Steve Eisman said on a recent podcast: “I’m sort of bewildered, given that there’s a war going on, why people would be selling defense stocks.” The reason that bewilderment matters to your portfolio is sitting on top of a wall of capital nobody is talking about.

Peter Arment, on the same segment, laid out the number: “$66 billion between 2020 and 2024 has come into the defense industry through venture capital and private equity.” Silicon Valley is rebuilding the Pentagon’s supply chain in real time, and the recent correction handed retail a window that doesn’t typically open twice.

1. Red Cat Holdings (RCAT): The Small-Cap Drone Pure-Play

Start with the name nobody on CNBC is leading with. Red Cat Holdings (NASDAQ:RCAT) is the textbook “purpose-built, lower-cost” archetype Arment described. Its Black Widow ISR drone is the Army’s Short Range Reconnaissance winner, the Blue Ops unit is pushing into unmanned surface vessels, and CEO Jeff Thompson is openly chasing the Pentagon’s drone budget line. Thompson said: “Secretary of War Hegseth has signaled budget allocations of up to $74 billion for UAV and USV procurement… in this arena, the Factory is the Weapon.”

Q1 FY26 told you the volume curve is bending: revenue hit $15.47 million, up 849.3% year over year, gross margin flipped to 12.7% from negative 52.1%, and management is guiding to a $150 million to $180 million annual revenue target. The stock is already responding, up 78% year to date and 56% in the past week alone.

The catch is that RCAT is one product line. If you want the same drone tailwind with a balance sheet behind it, the next ticker is where the institutional money is hiding.

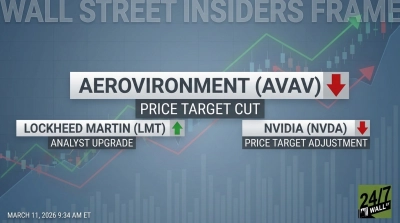

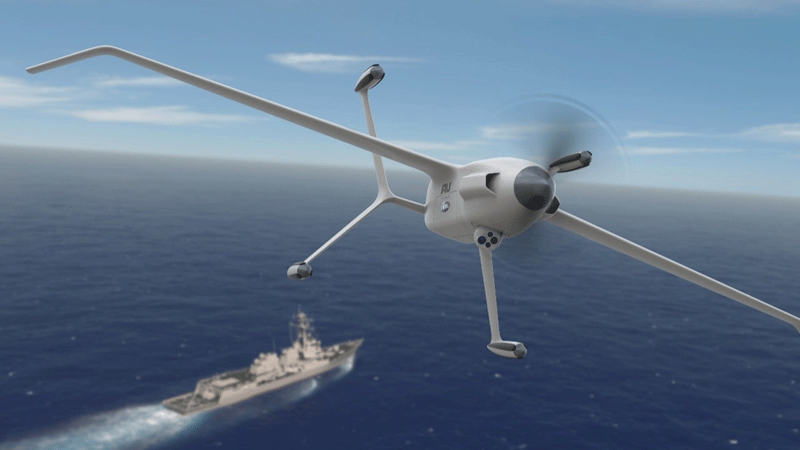

2. AeroVironment (AVAV): The Switchblade and BlueHalo Combination

AeroVironment (NASDAQ:AVAV | AVAV Price Prediction) is the publicly traded proxy for the Anduril-adjacent ecosystem. Switchblade loitering munitions are the weapon the Pentagon actually orders by the thousand, and the BlueHalo acquisition that closed in May 2025 bolted on space, cyber, and directed-energy capabilities that fit exactly into the FY2027 Department of War priority stack.

The order book tells the story. Q3 FY26 produced revenue of $408.05 million, up 143.4% year over year, a record funded backlog of $1.10 billion, and year-to-date bookings of $2.1 billion at a 1.6x book-to-bill. The stock is still down 11% year to date despite ripping 31% in the past week, which is precisely the correction Eisman flagged. The COO bought 1,800 shares at $194.39 on April 13, 2026, then the stock surged.

