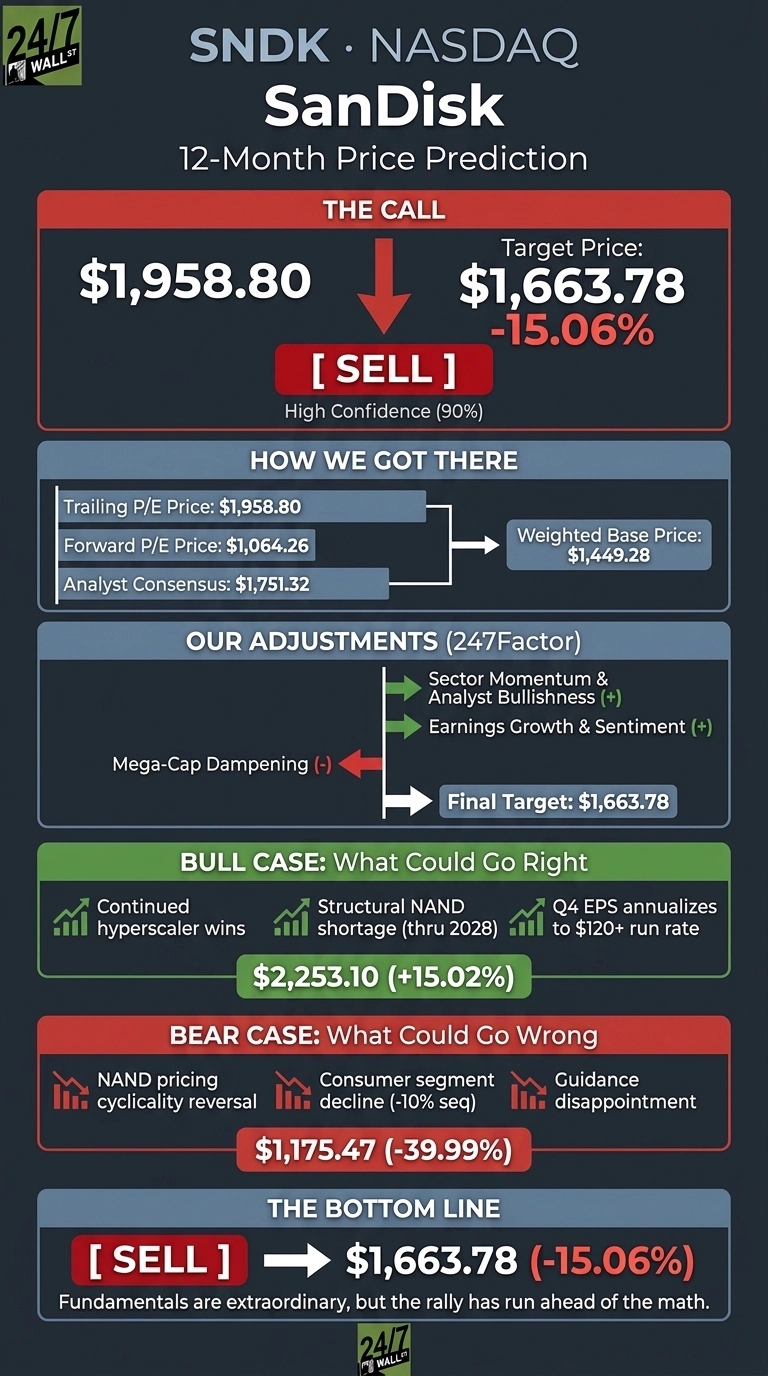

After one of the most extraordinary rallies in semiconductor history, SanDisk (NASDAQ:SNDK | SNDK Price Prediction) sits at $1,958.80 after climbing 725.17% year to date and 4,342.73% over the past year.

Our 24/7 Wall St. price target for SanDisk is $1,663.78 over the next 12 months, implying 15.06% downside and a sell recommendation at a 90% confidence level. The thesis is simple: fundamentals are extraordinary, but the rally has run ahead of even the bull math.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $1,958.80 |

| 24/7 Wall St. Price Target | $1,663.78 |

| Upside/Downside | -15.06% |

| Recommendation | SELL |

| Confidence Level | 90% |

A Note Before We Begin

SanDisk has become one of the most divisive stocks in the market, and real upside could come from continued hyperscaler datacenter wins or a structural NAND shortage extending through 2028. Our 24/7 Wall St. price target sits below today’s price, but consider it one datapoint among many. A detailed bull case appears below outlining why SNDK could keep outperforming our model.

How a $44 Stock Became a $1,958 Stock

SanDisk has surged from $44.21 in June 2025 to today’s level, gaining 46.95% in the past month alone.

The catalyst is undeniable: Q3 FY26 revenue hit $5.95 billion, up 251.03% year over year, with EPS of $23.41 crushing the $14.66 consensus by 59.67%. Datacenter revenue exploded 645% YoY to $1.467 billion, and gross margin expanded to 78.4% from 22.5%. Sandisk also retired $650 million in debt and now carries zero long-term obligations.

Why Bulls See a Breakout Ahead

The bull case is real. Q4 FY26 guidance calls for revenue of $7.75 billion to $8.25 billion with non-GAAP EPS of $30 to $33. CEO David Goeckeler called the quarter “a fundamental inflection point for Sandisk where our technology leadership is enabling a deliberate shift in our mix toward the highest-value end markets, led by Datacenter.”

Five signed multi-year New Business Model agreements lock in hyperscaler demand, BiCS8 is scaling toward majority bit production, and High Bandwidth Flash positions Sandisk for AI inference workloads. If Q4 EPS annualizes to a $120-plus run rate and the structural NAND shortage holds through 2028, the bull scenario reaches $2,253.10 within a year, or $2,906.86 over five years.

The Risks Worth Watching

The bear case centers on cyclicality. NAND pricing has historically reversed sharply once supply catches up, and Sandisk’s Consumer segment already declined 10% sequentially in Q3. The stock trades at a trailing P/E of 72 and a forward P/E of 33, leaving little room for guidance disappointment.

The bear scenario lands at $1,175.47, a 39.99% drawdown. Bulls would counter that elevated trailing multiples reflect the prior $1.83 billion goodwill impairment in FY25, and forward earnings power is structurally higher post-separation from Western Digital.

SanDisk Price Prediction 2026-2030

My 24/7 Wall St. price target of $1,663.78 with 90% confidence supports a sell rating, with risk skewed asymmetrically to the downside.

The model turns more constructive on a pullback toward the $1,400 area provided datacenter revenue keeps growing triple digits. It stays cautious if Q4 reports in line and shares hold above $1,900, because the math no longer rewards the entry at current levels.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $1,663.78 |

| 2027 | $1,720 |

| 2028 | $1,680 |

| 2029 | $1,620 |

| 2030 | $1,558.96 |

These projections assume Sandisk continues executing on hyperscaler NBM agreements and BiCS8 ramp. Significant upside could materialize if HBF becomes a standard for AI inference, while a NAND price cycle reversal in 2027 or 2028 could push outcomes toward the bear path.

Contact [email protected] for any questions or corrections.