Occidental Petroleum (NYSE:OXY | OXY Price Prediction) and Exxon Mobil (NYSE:XOM) just closed earnings chapters that read like opposite playbooks. Occidental wrapped fiscal 2025 by selling its chemicals arm to Berkshire and shrinking into a focused driller.

Exxon opened Q1 2026 by loading its first Golden Pass LNG cargo and buying back nearly $5 billion in stock. With WTI at $101.56, the comparison matters.

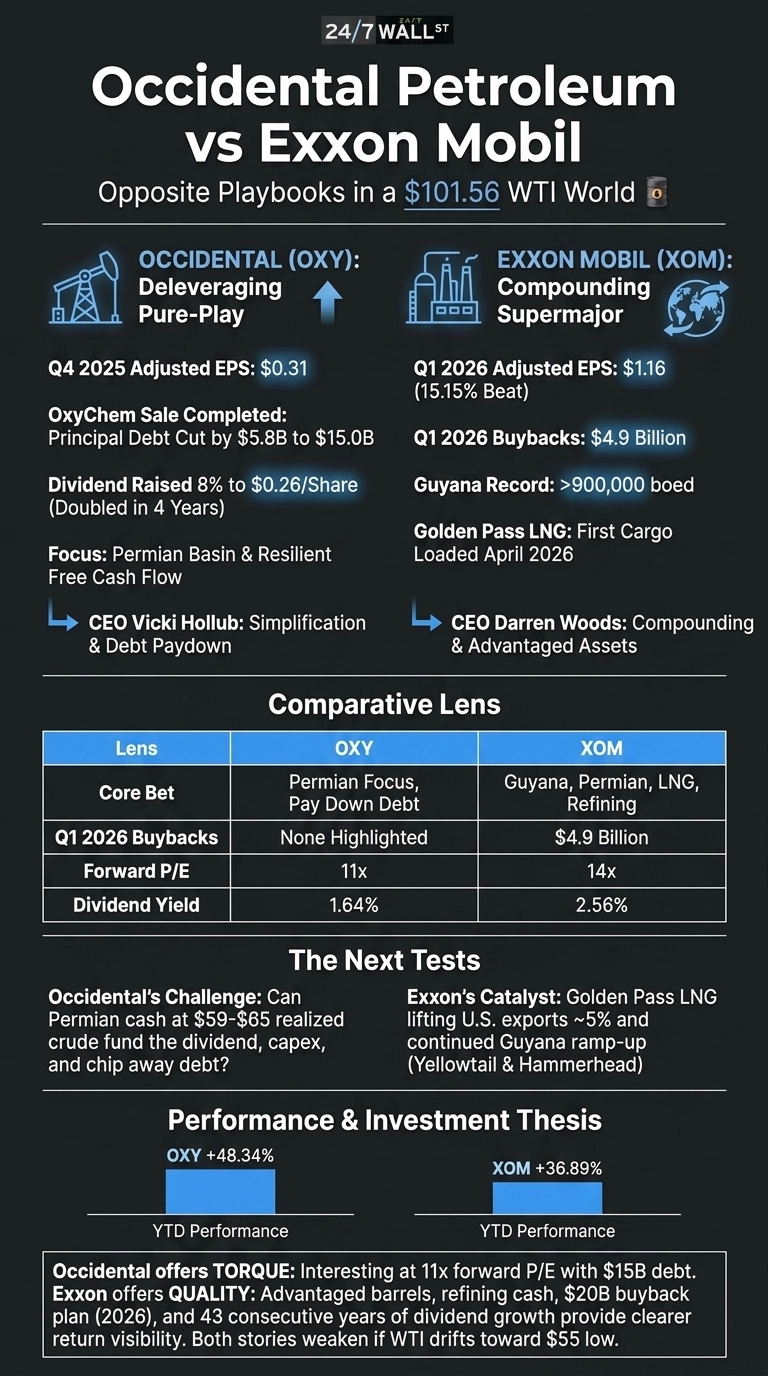

Shrinking Pure-Play Meets Scaling Supermajor

Occidental’s Q4 was about subtraction. Adjusted EPS came in at $0.31 on revenue of $5.42 billion, with a $68 million net loss tied to the OxyChem sale. Production beat guidance at 1,481 Mboed, and the Permian carried the quarter.

CEO Vicki Hollub framed the moment plainly: “With our enhanced balance sheet following the sale of OxyChem, we remain focused on generating resilient free cash flow.” The Berkshire deal cut principal debt by $5.8 billion to $15 billion, and the dividend rose 8% to $0.26 per share.

Exxon’s quarter was about scale absorbing shocks. Adjusted EPS hit $1.16, beating the $1.01 consensus by 15.15%, while revenue of $85.14 billion landed roughly in line. Headline net income of $4.18 billion absorbed $3.88 billion in mark-to-market derivative timing and $706 million in Middle East disruption losses. Underlying earnings were $8.77 billion. Guyana cleared 900,000 gross barrels per day, a record.

A Deleveraging Story vs. a Compounding Machine

| Lens | Occidental | Exxon |

| Core bet | Permian focus, pay down debt | Guyana, Permian, LNG, refining |

| Q1 2026 buybacks | None highlighted | $4.9 billion |

| Forward P/E | 11x | 14x |

| Dividend yield | 1.64% | 2.56% |

Hollub is simplifying. Woods is compounding. Exxon’s structural cost savings since 2019 reached $15.6 billion, with a $20 billion buyback planned for 2026 and 43 consecutive years of dividend growth. Occidental’s beta of 0.17 understates its operating leverage to crude. That low forward multiple is the market pricing a debt overhang that is now meaningfully smaller.

The Next Tests Are LNG Cargoes and Permian Cash

I am watching Golden Pass closely. Train 1’s first cargo loaded in April 2026, lifting U.S. LNG exports roughly 5% versus 2025. If Hammerhead and Yellowtail keep Guyana ramping, Exxon’s earnings power widens regardless of Brent’s path.

For Occidental, the question is whether free cash flow at $59 to $65 per barrel realized crude can fund the dividend, fund Permian capex, and keep chipping at the remaining debt. The stock has already moved: shares are up 48.34% year to date, with Exxon up 36.89%.

Exxon Offers Quality, Occidental Offers Torque

For the next twelve months, the setups diverge sharply. The combination of advantaged barrels, refining cash, and the $20 billion buyback gives me a clearer line of sight to returns even if oil cools from $101.

Occidental fits a different investor. If you want torque to crude and believe Hollub’s simpler company deserves a re-rate, the 11x forward multiple is interesting, especially with debt at $15 billion rather than $20 billion. Both stories weaken if WTI drifts back toward the $55 low printed last December. Quality compounds. Pure-play torque cuts both ways.