From Gaming Chips to the Center of the AI Universe

A decade ago, NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) was still primarily known for GeForce gaming cards. The data center business existed, but nobody outside niche research circles cared about CUDA. Then came the crypto mining boom and bust, the Hopper H100 ramp, and the post-ChatGPT explosion that turned Jensen Huang’s company into the default picks-and-shovels trade for generative AI.

Over the past year, the story shifted again. Blackwell scaled into full production, Blackwell Ultra followed, and the Vera Rubin platform was announced with a promised order-of-magnitude jump in inference economics. Partnerships with OpenAI, Anthropic, Meta, Microsoft, Google Cloud, Oracle, and xAI piled up. China H20 restrictions bit, but non-China demand more than absorbed the shortfall.

What $1,000 Actually Became

1-Year Return

- Initial Investment: $1,000

- Current Value: $1,660.70

- Total Return: 66.07%

- S&P 500 (same period): $1,287.00 (28.70%)

5-Year Return

- Initial Investment: $1,000

- Current Value: $13,405.50

- Total Return: 1,240.55%

- Annualized Return: roughly 68%

- S&P 500 (same period): $1,804.60 (80.46%)

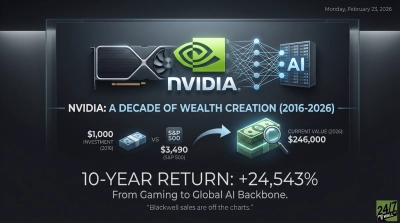

10-Year Return

- Initial Investment: $1,000

- Current Value: $196,656.60

- Total Return: 19,565.66%

- Annualized Return: roughly 70%

- S&P 500 (same period): $3,607.30 (260.73%)

A $1,000 bet in 2016 turning into nearly $197,000 looks inevitable in hindsight, but the path was brutal. Holders sat through the 2018 crypto-driven crash, a brutal 2022 drawdown of more than 60%, and several 20%+ pullbacks during the Blackwell ramp. The 10-year annualized number near 70% obliterates the S&P 500’s roughly 14%, and even the five-year window dwarfs the index. Timing mattered less than conviction.

Would I Put $1,000 In Today?

NVIDIA looks attractive if you believe the AI capex cycle has years left to run. Q1 FY27 revenue grew 85.2% to $81.6 billion, data center networking jumped 199%, gross margin sits at 75%, and supply commitments hit $119 billion. The forward multiple of 24x looks reasonable if Rubin extends the lead.

I’d avoid it if you think hyperscaler capex is about to digest. Heavy customer concentration with the largest cloud buyers, Amazon Trainium and Google TPU eating share, a $5.1 trillion market cap, and ongoing China restrictions are real risks. One disappointing CapEx guide from Microsoft or Meta could trim 20% quickly.

The bull case rests on continued AI capex; the bear case rests on hyperscaler digestion risk. With shares at a fresh 52-week high, entry timing carries more weight than usual.

Contact [email protected] for any questions or corrections.