NASDAQ: SNDK), and United Rentals (NYSE: URI). None has announced a split, hinted at one in filings, or telegraphed board action. The ranking below reflects structural likelihood based on nominal price, recent run-up, retail appeal, and sector precedent, counting down from least likely to most likely.

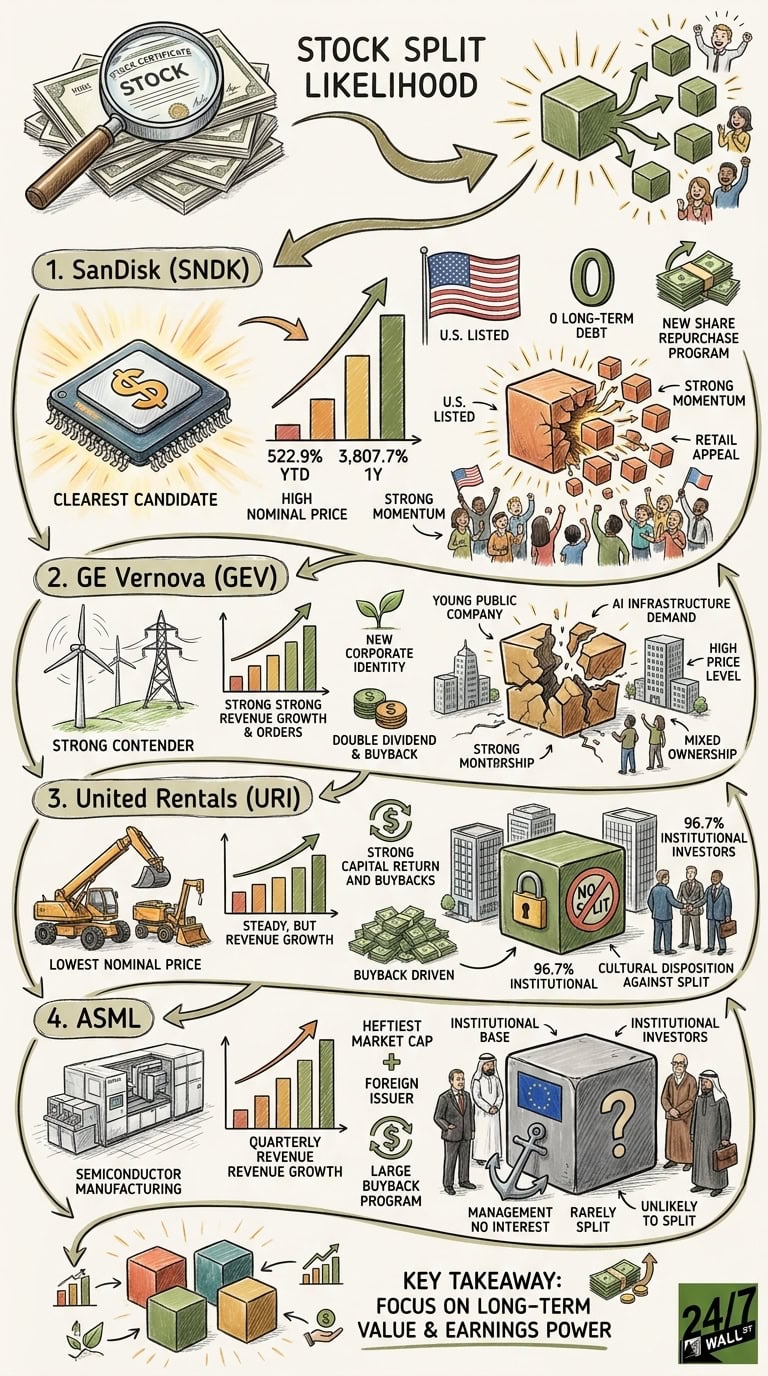

4. ASML

ASML carries the heftiest market cap at roughly $629.3 billion, with American depository receipts (ADRs) recently at $1,632.90 after a 122.9% one-year gain. Q1 2026 earnings showed quarterly revenue growth of 13.2% year over year and a trailing P/E of 54x. The company announced a new €12 billion buyback program running through December 2028 and lifted its FY25 dividend.

