Our Rambus (NASDAQ:RMBS | RMBS Price Prediction) call is a tough one to make, because this stock has been a runaway winner.

After a 166.41% one-year rally, the 24/7 Wall St. price target points to meaningful downside over the next 12 months. Memory interface chips remain a core AI infrastructure play, but valuation has stretched ahead of fundamentals.

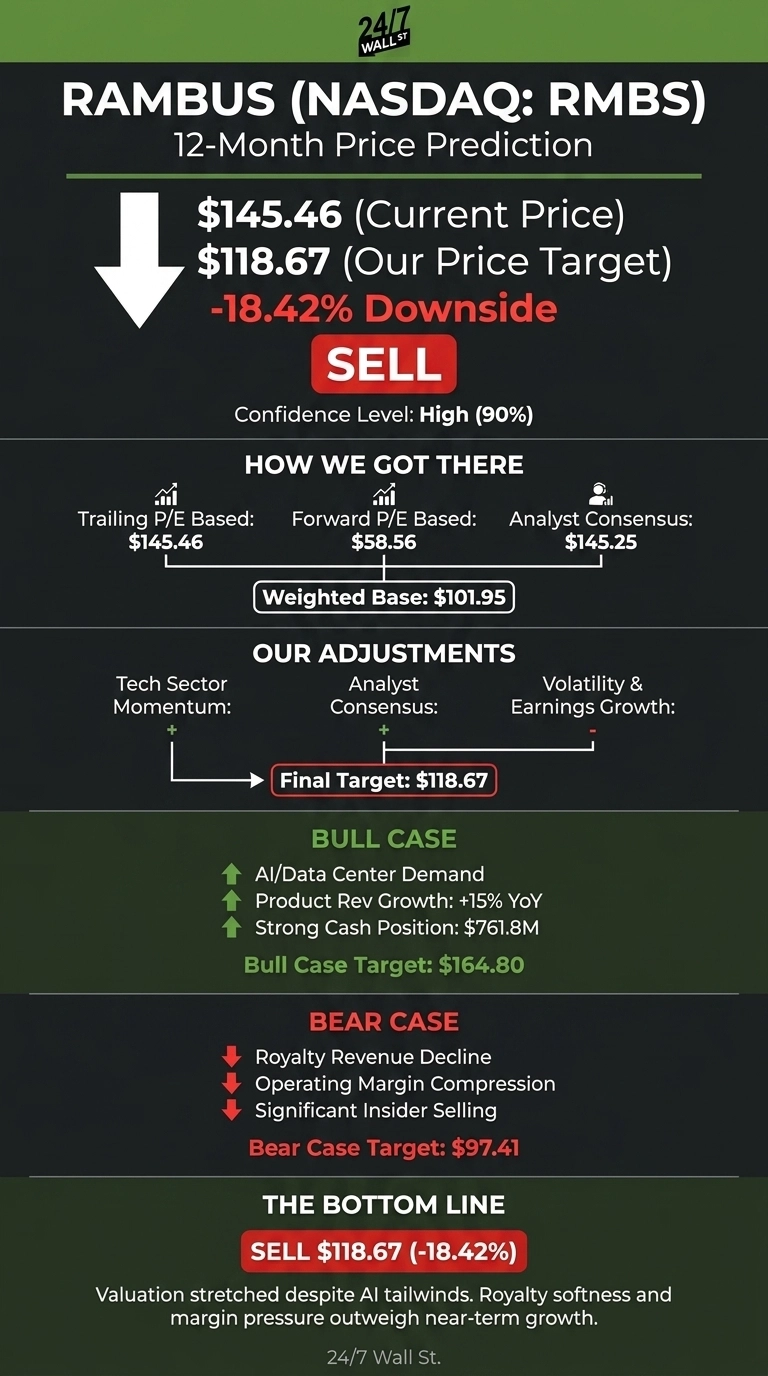

The 24/7 Wall St. Price Target for Rambus Is $118.67

| Metric | Value |

|---|---|

| Current Price | $145.46 |

| 24/7 Wall St. Price Target | $118.67 |

| Upside/Downside | -18.42% |

| Recommendation | SELL |

| Confidence Level | 90% |

Our 24/7 Wall St. price target for Rambus is $118.67, implying roughly 18% downside from current levels. The model returns a sell with high confidence, driven by an implied forward P/E of 64 and a stock that now sits just 10% below its 52-week high.

Why We Could Be Wrong on Rambus

Before going further, the bull arguments here are serious. Rambus owns mission-critical IP for DDR5, HBM4E, and the emerging LPDDR5X SOCAMM2 server module standard.

If hyperscaler memory bandwidth demand keeps compounding, royalty and product revenue could re-accelerate together, and our 24/7 Wall St. price target will look conservative. Consider this one datapoint among many. The detailed bull case follows.

An AI-Fueled Run From $54 to $145

RMBS is up 29.69% in the past month and 58.3% year to date.

Q1 FY26 revenue of $180.19 million narrowly beat consensus, while non-GAAP EPS of $0.63 came in just below the $0.6363 estimate. Product revenue jumped 15% YoY on AI infrastructure demand, but royalties slipped to $69.64 million from $74 million. Shares initially fell 21.26% after the report, then ripped back 30.73% over the following 30 days.

The Case for $165+

Bulls have real ammunition. FY25 revenue grew 27.13% to $707.63 million, operating income jumped 45.34%, and operating cash flow hit $360 million. CEO Luc Seraphin said “The growth of AI inference and agentic workloads in the data center continues to drive demand for higher memory bandwidth, efficient data movement, and scalable connectivity.”

Rambus claims the industry’s fastest HBM4E memory controller IP, and Q2 product revenue guidance of $95 to $101 million implies continued double-digit growth. Analyst ratings sit at 7 Buys and 2 Holds with zero Sells. Our bull-case scenario reaches $164.80 by June 2027.

What Could Go Wrong

Royalties shrank YoY, R&D rose 18%, and non-GAAP operating margin compressed from 46% to 42%. An analyst downgrade flagged tightening DRAM supply, CFO Desmond Lynch resigned, and insider activity has been heavy. COO Sean Fan disposed of 37,814 shares at $151.69 on May 26, the largest single transaction in the recent window.

Bulls would counter that the margin compression reflects deliberate investment in HBM4E and SOCAMM2, and the CFO transition and abandoned lease charge are one-time items. Still, with an implied P/E near 70, the bear case lands at $97.41.

I’d Stay Cautious Here

The 24/7 Wall St. price target on Rambus is $118.67, a sell with 90% confidence. The key factor tipping the scale is valuation: a forward P/E above 60 leaves little room for the royalty softness already visible in Q1.

The bull thesis strengthens if royalty revenue reaccelerates above $75 million and gross margin re-expands. The bear thesis takes over if DRAM supply tightens further or operating margin slips below 40%.

Rambus Price Prediction 2026-2030

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $118.67 |

| 2027 | $112.50 |

| 2028 | $109.00 |

| 2029 | $107.50 |

| 2030 | $106.21 |

These projections assume Rambus continues executing on AI memory IP but absorbs valuation compression as forward earnings catch up. Significant upside could come from a faster HBM4E ramp, while a stalled royalty base would pressure results.

Contact [email protected] for any questions or corrections.