Microsoft (NASDAQ:MSFT | MSFT Price Prediction) is having one of its strangest years in recent memory. The AI franchise is exploding, with CEO Satya Nadella telling investors “Our AI business surpassed an annual revenue run rate of $37 billion, up 123% year-over-year.”

Yet shares trade at $421.06, down 12.74% year to date. Intelligent Cloud just reported $34.681 billion, up 30%, and Azure grew 40%. Can Microsoft shares reach $625 by 2028? The path exists, and the math is more reasonable than the share price suggests.

The Real Reason Microsoft Is Down 12.7% This Year

The issue is the bill. Capital expenditures hit $30.876 billion in the most recent quarter, up 84.39% year over year, and the market is questioning AI return on capital. OpenAI investment losses widened to $3.1 billion in Q1 FY2026 versus $523 million a year earlier. More Personal Computing was down 1%. Shares are off 7.56% over the past year and sit roughly 2% off the 52-week high of $552.24 after a brutal February bottom near $396.86. With a beta of 1.093, volatility is contained; the real drag is confidence.

Wall Street Sees 33% Upside. Our Model Is Below That

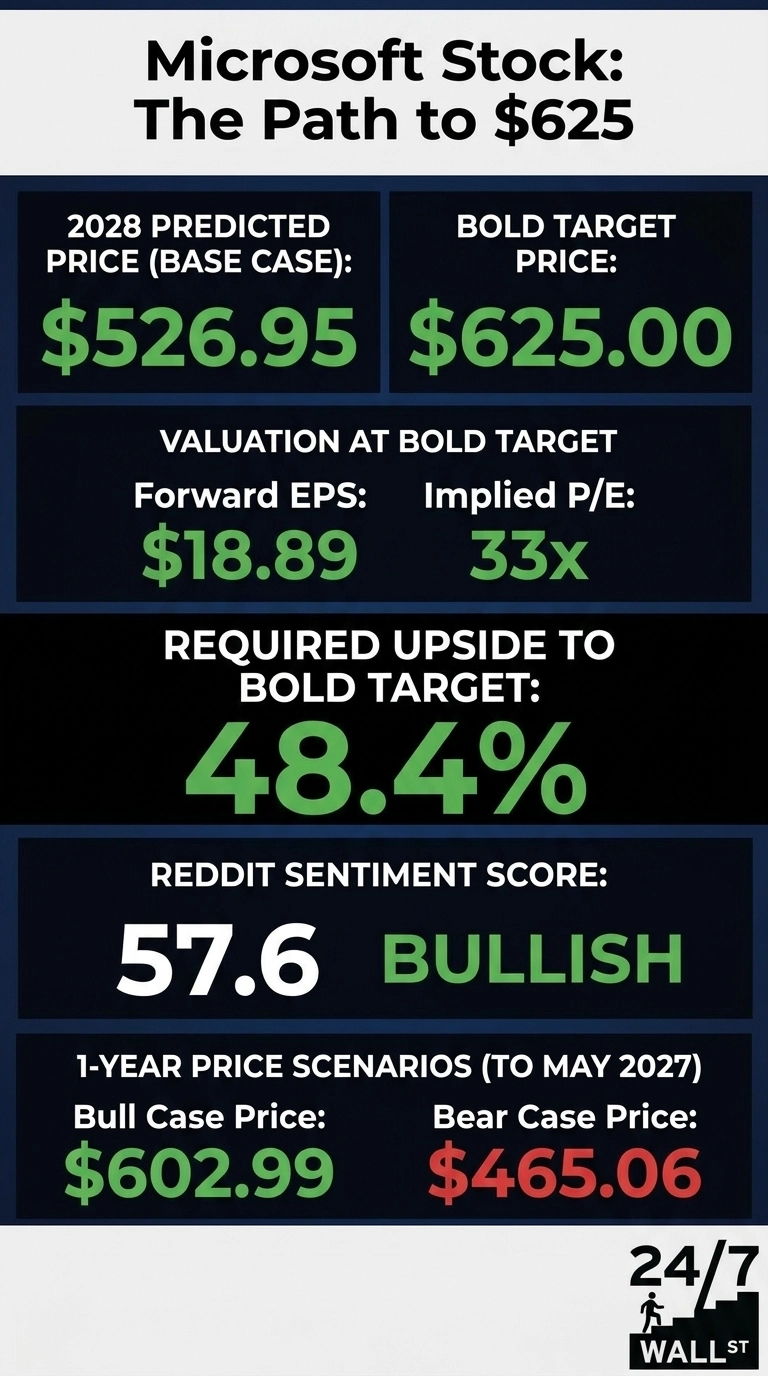

The Street consensus target sits at $560.63, backed by 9 Strong Buy, 42 Buy, and 3 Hold ratings, with zero sells. Our internal model lands at a 2028 base case of $526.95, a 25.15% return with high confidence (90%), with a bull case of $602.99 and bear case of $465.06.

We are more conservative than the Street due to mega-cap dampening. A $3.1 trillion base cannot compound like a small cap. That said, with 94% bullish analyst sentiment and 23.4% quarterly EPS growth, analysts are directionally right and our model may be too cautious on the upside tail.

The Path to $625 Per Share

Reaching $625 from today’s price of $421.06 would require a gain of 48.4%. With forward EPS of $18.89, a price of $625 implies a forward P/E of 33x. Our base case of $526.95 already implies 26x, meaning the bold target needs roughly 7x of additional multiple expansion.

Is that achievable? Yes, if three things hold. First, the adjustment factor of 1.15 reflects sector momentum plus 94% bullish analyst posture, both expanding as AI revenue compounds.

Second, commercial remaining performance obligations hit $627 billion, nearly doubling year over year. That is contracted future revenue.

Third, the OpenAI partnership now extends IP rights through 2032, with OpenAI committed to $250 billion of incremental Azure spend. Nadella framed it bluntly: “We are only at the beginning phases of AI diffusion and already Microsoft has built an AI business that is larger than some of our biggest franchises.” The primary risk: if AI capex returns disappoint, the multiple compresses instead of expanding.

Where Microsoft Trades Today vs Its Earnings Power

At $421.06 on forward EPS of $18.89, Microsoft trades at 22x forward earnings. For a business compounding revenue at 18.3%, earnings at 23.4%, and generating 34% ROE with 46.3% operating margins, that is cheap. Shares sit between the 52-week low of $356.28 and high of $552.24. The 10-year return is 838.78%. Investors who held through every capex panic were rewarded.

Is $625 Realistic? Here’s My Take

Reaching $625 by 2028 requires a 48.4% gain and roughly 7x of P/E re-rating on top of our base case. It is a stretch, but defensible.

Three things need to go right: AI revenue must keep growing above 100%, Azure must hold its 40% growth rate, and capex intensity must start showing operating leverage. A hard correction in AI demand that turns today’s $30.876 billion quarterly capex into a depreciation anchor would derail it. We’ve outlined the blueprint for how Microsoft could reach $625 in 2028.

Contact [email protected] for any questions or corrections.