Our Rambus (NASDAQ:RMBS | RMBS Price Prediction) call lands on the cautious side after a powerful run. The memory interface and semiconductor IP designer has more than doubled in a year as AI infrastructure spending pours into DDR5, HBM, and high-bandwidth memory controllers. Our model says the easy money has already been made.

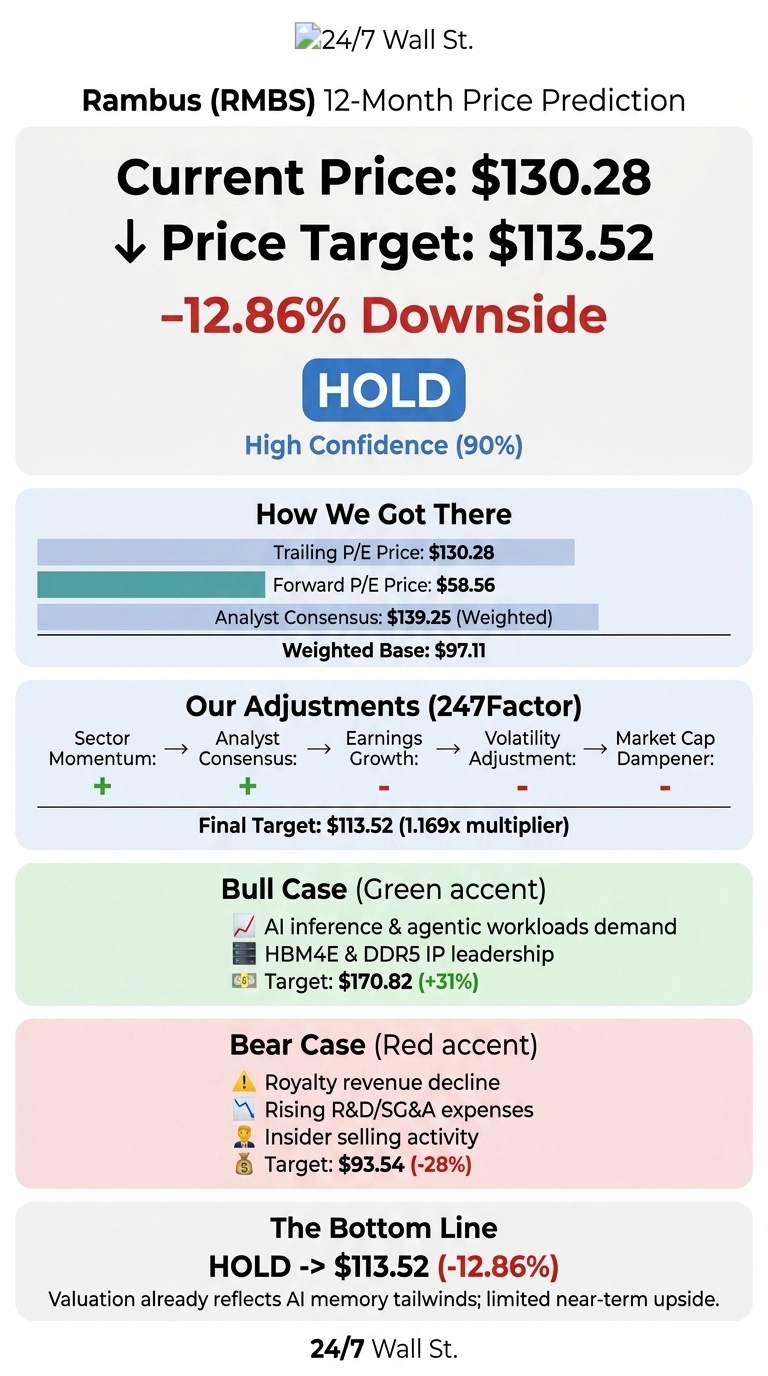

The 24/7 Wall St. price target for Rambus is $113.52, against a current price of $130.28. That implies -12.86% downside over the next 12 months. Our recommendation is hold, with a 90% confidence level, which qualifies as high conviction on the model side.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $130.28 |

| 24/7 Wall St. Price Target | $113.52 |

| Upside/Downside | -12.86% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Before going further, the 24/7 Wall St. price target of $113.52 sits below where Rambus trades today, and the bull arguments are real. Genuine upside could come from accelerating HBM4E memory controller IP adoption or a clean royalty re-acceleration as new licensing agreements close. Treat our number as one datapoint. A fuller bull case appears below.

A 140% Rally Met a Soft Quarter

RMBS is up 140.77% over one year and 41.78% year to date, trading 14% below its 52-week high of $161.80.

Q1 FY2026, reported April 27, brought revenue of $180.19M (up 8.1% YoY) and non-GAAP EPS of $0.63, missing the $0.636 consensus by 0.99%. Product revenue grew 15% to $88.0M, but royalty revenue slipped to $69.64M, and non-GAAP operating margin compressed to 42% from 46%. The stock dropped 21.26% on the report.

The Case for $170+

Bulls have a credible path. CEO Luc Seraphin says “the growth of AI inference and agentic workloads in the data center continues to drive demand for higher memory bandwidth, efficient data movement, and scalable connectivity.” Rambus owns the industry’s fastest HBM4E controller IP and is shipping LPDDR5X SOCAMM2 chipsets into next-gen AI servers.

Q2 FY2026 guidance points to revenue of $186 to $204M. Full-year FY2025 revenue grew 27.13% to $707.63M with operating income up 45.34%. Sell-side coverage skews positive with 8 buy ratings versus 1 hold. Our bull case scenario points to $170.82, a 31.12% return.

The Risks Worth Watching

Three headwinds keep us cautious. First, royalty revenue fell from $74.0M to $69.64M YoY, and an analyst downgrade cited tightening DRAM supply.

Second, operating expenses are accelerating, with R&D up 18% and SG&A up 13%. Bulls would counter that elevated R&D funds the HBM4E and SOCAMM2 roadmap that powers the long-term thesis.

Third, CFO Desmond Lynch resigned with John Allen stepping in as interim, and CEO Luc Seraphin executed multiple large disposals in March and April. Our bear case target is $93.54, a 28.2% drawdown.

Rambus Price Prediction 2026-2030

The 24/7 Wall St. price target of $113.52 reflects a real tension: Rambus has world-class IP in the right end markets, but at 64 trailing earnings and a forward P/E of 24, much of the AI memory story is priced in. The setup improves if Q2 FY2026 revenue lands at the high end of guidance and royalty revenue stabilizes. Caution stays warranted if margins compress further or DRAM supply tightens into a second quarter. Hold, with high model conviction.

Looking further ahead, here is where our model projects Rambus could trade, assuming current growth trajectories and AI memory tailwinds hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $113.52 |

| 2027 | $118.40 |

| 2028 | $124.10 |

| 2029 | $118.85 |

| 2030 | $109.56 |

These projections assume Rambus continues executing on its DDR5 and HBM4E roadmap. Significant upside could come from new licensing wins, while downside risk centers on royalty erosion and DRAM supply cycles.

Contact [email protected] for any questions or corrections.