Cisco Systems (NASDAQ:CSCO | CSCO Price Prediction) has quietly become one of the most compelling AI infrastructure plays in the market, even as retail chatter has turned sour.

The company just posted record quarterly revenue of $15.8 billion, raised full-year guidance, and told investors it now expects to book $9 billion in AI infrastructure orders from hyperscalers in FY26. Yet Reddit sentiment sits firmly bearish. Our proprietary model sides with management.

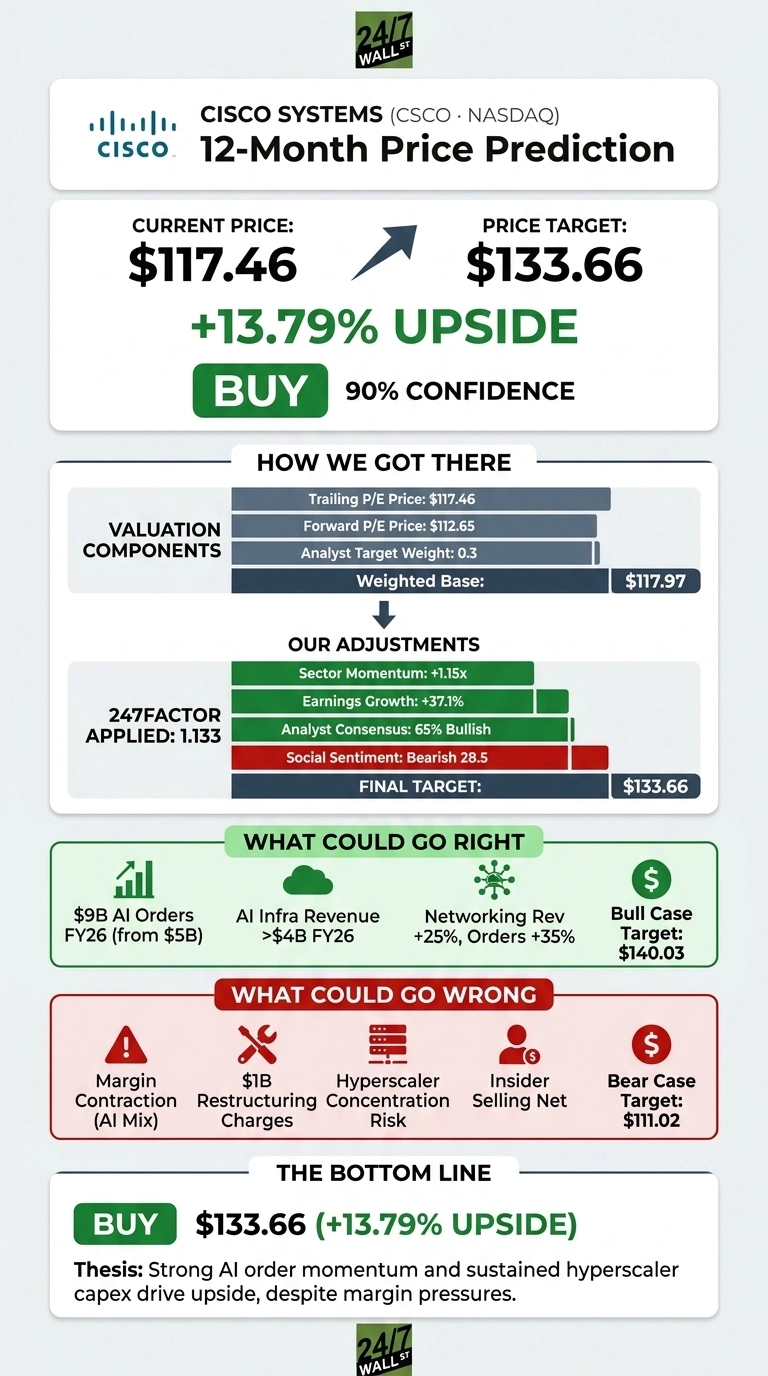

The 24/7 Wall St. price target for Cisco is $133.66, implying 13.79% upside from the current $117.46. Our recommendation is buy, with confidence at 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $117.46 |

| 24/7 Wall St. Price Target | $133.66 |

| Upside | 13.79% |

| Recommendation | BUY |

| Confidence Level | 90% |

The Stock Has Nearly Doubled Since April

Cisco is up 54.12% year to date and 73.17% over the past year, though shares have cooled 3.05% over the last week and trade about 10% off the 52-week high of $130.37.

The catalyst was the May 13 earnings release, where CSCO delivered its fourth consecutive EPS beat at $1.06 and revenue growth of 11.96% year over year. The stock jumped 13.41% on earnings day. Networking revenue surged 25%, and total product orders climbed 35%. Management raised FY26 revenue guidance to $62.8 billion to $63 billion and EPS to $4.27 to $4.29.

The Case for $140+

The bull case rests on AI infrastructure durability. CFO Mark Patterson told analysts “it’s reasonable to expect we will recognize at least $6 billion of revenue in FY ’27” from hyperscale AI alone. Acacia optics orders topped $1 billion in Q3, and Cisco booked five new Silicon One design wins with hyperscalers.

CEO Chuck Robbins said “Cisco is well-positioned as the critical infrastructure for the AI era.” Enterprise data center switching orders jumped over 40%, and public sector orders rose 27%. Our bull scenario points to $140.03, a 19.22% return.

The Risks Worth Watching

The trailing P/E of 38 is rich for a company whose long-term model is 4% to 6% growth in totality. Non-GAAP gross margins compressed 260 basis points on AI hardware mix, and Cisco is absorbing up to $1 billion in restructuring charges. Hyperscaler concentration is real: strip out webscale and order growth was 19%, of which 4 to 5 percentage points came from price increases rather than unit growth.

Insider activity has skewed net selling across 44 recent transactions. That said, bulls would note Patterson said “gross margins have stabilized” and the restructuring reinvests into silicon and optics, where Cisco is winning. Our bear case lands at $111.02.

Cisco Price Prediction 2026-2030

The 24/7 Wall St. price target of $133.66 reflects a buy with 90% confidence. The scale tips on AI order momentum: a jump to $9 billion of hyperscaler orders from an initial $5 billion plan represents a real backlog with a $6 billion FY27 revenue floor.

The bullish thesis holds if hyperscaler capex sustains through 2027 and Silicon One keeps taking share. The bearish scenario plays out if enterprise pull-forward reverses in FY27 or memory costs re-inflate.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $133.66 |

| 2027 | $145.00 |

| 2028 | $158.00 |

| 2029 | $170.00 |

| 2030 | $180.89 |

These projections assume Cisco continues executing on its AI infrastructure roadmap and campus refresh cycle. Significant upside or downside could result from hyperscaler capex trends and Silicon One share gains.

Contact [email protected] for any questions or corrections.