Johnson & Johnson (NYSE:JNJ | JNJ Price Prediction) has been one of 2026’s quieter winners in large-cap healthcare, and our proprietary model sees room to run. With a landmark $100 billion revenue year in progress and 11 Innovative Medicine brands growing at double digits, the setup is more offensive than defensive.

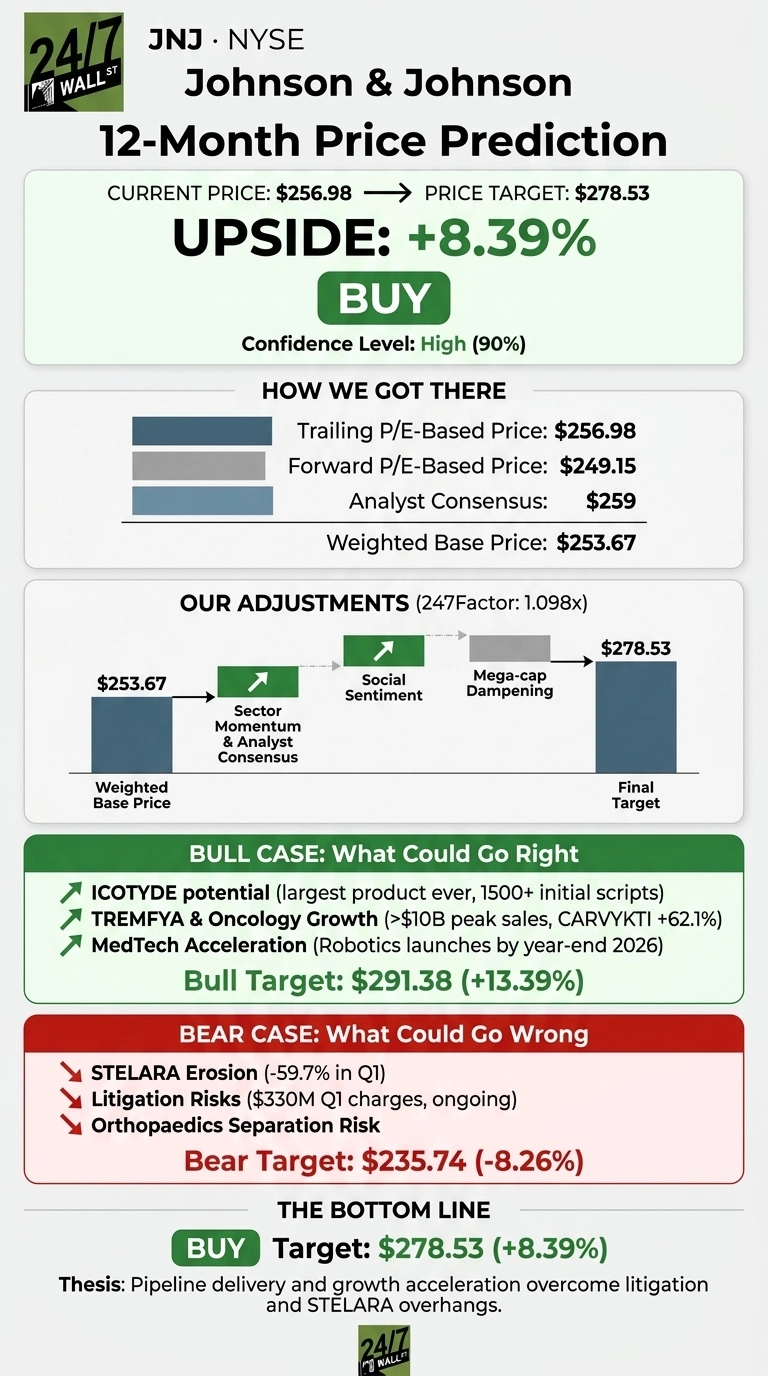

Our 24/7 Wall St. price target for Johnson & Johnson is $278.53, implying 8.39% upside from the recent close of $256.98. We rate JNJ a buy with 90% confidence. The pipeline is derisked, the dividend is a 64-year fortress, and the DePuy Synthes separation removes an anchor from reported growth.

| Metric | Value |

|---|---|

| Current Price | $256.98 |

| 24/7 Wall St. Price Target | $278.53 |

| Upside | 8.39% |

| Recommendation | BUY |

| Confidence Level | 90% |

From Litigation Overhang to Pipeline Story

JNJ has rallied 67.04% over the past year and 25.56% year to date, trading near its 52-week high of $269.43.

