Pfizer (NYSE:PFE | PFE Price Prediction) is one of those names where the headline narrative (COVID hangover, patent cliff) keeps overshadowing what is actually a defensive cash machine trading at a single-digit forward multiple. After running the numbers, my view leans constructive, and the 24/7 Wall St. price target reflects that.

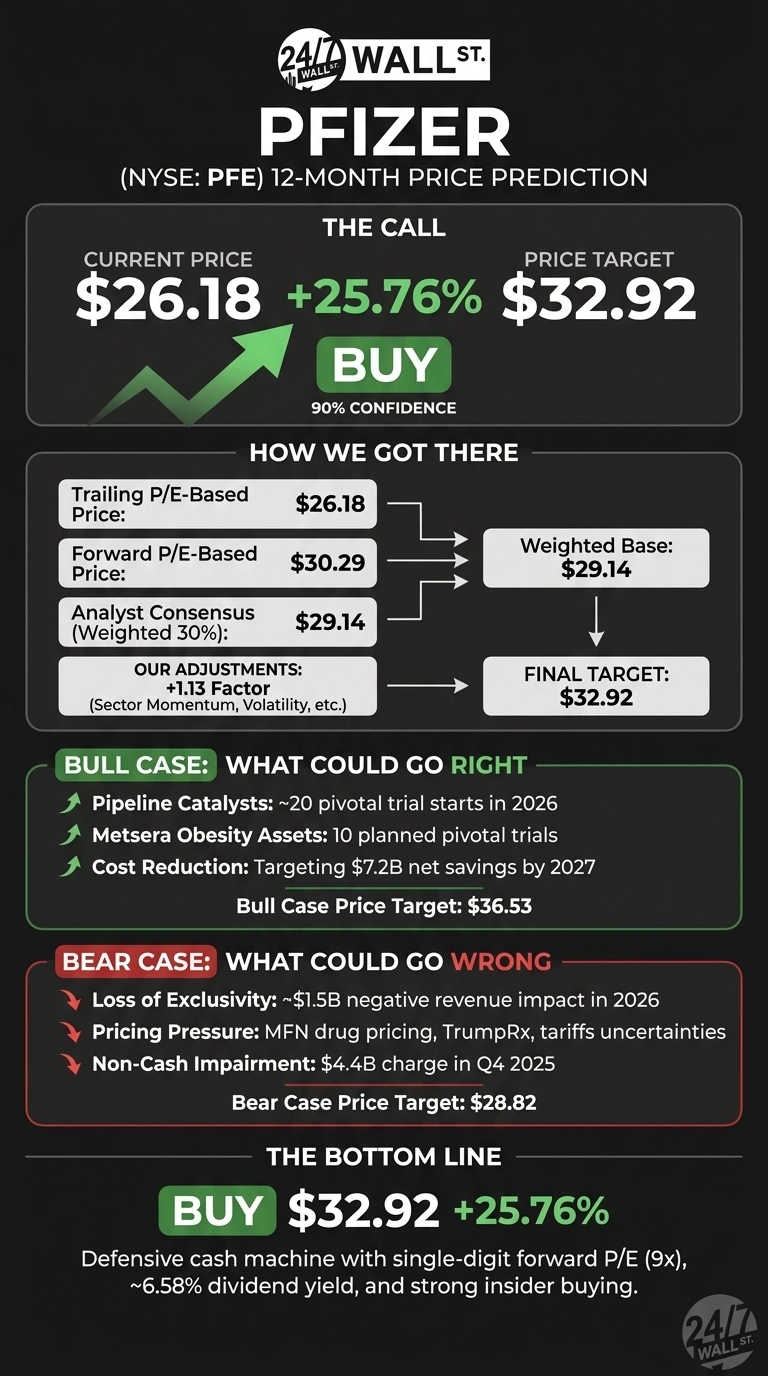

PFE stock trades at $26.18, and our 24/7 Wall St. price target for Pfizer is $32.92 over the next 12 months. That implies 25.76% upside, with a model confidence level of 90%. The recommendation is buy.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $26.18 |

| 24/7 Wall St. Price Target | $32.92 |

| Upside | 25.76% |

| Recommendation | BUY |

| Confidence Level | 90% |

The Non-COVID Engine Is Quietly Compounding

Pfizer is up 8.69% year to date and 19.48% over the past year, with the stock now sitting just 3% below its 52-week high of $28.28. The Q4 2025 earnings report on February 3, 2026 delivered adjusted EPS of $0.66 against a $0.57 consensus, with revenue of $17.56 billion beating estimates by 4.09%.

The story underneath is the post-COVID transition. Non-COVID revenue grew 9% operationally in Q4, with Abrysvo up 136%, Lorbrena up 45%, Eliquis up 10%, and the Prevnar family up 10%. Paxlovid fell 70% and Comirnaty fell 35%, but those declines are increasingly absorbed.

The Case for $36 and Higher

The bull case starts with the pipeline. Pfizer plans approximately 20 pivotal trial starts in 2026, including 10 obesity assets from the Metsera acquisition (priced at roughly $7 billion) and four trials for the PD-1 x VEGF bispecific from 3SBio.

Cost actions targeting $7.2 billion in net savings by 2027 should expand margins, and the $29.19 consensus analyst target (with 11 Buy/Strong Buy ratings) keeps a floor under sentiment.

Our bull-case scenario points to $36.53, a 39.54% return. Insider behavior reinforces this: 37 transactions between March and June 2026 were net acquisitions, including a coordinated 11-director buy on April 23 at $26.67.

The Risks Worth Watching

The bear thesis is real. Loss of exclusivity will shave roughly $1.5 billion off 2026 revenue, Most-Favored-Nation pricing and TrumpRx remain wildcards, and the Q4 GAAP loss of $1.65 billion reflected a $4.4 billion non-cash impairment.

That said, bulls would correctly note this is a non-cash charge that does not impair adjusted EPS of $3.22 for the full year, and gross profit actually expanded 11.15%. The bear-case path lands at $28.82, still a 10.07% return given the 6.58% dividend yield.

Pfizer Price Prediction 2026-2030

The 24/7 Wall St. price target of $32.92 reflects a buy rating with 90% confidence. The tipping factor is the combination of a 9x forward P/E, a 6.58% dividend yield, and insider buying into the rally. The constructive scenario depends on obesity pipeline readouts and oncology execution continuing at the current cadence.

The more cautious scenario emerges if MFN pricing rules land harder than guidance assumes or if Eliquis erosion accelerates before pipeline assets translate to revenue.

Looking further out, here is where our model projects Pfizer could trade, assuming current growth trajectories and pipeline execution hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $32.92 |

| 2027 | $37.50 |

| 2028 | $42.25 |

| 2029 | $46.80 |

| 2030 | $51.27 |

These projections assume Pfizer executes on its Metsera obesity assets and offsets loss of exclusivity with pipeline launches. Significant upside or downside could come from MFN drug pricing implementation or a successful GLP-1 entry.

Contact [email protected] for any questions or corrections.