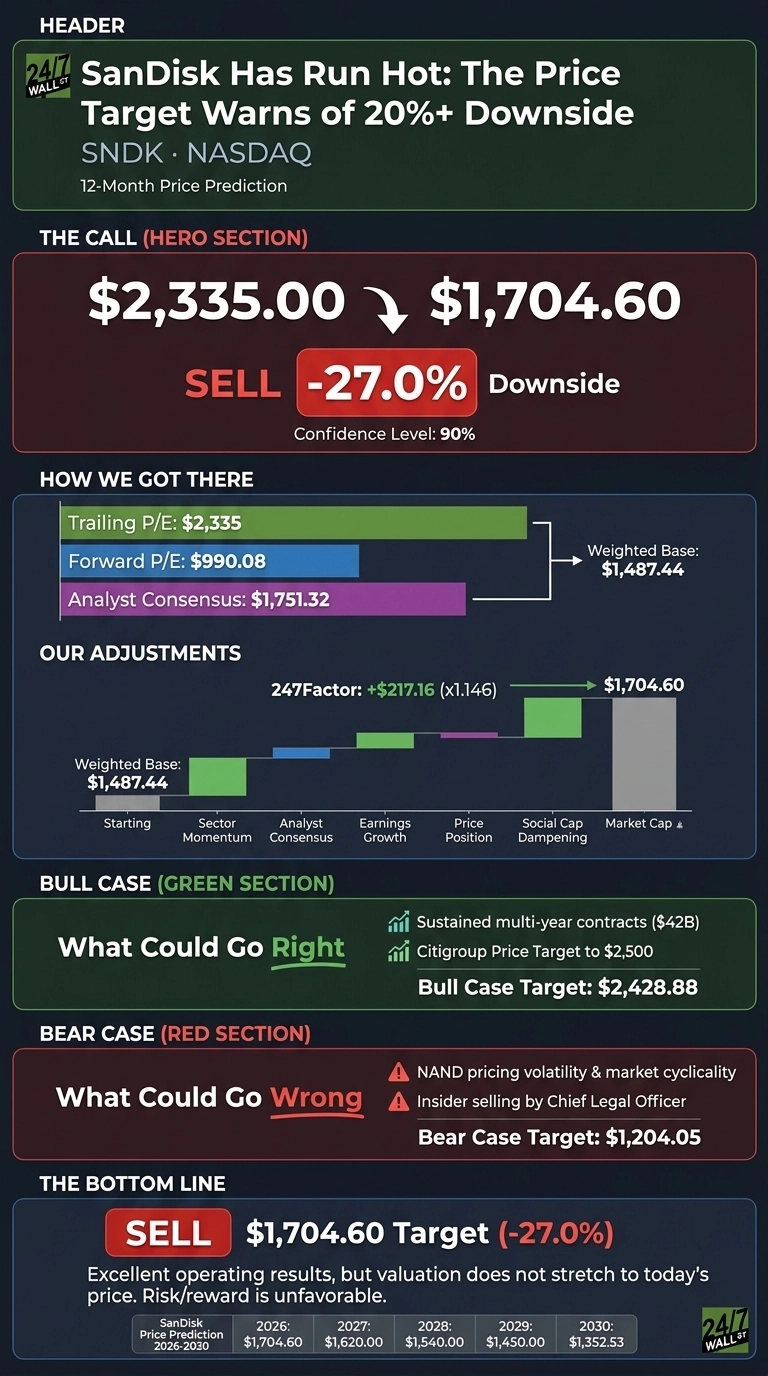

SanDisk (NASDAQ:SNDK | SNDK Price Prediction) has gone vertical. Shares have rallied 4,841.8% over the past year on an AI memory supercycle. Our 24/7 Wall St. price target for SanDisk is $1,704.60, implying meaningful downside from current levels even after the company’s transformation into a structurally more profitable business.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $2,335.00 |

| 24/7 Wall St. Price Target | $1,704.60 |

| Upside/Downside | -27.0% |

| Recommendation | SELL |

| Confidence Level | 90% |

Our recommendation is sell with 90% model confidence. SanDisk’s operating results are excellent, but the stock trades well above where consensus analyst work and our proprietary multiples justify.

Why We Could Be Wrong

SanDisk is one of the most divisive stocks in the market. Real upside could come from sustained $42B in multi-year contracted supply deals, a memory shortage analysts expect to persist through 2028, or continued hyperscaler ramp. Citigroup just lifted its target to $2,500. Treat our target as one datapoint among many.

From $41 to $2,335 in Ten Months

SanDisk is up 883.65% year to date and 46.9% in the past month, sitting 26% below a 52-week high of $2,354.39.

The Q3 FY26 report on April 30, 2026 was the catalyst: EPS of $23.41 against $14.66 consensus, revenue of $5.95 billion (251% YoY), and gross margin expansion to 78.4% from 22.5% a year earlier. Datacenter revenue jumped 645% YoY to $1.467 billion. Management retired $650 million in debt and now operates with zero long-term debt.

Why Bulls See a Breakout Ahead

The bull case rests on SanDisk’s transformation. CEO David Goeckeler called Q3 a “fundamental inflection point” driven by a new business model of multi-year customer engagements backed by firm financial commitments. Q4 FY26 guidance points to revenue of $7.75B to $8.25B and non-GAAP EPS of $30 to $33.

Citigroup at $2,500, Mizuho at $2,200, and Street targets at $3,250 argue SanDisk can compound from here. The 247Factor bull case puts shares at $2,428.88 in twelve months if contracted revenue holds and AI memory tightness persists into 2028.

The Risks Worth Watching

SanDisk is a pure-play NAND name dependent on the Kioxia joint venture and a small set of hyperscalers. Memory has historically cycled hard. Monthly RSI of 99.14 screams overbought, and Morgan Stanley has flagged valuation.

Chief Legal Officer Bernard Shek sold $1.04M in stock on June 6, 2026. Bulls counter that the contracted NBM book and zero-debt balance sheet structurally dampen past cyclicality. Our bear case lands at $1,204.05, a 48.43% drawdown.

The Risk Isn’t Worth the Reward Here

Verdict: Sell, with our 24/7 Wall St. price target at $1,704.60 and 90% confidence. Even applying a generous 75x forward multiple, the math does not stretch to today’s price.

The bull thesis strengthens if SanDisk locks in another wave of NBM contracts extending earnings power into FY28. The bear thesis strengthens if NAND spot pricing softens or a hyperscaler pushes back on commitments. After a 4,841.8% year, the risk/reward at current levels looks unfavorable on our model.

Here is where our model projects SanDisk could trade, assuming current trajectories and memory market conditions hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $1,704.60 |

| 2027 | $1,620.00 |

| 2028 | $1,540.00 |

| 2029 | $1,450.00 |

| 2030 | $1,352.53 |

These projections assume SanDisk continues executing on its NBM contract strategy. Significant upside or downside could result from a longer-than-expected memory shortage or cyclical NAND pricing pressure resurfacing late in the decade.

Contact [email protected] for any questions or corrections.