At $326 and $493, Visa (NYSE:V | V Price Prediction) and Mastercard (NYSE:MA) screen attractively after a year of underperformance that has reset valuations on two durable franchises in financial services.

The card networks earn a small slice on roughly every swipe, tap, and cross-border transaction. Both stocks have sold off since mid-2025 on stablecoin disruption fears, interchange litigation overhang, and rotation out of high-multiple compounders. The fundamentals keep strengthening.

Why the Sell-Off Has Created a Window

Visa delivered 14.6% revenue growth in fiscal Q1 2026 with non-GAAP EPS of $3.17, while Mastercard posted 15.8% revenue growth and a 4.24% EPS beat, its fourth consecutive. Mastercard’s value-added services grew 22% and adjusted operating margin expanded to 60.8%.

Forward multiples are reasonable: Visa trades at roughly 25x forward earnings and Mastercard near 25x, both inside five-year ranges. Cross-border volumes grew 11% at Visa and 13% at Mastercard. Visa has $21.1 billion of buyback authorization and Mastercard has $11.7 billion.

Why Bears See a Structural Reset

Stablecoins and agentic commerce threaten to route transactions around card rails. Regulatory pressure on interchange is unrelenting. Visa absorbed a $707 million litigation provision in Q1, the fourth hit in five quarters.

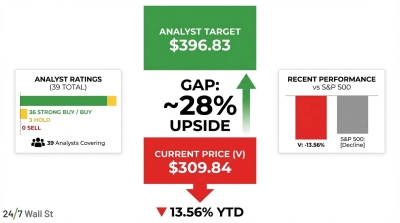

Visa is down 6.56% year to date and 9.24% over twelve months. Mastercard is off 13.19% YTD and 14% over a year, trading below its 200-day moving average of $541.87. Mastercard also faces higher effective tax rates from Pillar 2 global minimum tax rules.

The Argument for Sitting Tight

Both stocks are caught in a sentiment downdraft where good earnings are not moving the multiple. Reddit data shows bullish dividend-investor chatter but unscored high-volume debate in r/wallstreetbets, signaling institutions are still digesting the stablecoin narrative.

Waiting for clarity on the BVNK integration, interchange litigation resolution, or a quarter where stablecoin volumes dent network growth would be defensible. The cost is the dividend, buyback yield, and risk of paying up later.

What the Numbers Say

Visa trades at $326.36 against an analyst target of $398.74, implying upside, with 35 Buy ratings, 3 Holds, and zero Sells. Mastercard sits at $493.98 against a $646.97 target, with 36 Buys, 3 Holds, and no Sells.

With the S&P 500 roughly flat year to date, Visa’s 6.56% YTD decline and Mastercard’s 13.19% slide represent clear underperformance. Over five years, Visa is up 49.07% and Mastercard up 41.02%.

The Verdict: Bullish on Both, With Mastercard as the Sharper Setup

At $326 and $493, Visa and Mastercard screen attractively on the numbers.

Both networks grow revenue at 14% to 16%, expand margins, and return billions per quarter, yet trade at forward multiples in line with the broader market. Stablecoin and agentic commerce threats are real but multi-year. Visa is building its hyperscaler stack and Mastercard launched BVNK acquisition and Agent Pay.

Mastercard is the sharper setup. It grows faster, expands margins more aggressively, and has fallen further from highs, giving wider gap to consensus targets. Visa offers more buyback firepower and lower beta of 0.784, making it more defensive.

The thesis breaks if cross-border volumes roll over, if a major regulator caps interchange, or if stablecoin settlement shows up in volume disclosures. Watch quarterly cross-border growth and value-added services revenue.

When the toll booth gets cheaper and traffic keeps growing, the toll booth tends to look more interesting.