Oklo (NYSE:OKLO | OKLO Price Prediction) has become a poster child for the nuclear renaissance powering the AI buildout, and the advanced fission developer just stacked another regulatory and fuel-supply win onto a thesis built entirely on future revenue.

The Santa Clara company has been selected by the U.S. Department of Energy for advanced negotiations under the Surplus Plutonium Utilization Program, chosen alongside four other advanced nuclear companies. The program converts designated surplus plutonium material into fuel for advanced reactors, and Oklo is pairing it with a partnership with European developer newcleo that could bring up to $2 billion in project capital, subject to definitive agreements.

CEO Jacob DeWitte framed why this matters:

“Fuel supply constraints are a key throttle to advanced reactor development. This program creates a pathway to use existing surplus material as bridge fuel for advanced reactors to bring more reactors online sooner.”

Regulatory Momentum Is Stacking Up

The plutonium news lands on top of the NRC’s May 6, 2026 approval of Oklo’s Principal Design Criteria topical report for the Aurora powerhouse on an accelerated schedule, a milestone that sent shares up 12% to 22.5% on the day. Next up is a July 4, 2026 criticality target for the Groves Isotope Test Reactor at Idaho National Laboratory.

DeWitte has consistently leaned into the AI tailwind:

“We are entering an era of unprecedented energy demand, rivaled perhaps only by initial conversion to electrification over a century ago.”

That demand is showing up in the order book. The customer pipeline has expanded to roughly 14 GW, anchored by a 1.2 GW Meta Platforms agreement, a 12 GW non-binding master power agreement with Switch, and a 500 MW Equinix LOI backed by a $25 million pre-payment.

Pre-Revenue, With Losses Widening

The catch: Oklo still generates no commercial revenue. The Q1 2026 net loss came in at $33.1 million, or $0.19 per share, versus a $9.8 million loss in Q1 2025. Trailing EPS sits at -$0.84.

Management has the cash to wait. The balance sheet held $2.54 billion in cash and marketable securities at the end of Q1, fortified by a $1.2 billion equity raise and a new $1 billion ATM facility launched May 13, 2026. First commercial power is targeted for late 2027 to early 2028 at INL.

How the Street and Retail Are Reading It

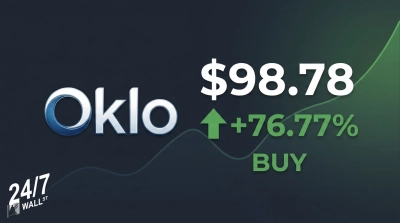

Shares trade at $65.88, up 65.86% over the past year but down 8.19% year to date. The analyst consensus target sits at $88.74, with Bank of America at $80 (Buy) and Tigress Financial at $130.

lass=”yoast-text-mark” />>

>

Reddit chatter mirrors the split. The NRC approval drove sentiment scores of 66 to 70 on r/stocks, while a May 10 bearish dip registered an 18 score. Keep an eye on the stock as the July criticality test and a COLA filing decision frame the next leg of this commercialization story.

Contact [email protected] for any questions or corrections.