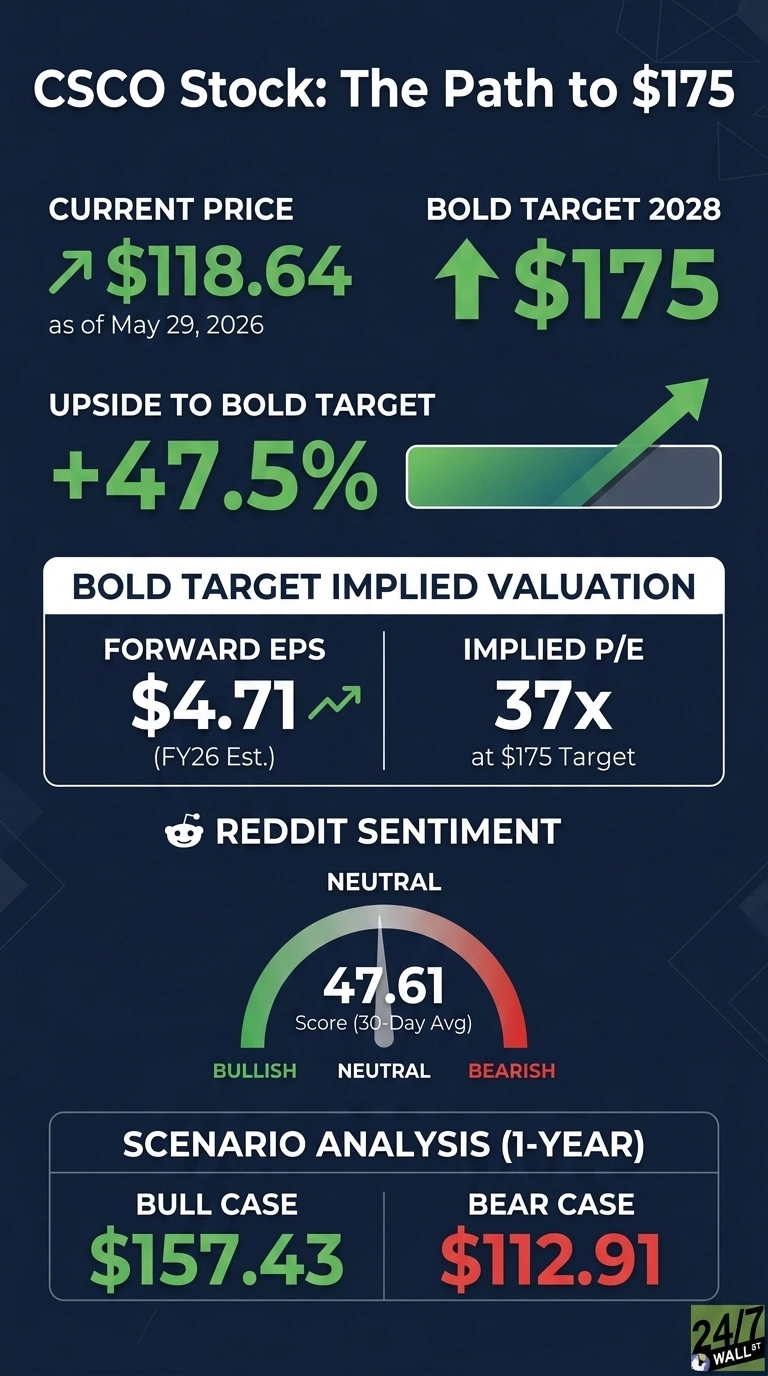

Cisco Systems (NASDAQ:CSCO | CSCO Price Prediction) just posted record quarterly revenue of $15.84 billion with networking up 25% year over year and AI infrastructure orders of $5.3 billion year to date. The stock has more than doubled, climbing 91.59% over the past year to $118.64. Can CSCO reach $175 by 2028? That is a stretch, but not impossible.

What Could Stall Cisco’s Run From Here

Cisco is extended. Shares are up 55.67% year to date and trading 4% below the 52-week high of $120.79. The easy re-rating has already happened, and the past month alone added another 36.59%.

Underneath the headline beats, real frictions exist. Gross margins are contracting as the product mix shifts toward lower-margin AI hardware. Services revenue declined 1% YoY, and operating cash flow fell 7% in Q3. Insider activity has skewed toward net selling. Beta sits at 0.912, so violent drawdowns are unlikely, but a melt-up requires an earnings catalyst.

Wall Street Sees 6% Upside. I Think That Is Wrong.

Wall Street’s consensus price target is $125.41, with 4 Strong Buys, 13 Buys, 9 Holds, and zero Sells. From today’s price that is barely 6% upside. Our model’s base case lands at $137.81 with 16.16% upside and a 90% confidence level. The optimistic scenario is $157.43, the conservative scenario $112.91.

The analyst community is anchored to last year’s Cisco, still modeling a low single-digit grower. The 65% bullish, 0% bearish distribution shows positive sentiment, but price targets have not caught up to the FY26 guide raise from $59-60B to $62.8-63B. That gap is the opportunity.

The Path to $175 Per Share

Reaching $175 from today’s price of $118.64 requires a 47.5% gain. With forward EPS of $4.71, a price of $175 implies a forward P/E of 37x. Our base case of $137.81 already implies 29x, meaning the bold target requires roughly 8x additional multiple expansion or, more likely, EPS that grows into the multiple.

The second path is realistic. AI infrastructure orders were raised this quarter to $9 billion for FY26, up from $5 billion, and AI revenue guidance jumped to $4 billion from $3 billion. Data center switching orders grew over 40%.

CEO Chuck Robbins put it bluntly: “Cisco is well-positioned as the critical infrastructure for the AI era, building on our technology leadership and customer trust, while innovating at the speed and scale that our dynamic world demands.” The primary risk is hyperscaler concentration: a pause in webscale capex would compress both orders and the multiple.

Where Cisco Trades Today vs Its Earnings Power

The current forward P/E sits at 25x against forward EPS of $4.71. For a company guiding to 12% revenue growth with 37.1% YoY earnings growth and a 25.2% return on equity, that does not look expensive.

Shares trade between a 52-week range of $60.90 and $120.79. Long-term holders have been rewarded: CSCO is up 454.98% over the past decade. The bull case for $175 rests on Cisco being valued as a structural AI infrastructure beneficiary rather than a mature networking vendor.

Is $175 Realistic? Here Is My Take

$175 by 2028 requires a 47.5% gain from here. That is a stretch, but not a fantasy.

Three things need to go right: AI infrastructure orders need to continue compounding toward and beyond the raised $9 billion FY26 target; gross margin pressure from AI hardware mix needs to stabilize; and the campus networking refresh cycle needs to extend into FY27 and FY28. A sharp hyperscaler capex pullback would derail the thesis. We’ve outlined the blueprint for how Cisco Systems could reach $175 in 2028.

Contact [email protected] for any questions or corrections.