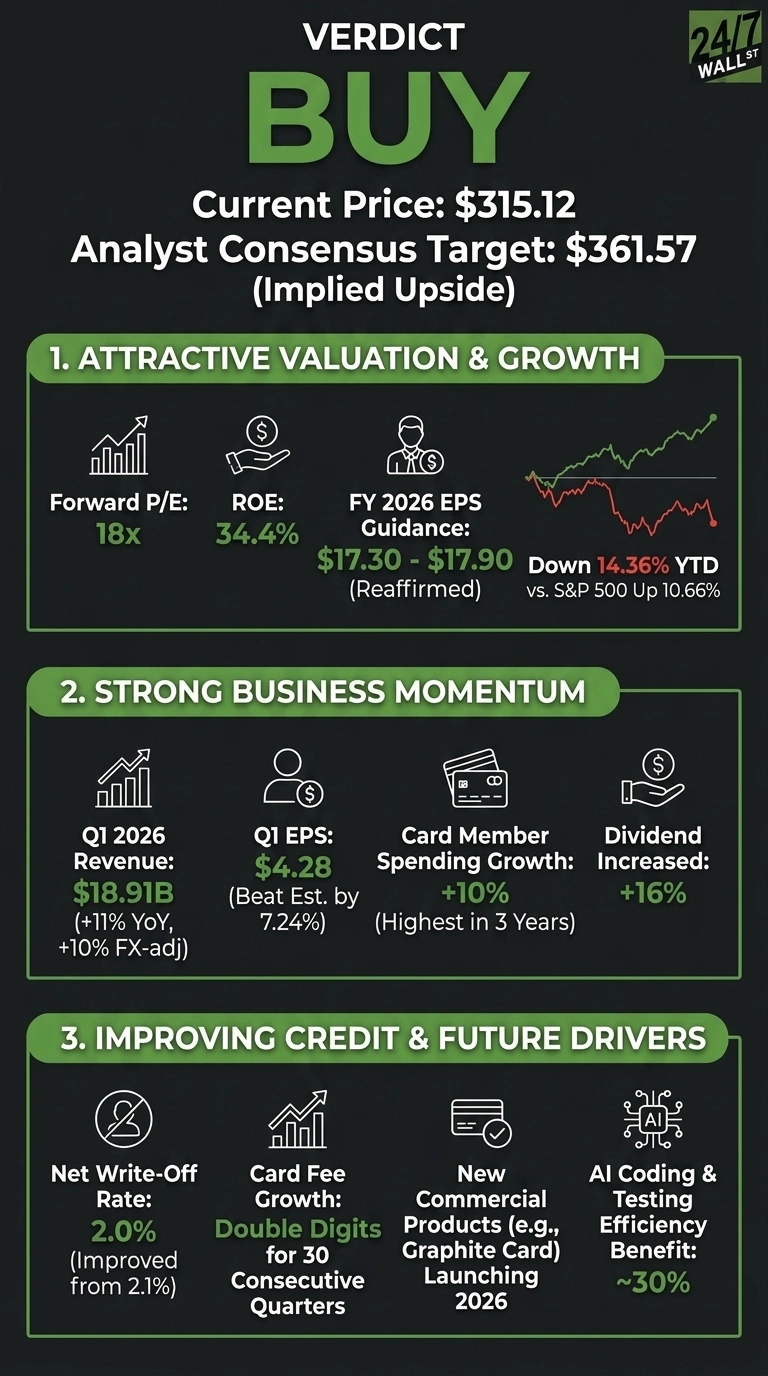

At $315, American Express (NYSE:AXP | AXP Price Prediction) looks attractively positioned. The stock has lagged while the underlying business accelerated, creating a potential opportunity.

American Express runs a closed-loop payments network anchored by premium, fee-paying cardholders. That model produces fatter spreads than open-loop rivals because Amex earns swipe fees from merchants and annual fees from cardholders while underwriting its own credit.

The company finished FY 2025 with $72.23B in revenue and $15.38 in EPS, and just printed its highest quarterly Card Member spending growth in three years.

Shares fell sharply after the Q1 2026 print on April 23, when investors fixated on heavier marketing and technology reinvestment and tariff-linked macro fears. That repricing, not the operating results, is what makes the current entry interesting.

Why the Sell-Off Created a Setup

Q1 2026 was a beat across the board. EPS came in at $4.28 against a $3.99 estimate, revenue hit $18.907 billion, net income rose 14.98%, and billed business grew 10% to $428 billion. Management reaffirmed full-year guidance of 9% to 10% revenue growth and EPS of $17.30 to $17.90.

Credit is improving. The net write-off rate fell to 2% from 2.1%, and CFO Christophe Le Caillec noted “write-off dollars are up by only 4% year-over-year, while NII is growing at double-digit pace.” Younger cohorts are powering the franchise: Gen Z spending is up 38%, millennials up 13%, and over 70% of new accounts are on fee-paying products.

On valuation, forward P/E sits at 18 with ROE of 34.4%. That is a reasonable multiple for a compounder growing EPS in the high teens and returning capital aggressively.

Why the Bears Have a Point

Amex is a consumer credit story heading into a soft macro. Tariff overhang, a potential consumer slowdown, and the threat of credit card interest rate caps all sit over the stock. Q4 2025 EPS of $3.53 missed the $3.55 estimate, the first crack in a clean run, and consolidated expenses rose 10% in that quarter.

Wall Street is not effusive. 15 analysts rate the stock Hold against 11 Buy or Strong Buy ratings and 1 Sell. Insider activity has tilted toward distribution: EVP Controller Quinn Lieberman disposed of 3,032 shares at $300.02 in early March. The stock trades below both its 50-day and 200-day moving averages, signaling that institutional money has yet to step back in.

The Patience Argument

A hold case is defensible. PEG of 1.54 is not screaming cheap, and the Platinum refresh will lap into 2027, removing a key tailwind. Le Caillec told investors “I wouldn’t expect a further acceleration; I expect that step-up to maintain into 2027.” Investors waiting for a clearer macro picture or a sub-$300 retest are not obviously wrong.

The cost of waiting is real. Card fees have grown double digits for 30 consecutive quarters, the dividend was raised 16%, and buybacks took diluted share count from 702M to 686M over a year.

The Numbers Behind the Call

AXP trades at $315.12, against an average analyst price target of $361.57, implying meaningful upside. The coverage universe spans 27 analysts:

- Strong Buy: 3

- Buy: 8

- Hold: 15

- Sell: 1

AXP is down 14.36% year to date, while the S&P 500 is up 10.66%. Shares trade at a trailing P/E of 20 and forward P/E of 18, with a 1.1% dividend yield.

At $315, the Setup Favors the Bulls

The market is pricing a credit cycle that the data is not delivering. Net write-offs improved, premium spend accelerated, and management raised marketing investment because “we’ve decided to increase our investments in marketing and technology to capitalize on key growth opportunities.” That is an offensive posture.

If Amex hits the midpoint of its $17.30 to $17.90 EPS guide, a 19x multiple gets the stock back near analyst targets within 12 months. Card fee growth runs into the high teens by year-end, the Graphite small-business card and a corporate cash-back launch arrive in the back half, and AI productivity is already delivering a 30% benefit in coding and testing.

The thesis breaks if write-offs spike above 2.5% or if billed business growth drops below 5%. Watch the next two quarters of credit metrics and Platinum retention.

An 18x forward compounder with 35% ROE trading after a 14% drawdown into a strengthening operating backdrop is the kind of setup that has historically rewarded patient holders.