Super Micro Computer (NASDAQ:SMCI | SMCI Price Prediction) just printed $10.24 billion in Q3 FY2026 revenue, up 122.68% year over year, while CEO Charles Liang declared that “Supermicro’s transformation into a total datacenter infrastructure provider is accelerating.”

Shares are up 41.1% year to date, yet still sit miles below last cycle’s highs. Can SMCI reach $60 per share in 2027?

Why SMCI Shares Are Stuck Below Their Old Highs

The recent ramp is real, but the year-long picture is messier. SMCI is down 1.57% over the trailing twelve months and sits 40% below its 52-week high of $62.36. The overhang is governance.

Results remain preliminary and unaudited as the Board conducts an independent review of export-control matters. Margins have been the other wound. GAAP gross margin compressed to 6.3% in Q2 FY2026 from 11.8% a year earlier before clawing back to 9.9% in Q3.

Add $8.8 billion in total debt and convertibles and a beta of 1.684, and you have a stock that punishes any whiff of bad news. The one-week move of 23.43% shows the volatility cuts both ways.

Wall Street Is Cautious. Too Cautious.

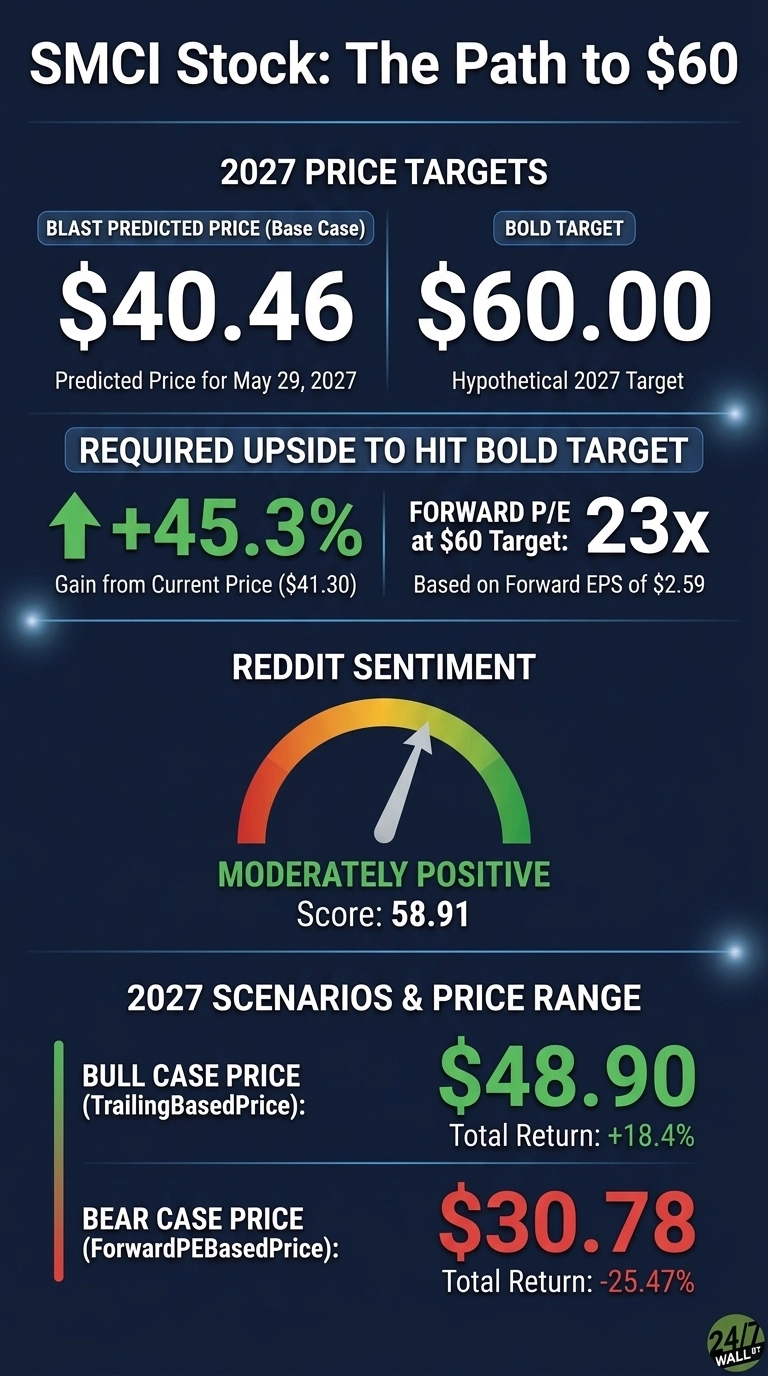

The Street consensus is uninspired. The average analyst target sits at $37.12, with a rating split of 2 Strong Buys, 3 Buys, 9 Holds, 2 Sells, and 2 Strong Sells. Only 28% of analysts are bullish.

Our internal base case puts 2027 fair value at $40.46, with an optimistic scenario at $48.90 and a bear case of $30.78, all carried at a 90% confidence.

Here’s my pushback. Full FY2026 guidance was raised to $38.90 to $40.40 billion, nearly double FY2025’s $21.97 billion. Analysts are anchored to the margin scare. If the audit clears and DCBBS scales, the consensus target looks stale by Q1 2027.

The Path to $60 Per Share

Reaching $60 from today’s price of $41.30 would require a gain of 45.3%. With forward EPS of $2.59, a price of $60 implies a forward P/E of 23x. Our base case of $40.46 already implies 18x, meaning the bold target needs roughly 5x of additional multiple expansion.

That is achievable if the EPS denominator keeps moving up. Q3 FY2026 non-GAAP EPS beat consensus by 34.51% and Q2 FY2026 beat by 41.42%.

Liang has pointed to “more than $13B in Blackwell Ultra orders” and said Supermicro is “exceptionally well-positioned to meet the massive demand for various AI and enterprise verticals” as new Silicon Valley manufacturing comes online.

If margins normalize toward FY2025’s 11.1% GAAP gross margin average, the forward multiple compresses as EPS grows into the price. The risk: the export-control review delivers a worse outcome than expected.

The Valuation Case for SMCI Right Now

SMCI trades at a current forward P/E of roughly 16x, well below the trailing 20x and a PEG ratio of 0.913. Shares sit between the 52-week low of $19.48 and high of $62.36. Long-term holders have been rewarded: SMCI is up 1,485.41% over the past decade. A sub-PEG, sub-20 multiple on a business compounding revenue triple digits is the entire bull case in one sentence.

$60 Is a Stretch, But Here’s Why It’s Possible

To hit $60 in 2027, SMCI needs a 45.3% gain from here. It is a stretch, but not a long shot.

Three things need to go right. The export-control review must close cleanly. Gross margins need to keep recovering toward double digits. And Blackwell Ultra shipments have to convert the $13B+ order book into reported revenue without further inventory write-downs.

What would derail it: another quarter of margin compression that resets the EPS curve lower. We’ve outlined the blueprint for how Super Micro Computer could reach $60 in 2027.