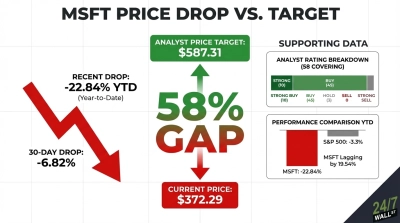

Microsoft (NASDAQ:MSFT | MSFT Price Prediction) just posted a quarter that should have shares ripping higher. Instead, the stock is down 6.49% year to date and trading at $450.24.

Yet CEO Satya Nadella just told investors that “Our AI business surpassed an annual revenue run rate of $37 billion, up 123% year-over-year.” Commercial RPO sits at $627 billion. The disconnect is real. Can Microsoft shares reach $650 by June 2027?

Why Microsoft Shares Are Stuck Despite Record AI Growth

The selling pressure has a name: capex. Q3 FY26 capex hit $30.88 billion, up 84.39% YoY, and investors are demanding proof that the spend will pay off. Sentiment briefly cratered in May after the Gates Foundation disclosed it sold its remaining MSFT position, fueling near-term doubt.

Shares are down 1.05% over the past year, with a brutal February low of $396.86. The recovery is underway. MSFT is up 7.57% over the past week and 6.3% over the past month, but with a beta of 1.093, the swings cut both ways. The market wants margin clarity before re-rating the multiple.

Wall Street Sees 24% Upside. I Think the Setup Is Bigger

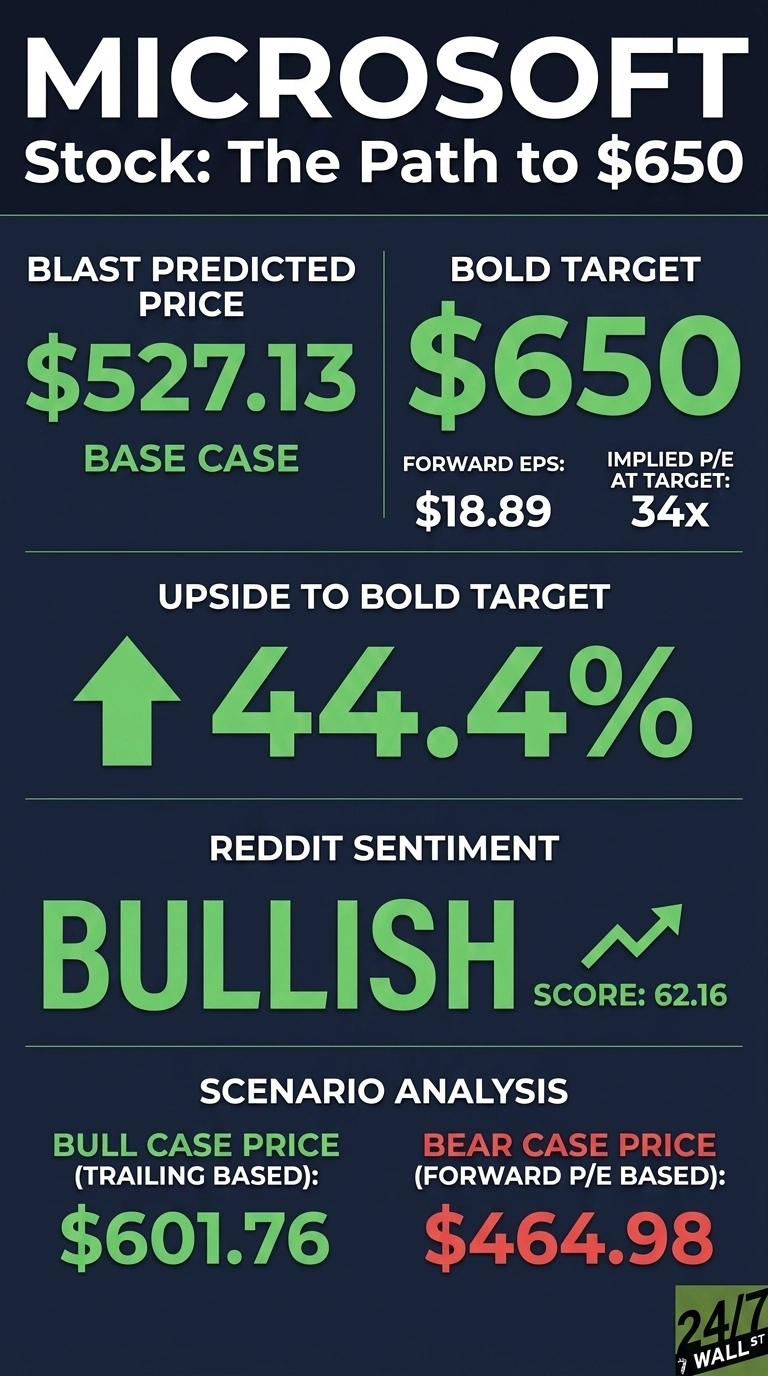

Consensus is squarely bullish. 51 analysts cover MSFT with 9 Strong Buys, 42 Buys, 3 Holds, zero Sells, and the average target sits at $560.63. Our model is more measured at the base case, with a predicted price of $527.13, or 17.08% upside, at high confidence (90%).

The bull case extends to $601.76. With 94% bullish analyst consensus and 23.4% YoY earnings growth, the consensus target is anchored to a forward multiple that hasn’t yet absorbed the AI run-rate inflection. That gap is the opportunity.

The Path to $650 Per Share

Reaching $650 from today’s price of $450.24 would require a gain of 44.4%. With forward EPS of $18.89, a price of $650 implies a forward P/E of 34x. Our base case of $527.13 already implies 28x, meaning the bold target requires 7x of additional multiple expansion.

That sounds aggressive but achievable. If EPS keeps compounding at the current pace, the multiple needed at $650 looks far less stretched twelve months from now.

Catalysts to watch: Azure growth of 40%, $250 billion in incremental Azure services contracted by OpenAI, and Nadella’s framing that “We are only at the beginning phases of AI diffusion and already Microsoft has built an AI business that is larger than some of our biggest franchises.” The primary risk is straightforward: if AI capex returns disappoint, the multiple compresses instead of expanding.

Where Microsoft Trades Today vs Its Earnings Power

At $450.24 against forward EPS of $18.89, MSFT trades at a forward P/E of roughly 24x. That is below the trailing P/E of 27 and well off the 52-week high of $551.05, with the 52-week low at $355.51.

Over the past decade, the stock has returned 860.84%. For a mega-cap compounder growing earnings north of 20% with the largest AI revenue stream in software, 24x looks cheap.

Can Microsoft Really Hit $650? My Verdict

Hitting $650 from $450.24 requires a 44.4% gain in twelve months. It is a stretch but achievable.

Three things need to go right. AI run-rate revenue must clear $50 billion. Operating margin needs to hold near the 46.3% TTM level despite the capex surge. And Azure growth has to stay above 35%. A capex hangover that forces analysts to cut FY27 numbers derails it. Returns at this level shouldn’t be expected every year, but we’ve outlined the blueprint for how Microsoft could reach $650 in 2027.