The bull case: four-digit ADR price and surging AI-driven lithography demand. The bear case is stronger. ASML is a Dutch-domiciled foreign issuer whose ADRs rarely split. Its shareholder base skews heavily institutional, and management has shown no interest in resetting the price. With analysts targeting $1,663.96 and a deep European holder base accustomed to high nominal prices, a split would be out of character. ASML lands at #4.

3. United Rentals

United Rentals trades at $938.62, the lowest nominal price in this group, with a market cap of about $58.8 billion. Q1 2026 produced adjusted EPS of $9.71 versus $8.94 expected on $3.985 billion in revenue, up 7.15% year over year. Management raised 2026 guidance to $16.9 billion to $17.4 billion in revenue. Capital return is robust: a fresh $5 billion buyback authorization and a quarterly dividend lifted 10% to $1.97.

Insider activity tells the story. Nine directors acquired 203 shares each at $937.00 on May 8, 2026, while CEO Matthew Flannery disposed of 22,768 shares at $984.976 on April 24, 2026. United Rentals has never executed a stock split. Its run-up has been buyback-driven and its shareholder base is 96.7% institutional. Without a retail catalyst, the cultural disposition leans against a split.

2. GE Vernova

Spun off from General Electric in April 2024, GE Vernova trades at $1,038.74 with a market cap near $279.1 billion. Q1 2026 delivered $9.30 billion in revenue, up 15.79% year over year, orders of $18.3 billion (up 71% organically), and an Electrification book-to-bill near 2.5x. Management raised 2026 guidance to $44.5 billion to $45.5 billion in revenue, doubled the dividend to $0.50 per quarter, and expanded its buyback authorization to $10 billion.

CEO Scott Strazik told investors, “our backlog growing by more than $13 billion quarter-over-quarter,” fueled by data center and AI infrastructure demand. The bull case: a young, retail-loved AI infrastructure name approaching four-digit territory with a one-year gain of 126.4%. The bear case: institutional ownership of 79.2% and a leadership team prioritizing buybacks and dividend growth over cosmetic actions. The combination of price level, AI narrative, and fresh corporate identity puts GE Vernova at #2.

1. SanDisk

SanDisk is the clearest structural split candidate. The pure-play NAND name trades at $1,478.69, the highest nominal price in the group, with a market cap of roughly $219.0 billion. The chart tells a staggering story: up 522.9% year to date and 3,807.7% over the past year.

Fundamentals justify the move. Q3 FY2026 delivered non-GAAP EPS of $23.41 versus $14.66 consensus on $5.95 billion in revenue, up 251.03% year over year, with gross margin of 78.4%. The Datacenter segment grew 645% year over year to $1.47 billion. Guidance for Q4 calls for revenue of $7.75 billion to $8.25 billion and non-GAAP EPS of $30.00 to $33.00. CEO David Goeckeler said, “This quarter marks a fundamental inflection point for Sandisk where our technology leadership is enabling a deliberate shift in our mix toward the highest-value end markets, led by Datacenter.”

This is the bull case: highest nominal price of the four, U.S.-listed, recent spin-off from Western Digital, zero long-term debt after $650 million in debt repayment, and a newly authorized share repurchase program. On the other hand, SanDisk is a young public company still establishing its capital-return identity, and management has not signaled split intent. On every structural factor that matters, though, SanDisk leads the pack.

Key Takeaway for Investors

None of these four has announced or signaled a stock split. Splits are cosmetic: market cap, fundamentals, and intrinsic value remain unchanged. What they can shift is retail demand, options accessibility, and short-term sentiment. If the four-digit club continues to thin behind KLA and Booking, SanDisk’s combination of nominal price, momentum, and U.S.-listed structure makes it the most natural next candidate, with GE Vernova a credible second. ASML and United Rentals look unlikely to follow that path, though both continue returning capital aggressively through buybacks and dividends. Earnings power and cash flow drive long-term value far more than split mechanics.

Contact [email protected] for any questions or corrections.