Hardware is half the story. The other half is the software brain that tells every drone, satellite, and Switchblade where to point. That brings us to the heavyweight.

3. Palantir (PLTR): The Software Layer of the New Defense Stack

Palantir (NASDAQ:PLTR) is Silicon Valley’s original defense disruptor. Maven Smart System, TITAN, and the Army’s next-generation battle command stack all run on Foundry and AIP. Every drone in this article eventually needs the data fusion layer Palantir sells, which is why CEO Alex Karp can plant a flag like this: “Palantir’s Rule of 40 score is now an incredible 127%… We are an n of 1.”

Q4 FY25 numbers were the kind that justify the multiple. Revenue of $1.41 billion grew 70% year over year, U.S. commercial revenue jumped 137% to $507 million, and GAAP operating income hit $575.4 million at a 41% margin. The complication is valuation. The stock trades at a P/E around 203 and is down 19% year to date, with Polymarket traders pricing only 29% odds of PLTR reclaiming $150 by month-end.

If you believe AI is the operating system of modern warfare, Palantir is the toll bridge. If you want the company actually launching the satellites that feed that software, keep reading.

4. Rocket Lab (RKLB): Vertically Integrated Space and Hypersonics

Rocket Lab (NASDAQ:RKLB) sits on the Austin-to-Southern California corridor Arment described, and it just got picked for the program that defines the next decade of national security spending. CEO Peter Beck confirmed it: “selected to support the Department of War’s Space Based Interceptor program under Golden Dome for America in partnership with Raytheon.” Electron and HASTE launches are flying, Neutron medium-lift is on deck for later in 2026, and the satellite manufacturing arm is now writing eight-figure deals on its own.

The Q1 FY26 print backed it up. Revenue came in at $200.35 million, up 63.5% year over year, backlog grew 20.2% sequentially to $2.20 billion, and the $816 million Space Development Agency contract for 18 Tracking Layer Tranche 3 satellites is the largest single award in company history. The shares are up 112% year to date and 412% over the past year, and prediction markets already resolved every May upside target through $104 to YES.

One name remains, and it is the cleanest visual proof that the era of $100 million fighters is over.

5. Kratos Defense (KTOS): The Punchline of the “60 Primes” Thesis

Kratos Defense & Security Solutions (NASDAQ:KTOS) is what Arment meant when he said “we’re going back to the ’80s, where there’s going to be 60 defense primes.” The Valkyrie XQ-58 is a jet-powered autonomous combat aircraft built to fly alongside crewed fighters, attritable on purpose, priced an order of magnitude below a manned platform. Add hypersonics, Zeus and Oriole solid rocket motors, and the jet engines that go inside everyone else’s drones, and Kratos is selling four of the FY2027 budget’s loudest line items at once.

CEO Eric DeMarco said: “Fiscal 2027 National Security spend is currently projected to be $1.5 trillion, an approximate $400 billion increase above Fiscal Year 2026.” Q1 FY26 already showed the operating leverage: revenue of $371 million, up 22.6% year over year, Unmanned Systems organic growth of 30.9%, and a 1.6x book-to-bill on $605.2 million of bookings. Valkyrie was just selected for the Northrop Grumman MUX TACAIR CCA program, with management planning to ramp production to roughly 40 aircraft per year by the end of 2027.

The setup: shares are down 14% year to date against an analyst target price of $113.05 on a stock trading near $65. I’ve been watching Kratos for the better part of two years, and this is the first quarter where the Valkyrie cadence, the hypersonic backlog, and the budget line items finally rhyme.

The Trade Setup

The math is pretty simple.

Silicon Valley funneled $66 billion of venture and private equity capital into defense between 2020 and 2024, the FY2027 budget is opening a $400 billion delta above FY2026, and the publicly traded names that touch this capital stack just sold off into the news. The legacy primes are the share donors; these five sit on the receiving end of the share shift. Watch the FY2027 budget cadence and the next round of contract awards across these five names.

Contact [email protected] for any questions or corrections.