Q1 2026 was the catalyst: revenue of $24.06 billion beat consensus by 1.89%, adjusted EPS of $2.70 extended the beat streak to four, and management raised full-year guidance to $100.30 billion to $101.30 billion in revenue with adjusted EPS of $11.45 to $11.65. Standouts included DARZALEX at $3.96 billion (+22.5%) and TREMFYA at $1.61 billion (+68.3%).

The Case for $291 and Beyond

Our bull scenario puts JNJ at $291.38 in twelve months. Three catalysts drive it. First, ICOTYDE, the first oral IL-23 for psoriasis, which CEO Joaquin Duato said “could be one of our largest products ever” after 1,500 patient prescriptions in the first weeks post-launch.

Second, TREMFYA is tracking to peak sales above $10 billion, with RYBREVANT/LAZCLUZE growing 82.7% and CARVYKTI up 62.1%.

Third, MedTech growth accelerates as OTTAVA and MONARCH robotics both launch by year-end 2026. Polymarket traders are pricing a 92.5% probability JNJ beats Q2 earnings.

What Could Go Wrong

Our bear scenario drops JNJ to $235.74, a downside of -8.26%. STELARA fell 59.7% in Q1 as biosimilars eroded Innovative Medicine growth, and Q1 net income dropped 52.4% on litigation charges of $330 million.

Bulls counter that adjusted EPS still beat, free cash flow guidance sits at roughly $21 billion, and STELARA erosion was fully baked into the raised outlook. The Orthopaedics spin carries execution risk, and a PEG ratio of 4.94 leaves little forgiveness on a growth miss.

How JNJ Compares to Merck and Pfizer

Merck (NYSE:MRK) is the cleanest comparison on oncology franchise concentration. Merck’s 2026 EPS guide of $5.04 to $5.16 reflects heavier one-time charges from the $9 billion Cidara deal, and KEYTRUDA at $7.91 billion in Q1 represents concentrated patent-cliff risk that JNJ’s 28 billion-dollar brands do not carry.

Pfizer (NYSE:PFE) shows the valuation contrast. Pfizer trades at a trailing P/E of 18 with a 7.09% dividend yield, reflecting COVID-cliff and Eliquis loss-of-exclusivity concerns. JNJ trades at a forward P/E of 22 with a 2.01% yield. JNJ is delivering accelerating 9.91% revenue growth while Pfizer’s 2026 revenue is guided flat. Our $278.53 target looks reasonable against this peer set.

JNJ Price Prediction 2026 to 2030

Our 24/7 Wall St. price target of $278.53, buy rating, and 90% confidence rest on a simple thesis: JNJ is exiting its litigation and STELARA overhang as the pipeline delivers.

The thesis strengthens if ICOTYDE traction holds through the psoriatic arthritis readout later in 2026. It weakens if the DePuy Synthes separation slips or a fresh talc settlement dwarfs the current run rate. On balance, the setup favors the bull case.

Extending the model forward using JNJ’s guide to double-digit growth by decade-end, our 5-year base case reaches $353.01, a 37.37% total return.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $278 |

| 2027 | $298 |

| 2028 | $318 |

| 2029 | $335 |

| 2030 | $353 |

These projections assume JNJ executes its pipeline and completes the Orthopaedics separation on schedule. Meaningful deviation could come from a talc mega-settlement or an ICOTYDE peak-sales surprise well north of TREMFYA’s $10 billion trajectory.

Contact [email protected] for any questions or corrections.